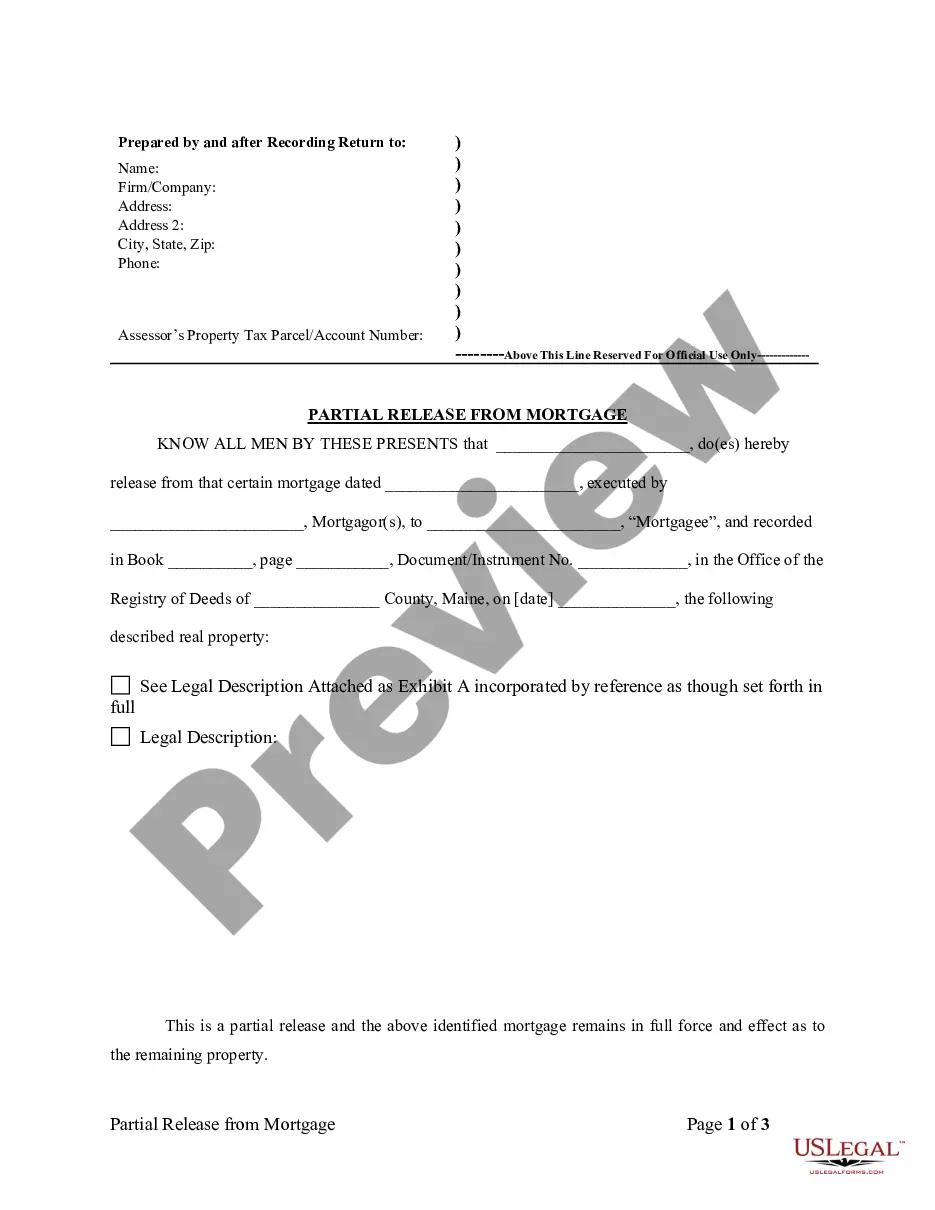

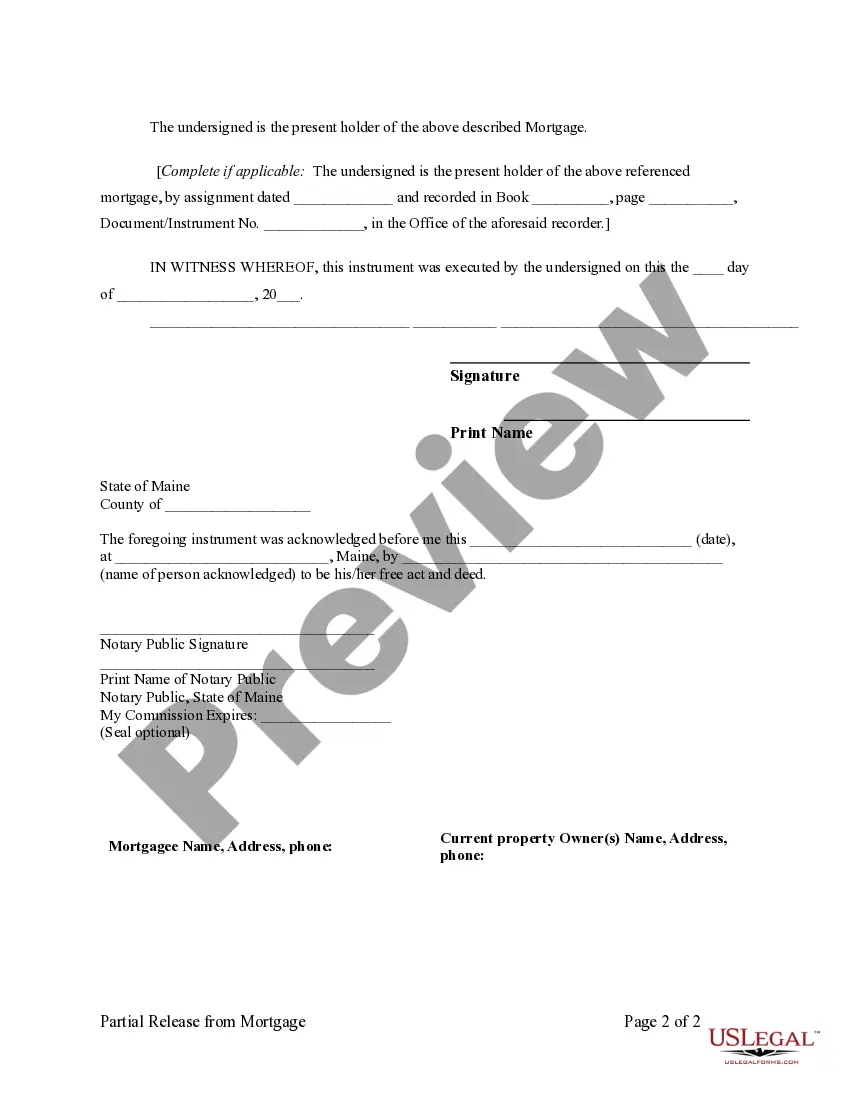

This form is for a holder of a deed of trust or mortgage (see title) to release a portion of the real property described as security. It asserts that the identified an referenced deed of trust or mortgage remains in full force or effect as to the remaining property.

Partial Deed

State:

Maine

Control #:

ME-S124-Z

Format:

Word;

Rich Text

Instant download

Description Allocated Waiver Check Mortgage Example

Free preview Allocated Waiver Mortgage Letter

How to fill out Mortgagee Clause Example?

- If you have previously registered with US Legal Forms, simply log in to your account, ensuring your subscription is active. You can then find and download your desired form by clicking the 'Download' button.

- For first-time users, begin by browsing the extensive online library. Review the preview mode and form description to confirm it meets your needs and complies with local jurisdiction rules.

- If the form doesn’t fit your requirements, utilize the search feature to find a more suitable document. Keep searching until you locate the right template.

- Once you’ve found the correct form, click the 'Buy Now' button and select your preferred subscription plan. You will need to register an account for full library access.

- Proceed to make your purchase by entering your credit card information or using PayPal for payment.

- After purchasing, download the form directly to your device. You can always access this document later from the My Forms section of your profile.

Utilizing US Legal Forms not only provides you with instant access to a vast collection of over 85,000 legal documents but also ensures you can complete your forms confidently, supported by access to premium experts for any assistance you may need.

In conclusion, obtaining the Maine Partial Release of Property From Mortgage by Individual Holder is streamlined with US Legal Forms. Simplify your legal document preparation today and ensure your forms are accurate and compliant!

