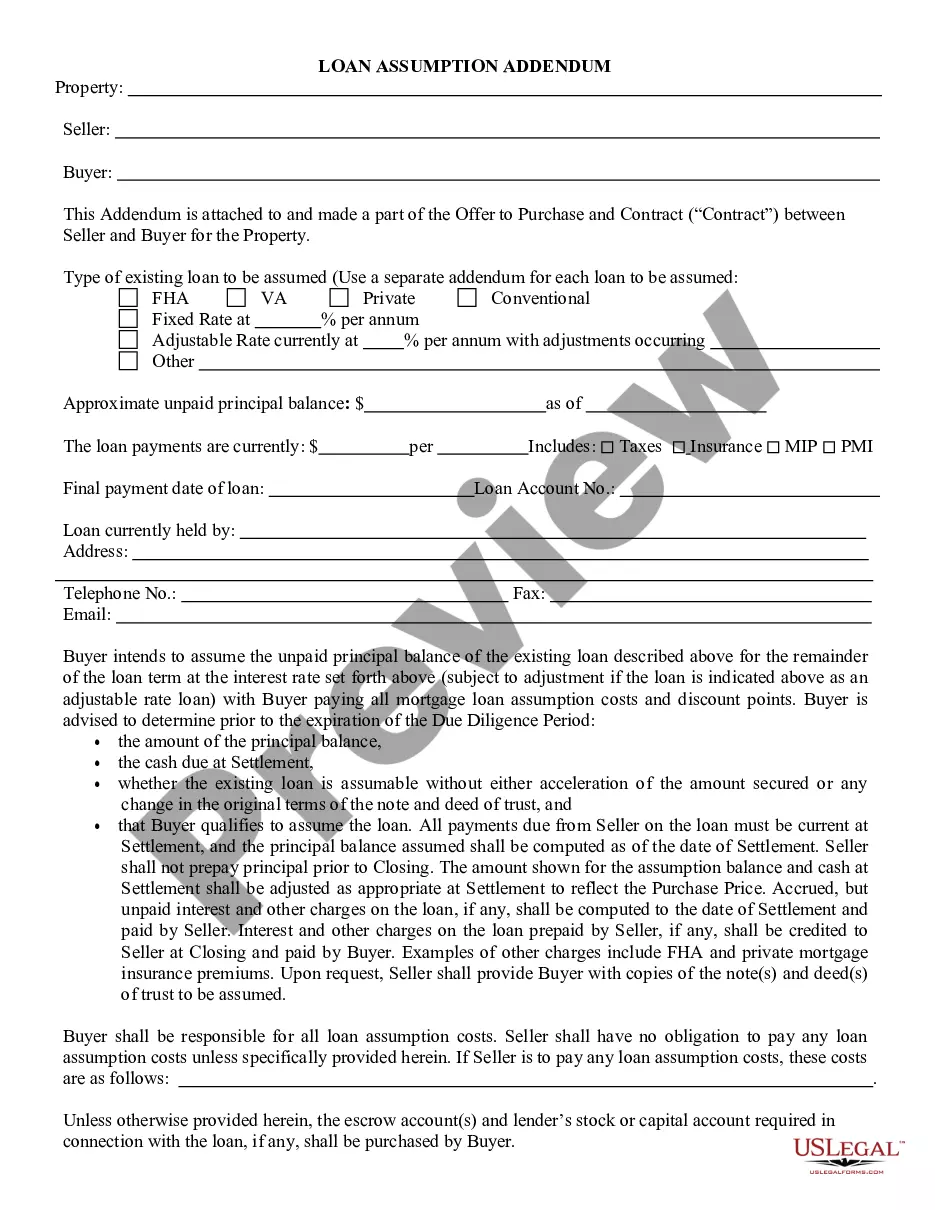

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Maine Loan Assumption Agreement

Category:

State:

Multi-State

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Assumption Agreement?

US Legal Forms - one of the largest collections of legal documents in the USA - provides a variety of legal form templates you can obtain or print. While navigating the website, you will find thousands of forms for business and personal use, categorized by types, states, or keywords. You can locate the latest versions of forms such as the Maine Loan Assumption Agreement in moments.

If you already possess a subscription, Log In and obtain the Maine Loan Assumption Agreement from your US Legal Forms library. The Download button will appear on every form you view. You can access all previously acquired forms from the My documents section of your account.

To utilize US Legal Forms for the first time, here are simple instructions to help you get started: Ensure you have selected the correct form for your city/state. Click the Preview button to review the form's details. Check the form summary to confirm that you have chosen the right form. If the form doesn’t meet your needs, use the Search field at the top of the screen to find one that does. If you are satisfied with the form, confirm your choice by clicking the Purchase now button. Then, select the payment plan you prefer and provide your credentials to register for an account. Process the payment. Use your credit card or PayPal account to finalize the transaction. Choose the format and download the form to your device. Make modifications. Complete, alter, print, and sign the downloaded Maine Loan Assumption Agreement. Every template you added to your account has no expiration date and is yours indefinitely. So, if you wish to obtain or print another copy, simply go to the My documents section and click on the form you need.

- Access the Maine Loan Assumption Agreement with US Legal Forms, the most extensive collection of legal document templates.

- Utilize thousands of professional and state-specific templates that meet your business or personal requirements and needs.

Form popularity

FAQ

"Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility. The word "assumption" is used when a buyer assumes personal liability for an existing debt.

How does the loan assumption process work? Getting approved to assume a loan is similar to getting approved for a new mortgage. You will need to complete an application, provide documents, and meet the lender's credit, income, and financial requirements to get the loan assumption approved.

Most conventional mortgages are not assumable, but many government-backed loans (FHA, VA, USDA) are. The lender must approve you assuming the mortgage, and at the closing, you must compensate the old borrower for the amount they've paid off.

May not be approved: For most assumptions, you'll have to meet the credit qualification standards of the lender and/or investor in the mortgage. There's no guarantee that buyers will be approved.

The Bottom Line. Most FHA, VA and USDA mortgages are easy to assume, though each is treated differently. Some conventional loans are harder to assume. When you assume a mortgage, you take on the exact terms, including the interest rate, monthly payment and any mortgage insurance payment.

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

To assume a loan, the buyer must qualify with the lender. If the price of the house exceeds the remaining mortgage, the buyer must remit a down payment that is the difference between the sale price and the mortgage. If the difference is substantial, the buyer may need to secure a second mortgage.

If the mortgage loan is assumable, a seller can sell their home to a qualified buyer, allowing the buyer to purchase the home by way of assuming responsibility for the seller's loan terms and remaining balance.