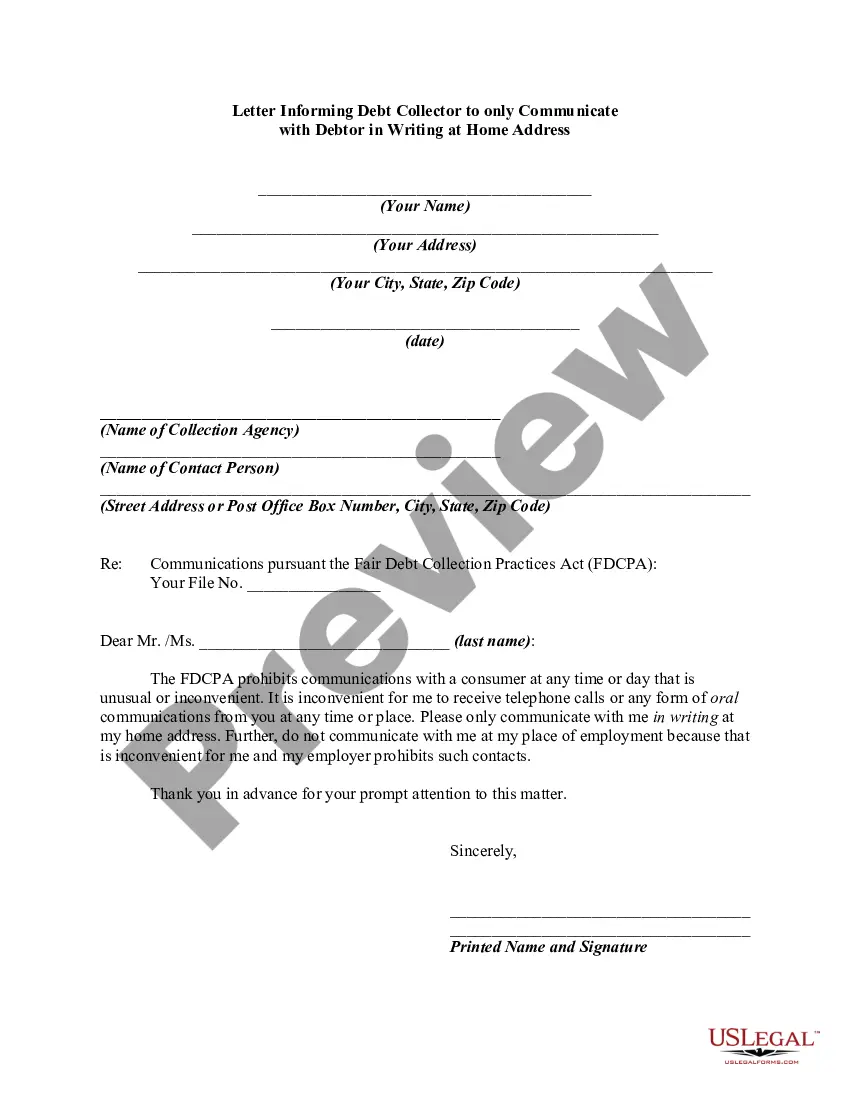

The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. This Act sets forth strict rules regarding communicating with the debtor.

The collector is restricted in the type of contact he can make with the debtor. He can't contact the debtor before 8:00 a.m. or after 9:00 p.m. He can contact the debtor at home, but cannot contact the debtor at the debtor's club or church or at a school meeting of some sort. The debtor cannot be contacted at work if his employer objects. If the debtor tells the creditor the name of his attorney, any future contacts must be made with the attorney and not with the debtor.

Maine Letter Informing Debt Collector to only Communicate with Debtor in Writing at Debtor's Home Address is a legal document designed to ensure that a debtor's rights are protected when dealing with debt collection agencies. This letter requests that all communication regarding the debt be made in writing and sent to the debtor's home address. By sending this letter, the debtor aims to limit any harassment or intimidation tactics commonly employed by debt collectors. The main intent is to assert control over the communication process and reduce the constant phone calls or in-person visits that can be overwhelming and stressful. It is important to note that there may be variations of the Maine Letter Informing Debt Collector to only Communicate with Debtor in Writing at Debtor's Home Address, depending on specific circumstances. Some examples include: 1. Initial Notice: This letter serves as the first communication to the debt collector, informing them of the debtor's preference for written communication only. It is crucial to mention the relevant laws that support this request and any specific details related to the debt. 2. Cease and Desist: If the debt collector continues to contact the debtor via phone calls or in-person visits after receiving the initial notice, this letter can be sent to demand an immediate stop to all communication that violates the debtor's rights. This letter may include references to the Fair Debt Collection Practices Act (FD CPA) and any other state-specific laws. 3. Validation Request: If the debtor believes the debt is inaccurate or wishes to seek validation of the debt amount and ownership, this letter can be sent. It requests the debt collector to provide detailed documentation verifying the debt, including the original creditor's name, account number, and any other relevant information. 4. Dispute: In cases where the debtor disputes the validity of the debt, a dispute letter can be sent. This letter informs the debt collector of the debtor's disagreement with the debt and requests that they cease all collection activities until the matter is resolved. It is essential to consult with a legal professional or use trusted templates specific to Maine to ensure compliance with state laws when drafting any of these letters.Maine Letter Informing Debt Collector to only Communicate with Debtor in Writing at Debtor's Home Address is a legal document designed to ensure that a debtor's rights are protected when dealing with debt collection agencies. This letter requests that all communication regarding the debt be made in writing and sent to the debtor's home address. By sending this letter, the debtor aims to limit any harassment or intimidation tactics commonly employed by debt collectors. The main intent is to assert control over the communication process and reduce the constant phone calls or in-person visits that can be overwhelming and stressful. It is important to note that there may be variations of the Maine Letter Informing Debt Collector to only Communicate with Debtor in Writing at Debtor's Home Address, depending on specific circumstances. Some examples include: 1. Initial Notice: This letter serves as the first communication to the debt collector, informing them of the debtor's preference for written communication only. It is crucial to mention the relevant laws that support this request and any specific details related to the debt. 2. Cease and Desist: If the debt collector continues to contact the debtor via phone calls or in-person visits after receiving the initial notice, this letter can be sent to demand an immediate stop to all communication that violates the debtor's rights. This letter may include references to the Fair Debt Collection Practices Act (FD CPA) and any other state-specific laws. 3. Validation Request: If the debtor believes the debt is inaccurate or wishes to seek validation of the debt amount and ownership, this letter can be sent. It requests the debt collector to provide detailed documentation verifying the debt, including the original creditor's name, account number, and any other relevant information. 4. Dispute: In cases where the debtor disputes the validity of the debt, a dispute letter can be sent. This letter informs the debt collector of the debtor's disagreement with the debt and requests that they cease all collection activities until the matter is resolved. It is essential to consult with a legal professional or use trusted templates specific to Maine to ensure compliance with state laws when drafting any of these letters.