A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

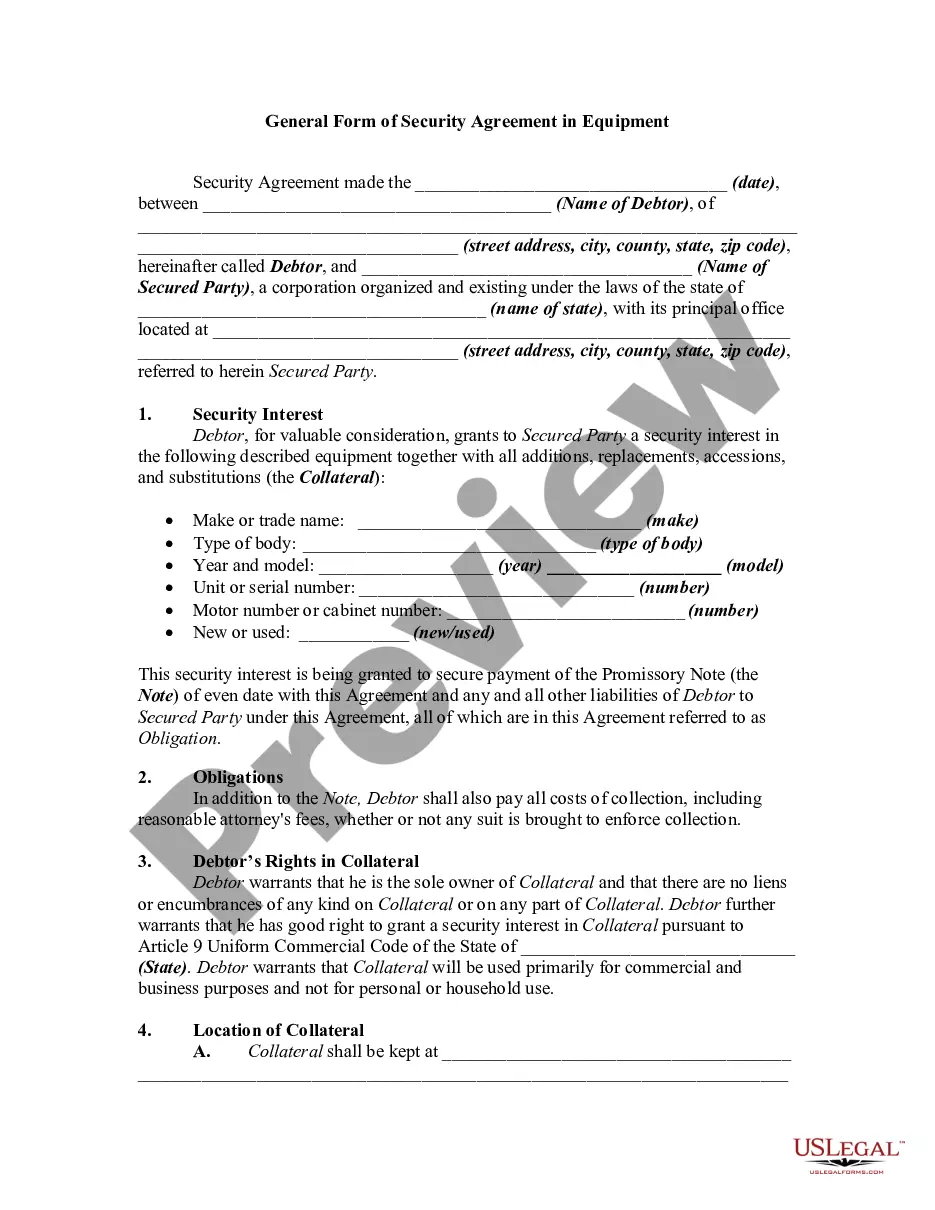

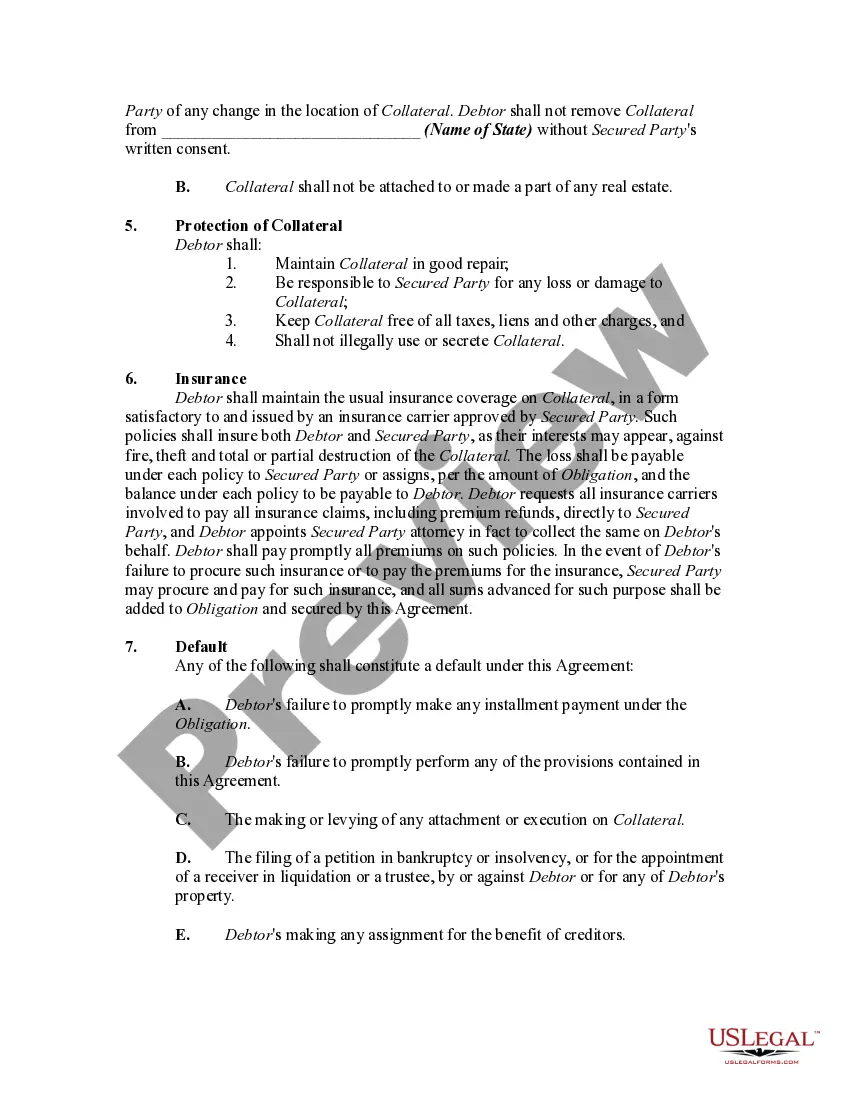

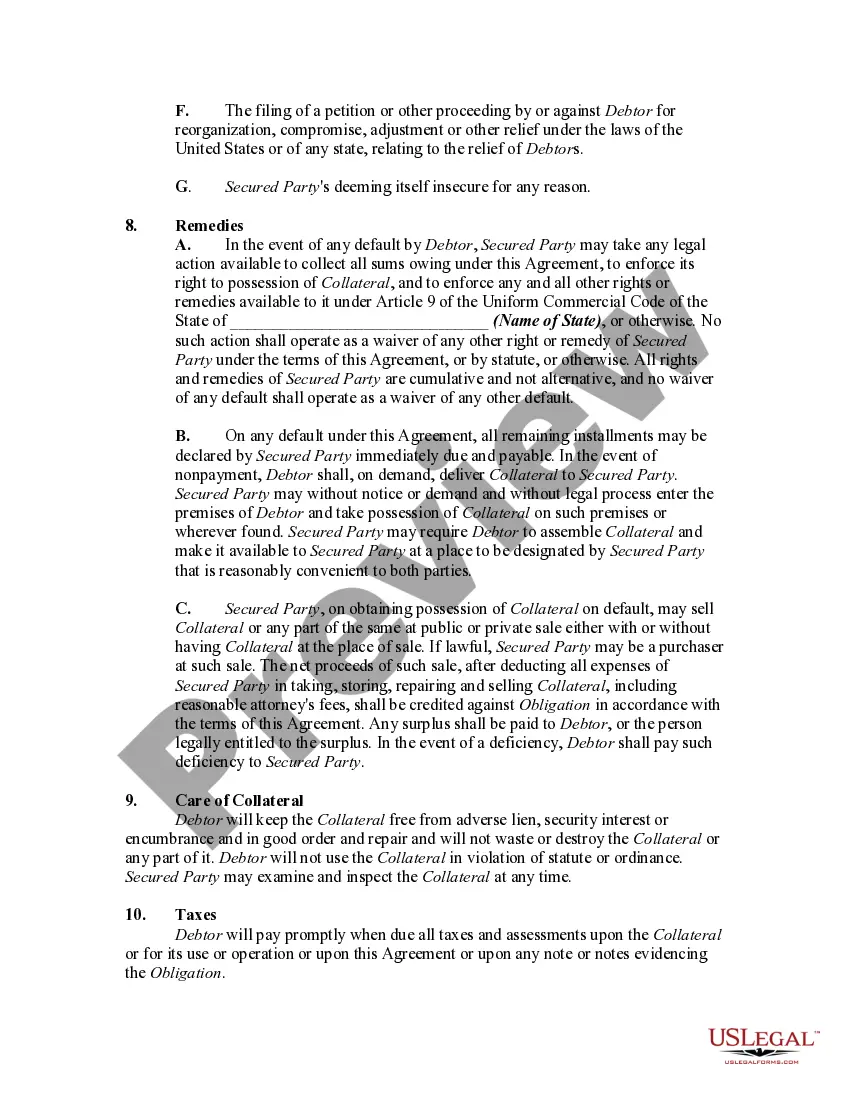

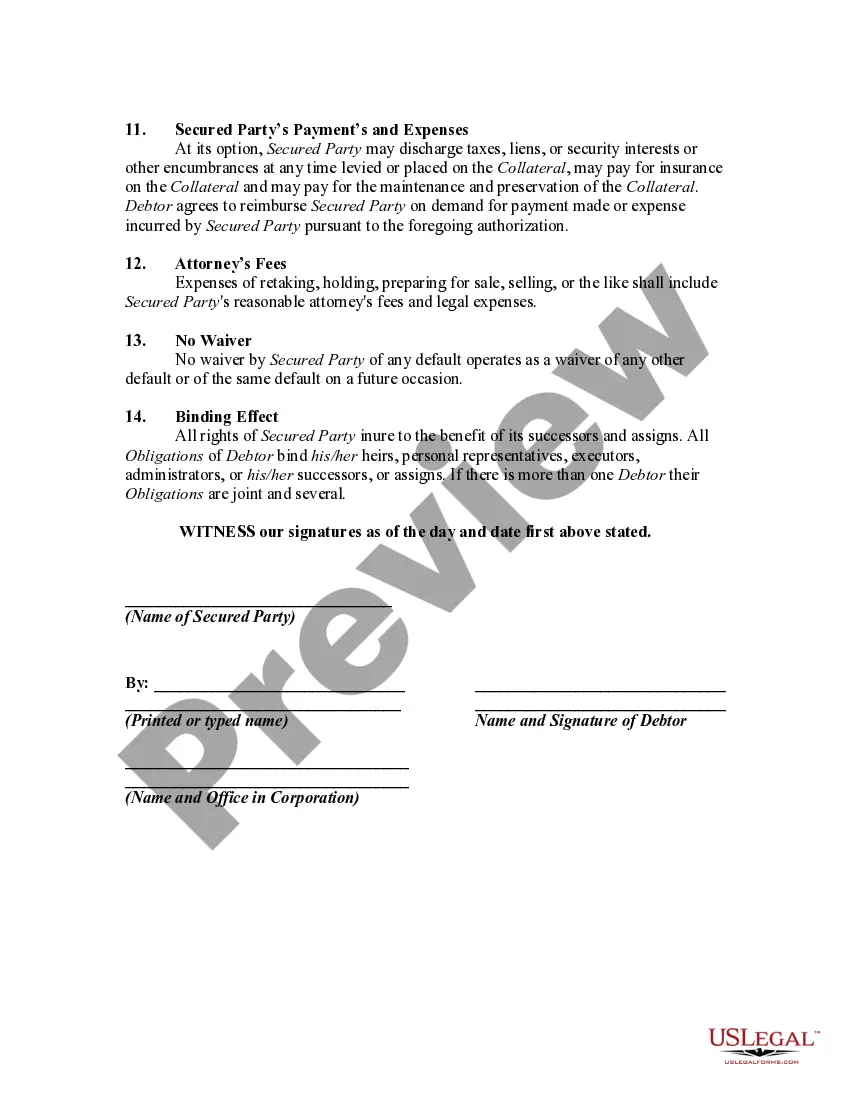

A Maine General Form of Security Agreement in Equipment is a legally binding document that establishes a security interest in equipment. This agreement is commonly used in commercial transactions where the equipment serves as collateral for a loan or credit. It outlines the terms and conditions under which the equipment can be used as security, ensuring the creditor's rights in case the debtor defaults on their obligations. The Maine General Form of Security Agreement in Equipment typically includes keywords such as: 1. Equipment description: This part of the agreement provides a detailed description of the equipment being used as collateral, including its make, model, serial number, and any other identifying features. 2. Parties involved: It identifies the parties to the agreement, namely the debtor (the party providing the equipment as collateral) and the creditor (the party who holds the security interest). 3. Representations and warranties: This section includes statements made by the debtor regarding the ownership, condition, and value of the equipment. It ensures that the debtor has the right to grant the security interest and that the equipment is free from any other liens or encumbrances. 