Allocated Waiver Mortgage Letter Example Form popularity

Property Deed Example Other Form Names

Partial Release Of Mortgage Form

Motor Vehicle Services Allocated Waiver

Allocated Waiver Mortgage Check

Partial Release Clause

What Is A Partial Release

Deed Of Mortgage Sample

Partial Mortgage Release

Partial Lien Release Mortgage FAQ

A partial reconveyance is to reconvey a portion of the land subject to a deed of trust, not the loan amount.He will have to wait to pay off the full loan before the property is granted back to him.

If you are approved for the partial mortgage release, you will receive notification within two to six weeks.

A partial release is a mortgage provision that allows some of the collateral to be released from a mortgage after the borrower pays a certain amount of the loan. Lenders require proof of payment, a survey map, appraisal, and a letter outlining the reason for the partial release.

In most cases, the lien holder (the lender in this case) should send the release to be recorded within 30-90 days. If you aren't sure what the requirements are in your area, reach out to your real estate agent, title agent, or real estate attorney for guidance.

The servicer of a MERS-registered loan has the legal authority to discharge the mortgage on behalf of MERS because, as a member of MERS, authority was granted to their officers through a corporate resolution. The person authorized to sign discharges is sometimes referred to as a certifying officer by MERS.

A Mortgage Release is where you, the homeowner, voluntarily transfer the ownership of your property to the owner of your mortgage in exchange for a release from your mortgage loan and payments.Depending on your situation, you may be required to make a financial contribution to receive a mortgage release.

Partial Release Clause is a provision under which the mortgagee agrees to release certain parcels from the lien of the blanket mortgage upon payment of a certain sum of money by the mortgagor. It's frequently found in tract development construction loans.