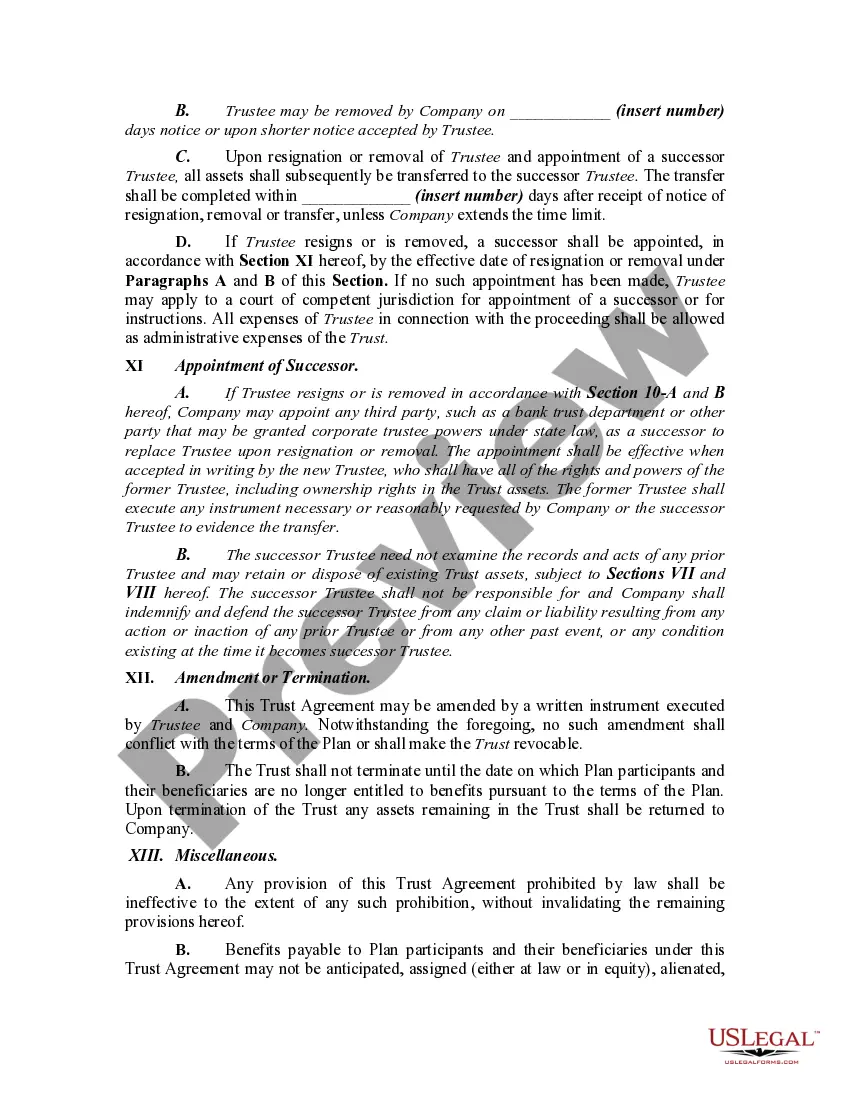

A method of deferring compensation for executives is the use of a rabbi trust. The instrument was named - rabbit trust - because it was first used to provide deferred compensation for a rabbi. Generally, the Internal Revenue Service (IRS) requires that the funds in a rabbi trust must be subject to the claims of the employer's creditors.

This information is current as of December, 2007, but is subject to change if tax laws or IRS regulations change. Current tax laws should be consulted at the time of the preparation of such a trust.

Maine Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees — a Rabbi Trust is a type of trust established for the purpose of providing nonqualified deferred compensation benefits to executive employees in the state of Maine. It operates under the provisions outlined in the Employee Retirement Income Security Act (ERICA) and offers certain tax advantages to both the employer and the employee. This specific type of trust is referred to as a "Rabbi Trust" because it derives its name from a landmark court case involving a rabbi and his deferred compensation. It has since become a popular term used to describe trusts that offer benefits similar to these. The Maine Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees — a Rabbi Trust is designed to allow executive employees to defer a portion of their compensation, such as salary, bonuses, or stock options, until a later date, typically retirement. By deferring this income, employees have the opportunity to potentially grow their savings and defer the associated taxes. Moreover, this trust is subject to ERICA regulations, which means it must meet certain qualification criteria to ensure that the deferred compensation remains protected for the employees until it is distributed. These criteria primarily focus on providing adequate funding and adhering to specific rules relating to vesting, distribution, and taxation. While the specific details may vary based on the employer's plan, there are generally two main types of Maine Nonqualified Deferred Compensation Trusts — Restricted and Unrestricted. A restricted trust typically imposes limitations on the timing and conditions for access to the deferred funds, such as reaching a specific age or retiring from the company. Meanwhile, an unrestricted trust offers more flexibility, allowing employees to access their deferred compensation at any time, subject to certain restrictions. In summary, the Maine Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees — a Rabbi Trust is a trust designed to provide executive employees in Maine with the opportunity to defer a portion of their compensation until a future date, usually retirement. It offers tax advantages and operates under ERICA regulations to protect the deferred funds. The trust may be categorized as either restricted or unrestricted, depending on the specific access and distribution conditions.