4. Permitted use and maintenance: The agreement may outline specific conditions or limitations regarding how the debtor can use and maintain the equipment. This ensures that the equipment remains in good working condition and preserves its value. 5. Default and remedies: The agreement specifies the events that would constitute a default, such as failure to make payments or breach of other terms. It also lists the remedies available to the creditor in case of default, which may include repossession, sale, or legal action. 6. Indemnification and insurance: This section addresses the debtor's obligation to maintain insurance coverage on the equipment and indemnify the creditor against any loss, damage, or liability arising from its use. 7. Governing law and jurisdiction: The agreement may include clauses stating that Maine law applies and designating the courts or arbitration forums where disputes will be resolved. Different types of Maine General Form of Security Agreements in Equipment may include variations specific to certain industries or purposes. For example, there might be separate agreements for construction equipment, manufacturing machinery, or medical devices. It is important to use the appropriate form depending on the type of equipment involved to ensure accurate and comprehensive coverage.A Maine General Form of Security Agreement in Equipment is a legally binding document that establishes a security interest in equipment. This agreement is commonly used in commercial transactions where the equipment serves as collateral for a loan or credit. It outlines the terms and conditions under which the equipment can be used as security, ensuring the creditor's rights in case the debtor defaults on their obligations. The Maine General Form of Security Agreement in Equipment typically includes keywords such as: 1. Equipment description: This part of the agreement provides a detailed description of the equipment being used as collateral, including its make, model, serial number, and any other identifying features. 2. Parties involved: It identifies the parties to the agreement, namely the debtor (the party providing the equipment as collateral) and the creditor (the party who holds the security interest). 3. Representations and warranties: This section includes statements made by the debtor regarding the ownership, condition, and value of the equipment. It ensures that the debtor has the right to grant the security interest and that the equipment is free from any other liens or encumbrances. 4. Permitted use and maintenance: The agreement may outline specific conditions or limitations regarding how the debtor can use and maintain the equipment. This ensures that the equipment remains in good working condition and preserves its value. 5. Default and remedies: The agreement specifies the events that would constitute a default, such as failure to make payments or breach of other terms. It also lists the remedies available to the creditor in case of default, which may include repossession, sale, or legal action. 6. Indemnification and insurance: This section addresses the debtor's obligation to maintain insurance coverage on the equipment and indemnify the creditor against any loss, damage, or liability arising from its use. 7. Governing law and jurisdiction: The agreement may include clauses stating that Maine law applies and designating the courts or arbitration forums where disputes will be resolved. Different types of Maine General Form of Security Agreements in Equipment may include variations specific to certain industries or purposes. For example, there might be separate agreements for construction equipment, manufacturing machinery, or medical devices. It is important to use the appropriate form depending on the type of equipment involved to ensure accurate and comprehensive coverage.