Maine 4.26.7206 False Statements on Income Tax Return, 26 U.S.C. Sec. 7206(1), is a federal statute that makes it a crime to knowingly make false statements or representations on a federal income tax return. This includes filing a return containing false information, or willfully aiding in the preparation of an income tax return that contains false information. There are two types of false statements that can be made on a federal income tax return: fraud and negligence. Fraudulent tax returns are those that contain intentional false statements or omissions of material facts, while negligent tax returns are those that contain unintentional false statements or omissions of material facts. The penalty for violating Maine 4.26.7206 False Statements on Income Tax Return, 26 U.S.C. Sec. 7206(1), is a fine of up to $100,000, or imprisonment for up to three years, or both.

Maine 4.26.7206 False Statements on Income Tax Return, 26 U.S.C. Sec. 7206(1)

Description

How to fill out Maine 4.26.7206 False Statements On Income Tax Return, 26 U.S.C. Sec. 7206(1)?

If you are looking for a method to adequately prepare the Maine 4.26.7206 False Statements on Income Tax Return, 26 U.S.C. Sec. 7206(1) without employing a legal expert, then you are exactly in the right place.

US Legal Forms has demonstrated itself as the most comprehensive and esteemed collection of official templates for every personal and business situation. Every document you discover on our online service is created in accordance with national and state laws, ensuring your paperwork is correct.

Another fantastic aspect of US Legal Forms is that you will never lose the documents you obtained - you can access any of your downloaded forms in the My documents section of your account whenever you need them.

- Verify the document you see on the webpage aligns with your legal circumstances and state laws by reviewing its text description or exploring the Preview mode.

- Input the document title in the Search tab at the top of the page and select your state from the list to locate an alternative template in case of any discrepancies.

- Repeat the content verification and select Buy now when you are assured of the document's compliance with all requirements.

- Log in to your account and click Download. If you do not have a membership, register for the service and choose a subscription plan.

- Use your credit card or PayPal option to purchase your US Legal Forms subscription. The blank will be available for download immediately afterward.

- Choose the format in which you would like to save your Maine 4.26.7206 False Statements on Income Tax Return, 26 U.S.C. Sec. 7206(1) and download it by clicking the relevant button.

- Upload your template to an online editor for quick completion and signing, or print it out for manual preparation of your hard copy.

Form popularity

FAQ

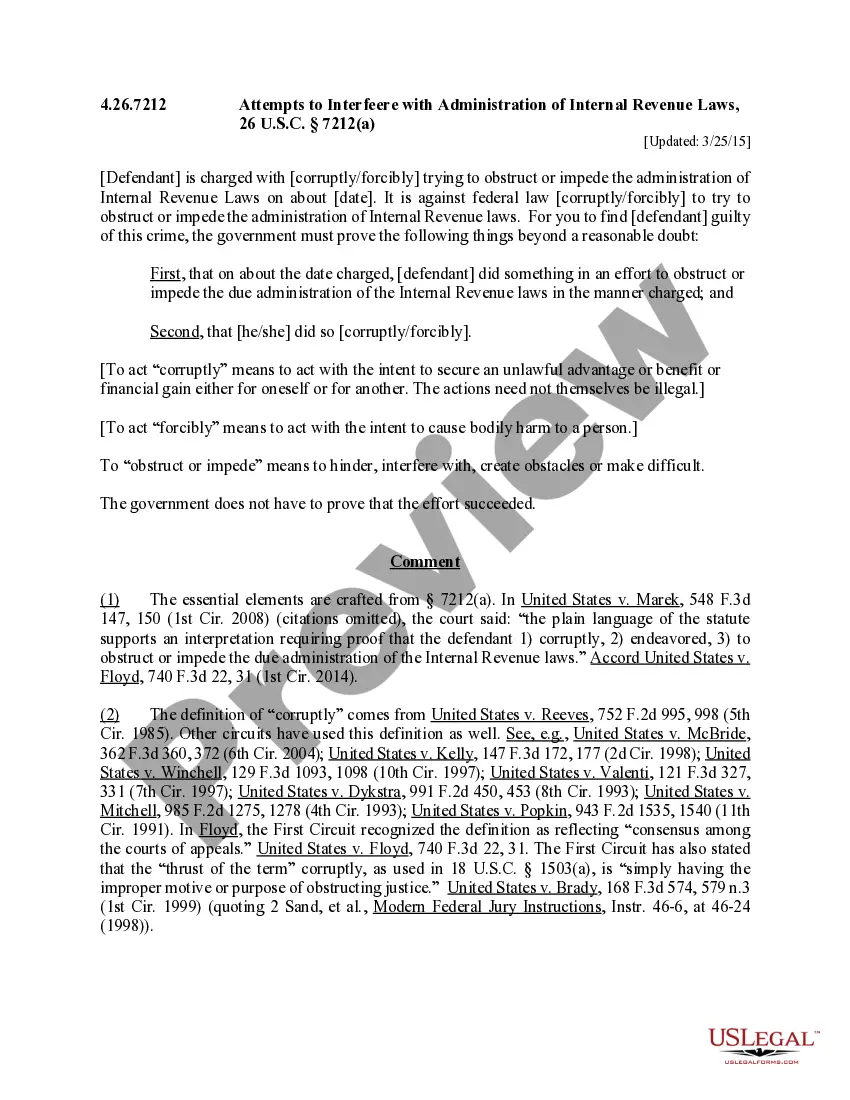

Shall be guilty of a felony and, upon conviction thereof, shall be fined not more than $100,000 ($500,000 in the case of a corporation), or imprisoned not more than 3 years, or both, together with the costs of prosecution.

Shall be guilty of a felony and, upon conviction thereof, shall be fined not more than $100,000 ($500,000 in the case of a corporation), or imprisoned not more than 3 years, or both, together with the costs of prosecution.

Section 7201 creates two offenses: (a) the willful attempt to evade or defeat the assessment of a tax, and (b) the willful attempt to evade or defeat the payment of a tax. Sansone v. United States, 380 U.S. 343, 354 (1965).

Title 26, United States Code, Section 7206(2), makes it a crime to willfully aid or assist in preparing or presenting a false return or document and provides as follows: Any person who?? (2) Aid or Assistance.

Can You be Prosecuted for Perjury or False Statements in Your Tax Returns? Yes, the Internal Revenue Code has its very own perjury and false statements statute. This crime is separate from the tax evasion statute, and different elements must be present for the taxpayer to be charged with perjury and false statements.

§ 7206 (1) and (2) makes it a crime to deliberately make or assist another person in making any IRS document that the maker does not believe to be true and correct.

7206 filing a fraudulent and false statement verified via written declaration under penalty of perjury is a felony and carries a penalty of imprisonment for up to 3 years, a $100,000 fine for individuals or a $500,000 fine for corporations, or both, and reimbursement to the federal government to cover the costs of