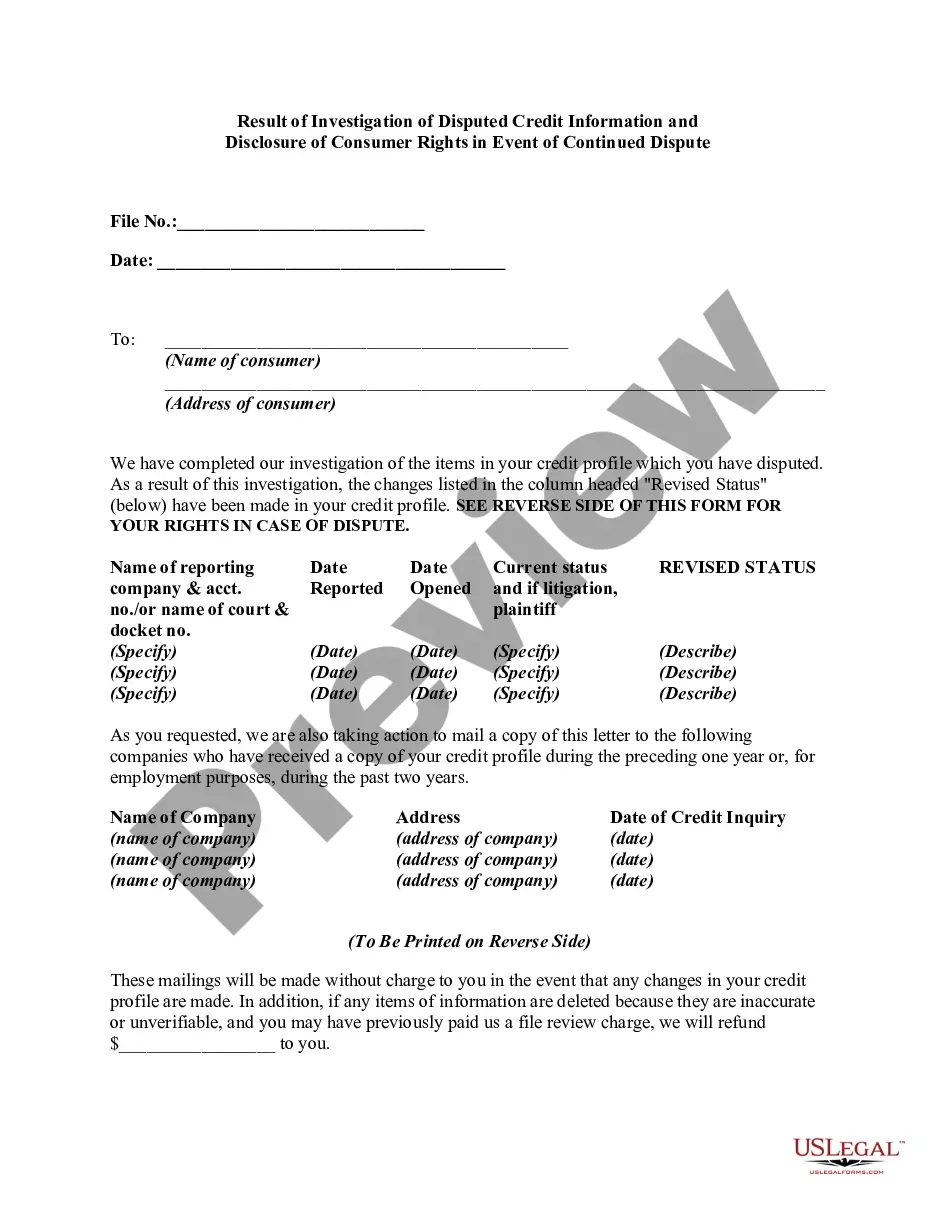

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

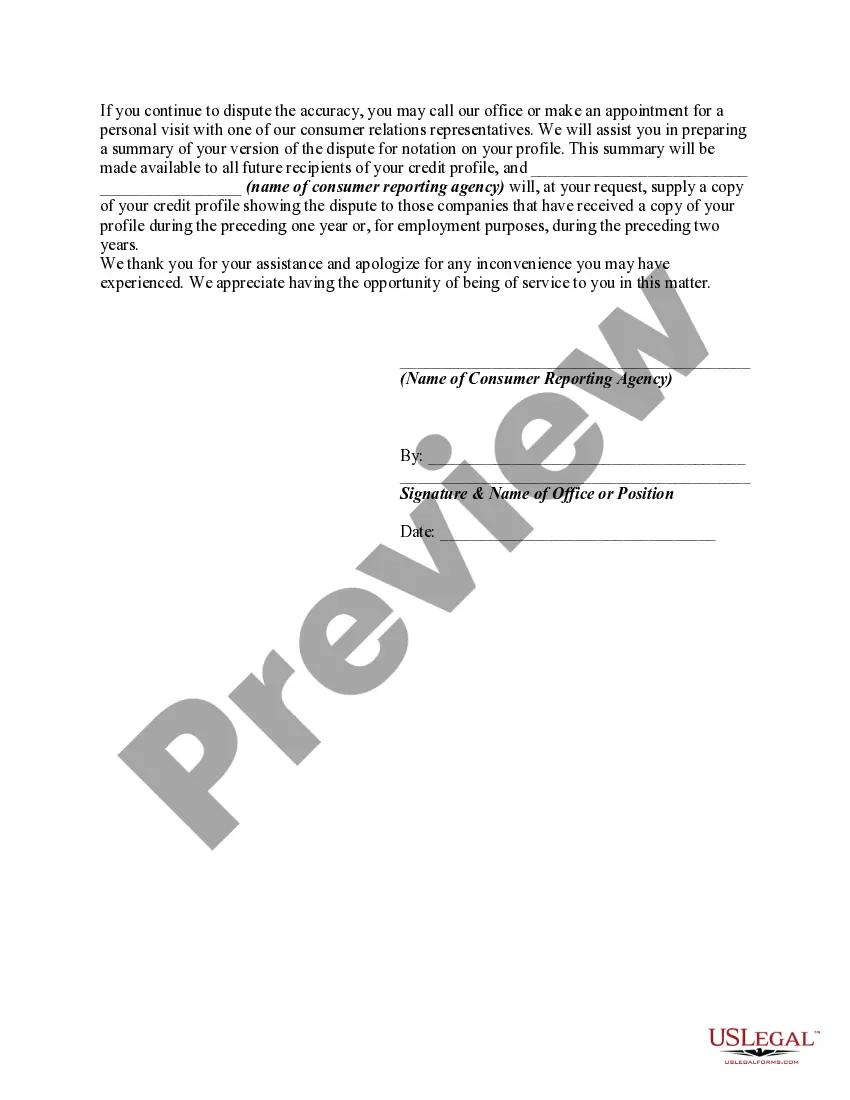

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Maine has specific laws and regulations in place to protect consumers when it comes to disputed credit information and the disclosure of consumer rights. In the event of a dispute regarding credit information, consumers in Maine have the right to a thorough investigation to determine the accuracy of the reported information. The result of an investigation of disputed credit information in Maine can vary depending on the specific circumstances of the case. If the investigation reveals that the reported information is indeed inaccurate, the credit reporting agency (CRA) must promptly correct or delete the erroneous information from the consumer's credit report. This ensures that the consumer's credit history is accurately reflected. On the other hand, if the investigation determines that the disputed credit information is accurate, the consumer has the right to add a brief statement to their credit report explaining their position. This allows consumers to provide context or additional information regarding the negative credit information. Maine also emphasizes the importance of disclosure of consumer rights in the event of a continued dispute. When a consumer files a dispute with a CRA, the CRA must inform the consumer about their rights and provide them with a summary of the Fair Credit Reporting Act (FCRA). This summary outlines the consumer's rights, such as the right to a free annual credit report, the right to dispute inaccurate information, and the right to contact the CRA regarding the investigation's results. It is crucial for consumers to understand their rights and take appropriate action if they believe their credit information is inaccurate or if the investigation does not yield a satisfactory result. By familiarizing themselves with the laws and regulations in Maine and staying proactive, consumers can protect their credit standing and ensure the accuracy of their credit reports. In summary, in Maine, the result of an investigation of disputed credit information can lead to either the correction or deletion of inaccurate information or the addition of a consumer's statement providing context. Regardless of the outcome, consumers must be aware of their rights and take appropriate action to protect their credit standing.Maine has specific laws and regulations in place to protect consumers when it comes to disputed credit information and the disclosure of consumer rights. In the event of a dispute regarding credit information, consumers in Maine have the right to a thorough investigation to determine the accuracy of the reported information. The result of an investigation of disputed credit information in Maine can vary depending on the specific circumstances of the case. If the investigation reveals that the reported information is indeed inaccurate, the credit reporting agency (CRA) must promptly correct or delete the erroneous information from the consumer's credit report. This ensures that the consumer's credit history is accurately reflected. On the other hand, if the investigation determines that the disputed credit information is accurate, the consumer has the right to add a brief statement to their credit report explaining their position. This allows consumers to provide context or additional information regarding the negative credit information. Maine also emphasizes the importance of disclosure of consumer rights in the event of a continued dispute. When a consumer files a dispute with a CRA, the CRA must inform the consumer about their rights and provide them with a summary of the Fair Credit Reporting Act (FCRA). This summary outlines the consumer's rights, such as the right to a free annual credit report, the right to dispute inaccurate information, and the right to contact the CRA regarding the investigation's results. It is crucial for consumers to understand their rights and take appropriate action if they believe their credit information is inaccurate or if the investigation does not yield a satisfactory result. By familiarizing themselves with the laws and regulations in Maine and staying proactive, consumers can protect their credit standing and ensure the accuracy of their credit reports. In summary, in Maine, the result of an investigation of disputed credit information can lead to either the correction or deletion of inaccurate information or the addition of a consumer's statement providing context. Regardless of the outcome, consumers must be aware of their rights and take appropriate action to protect their credit standing.