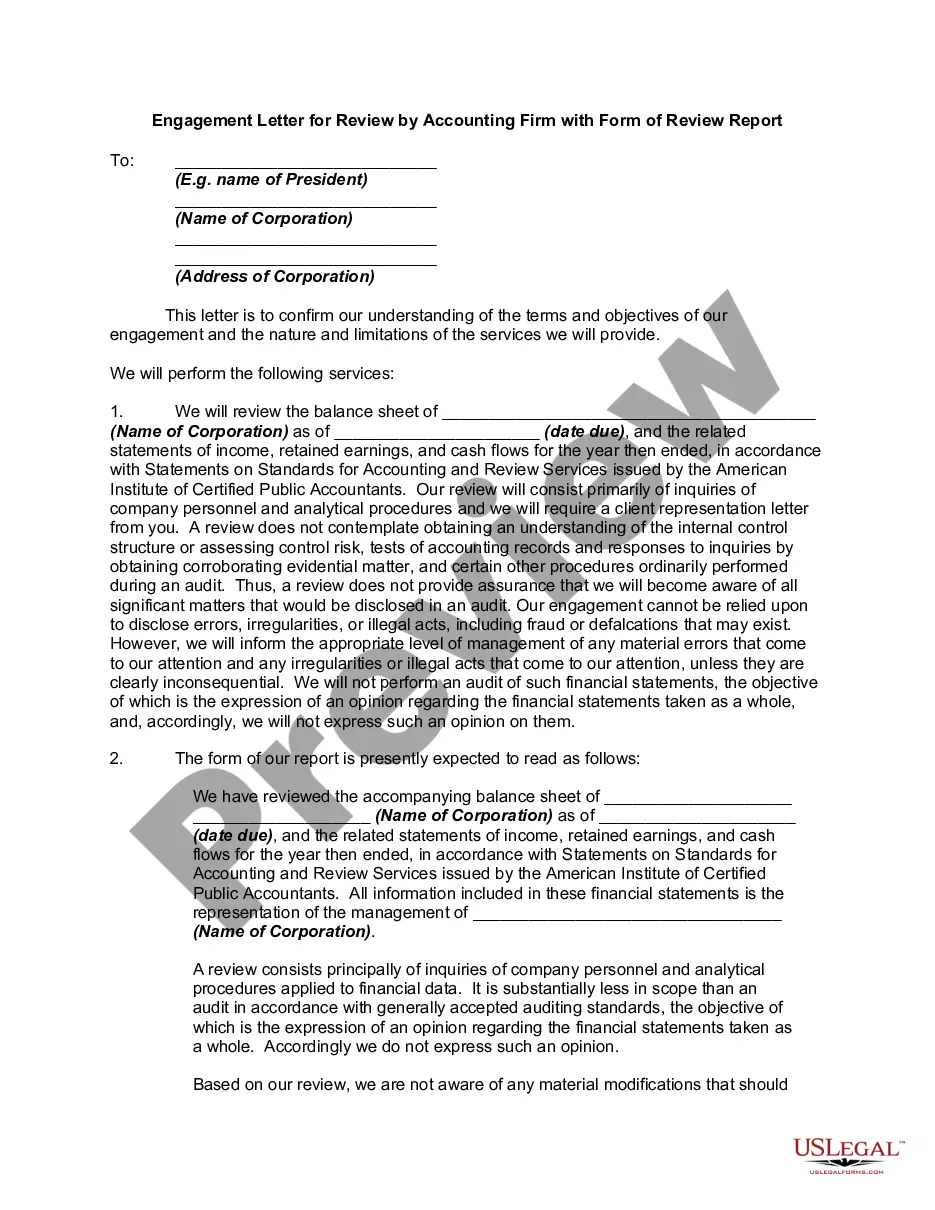

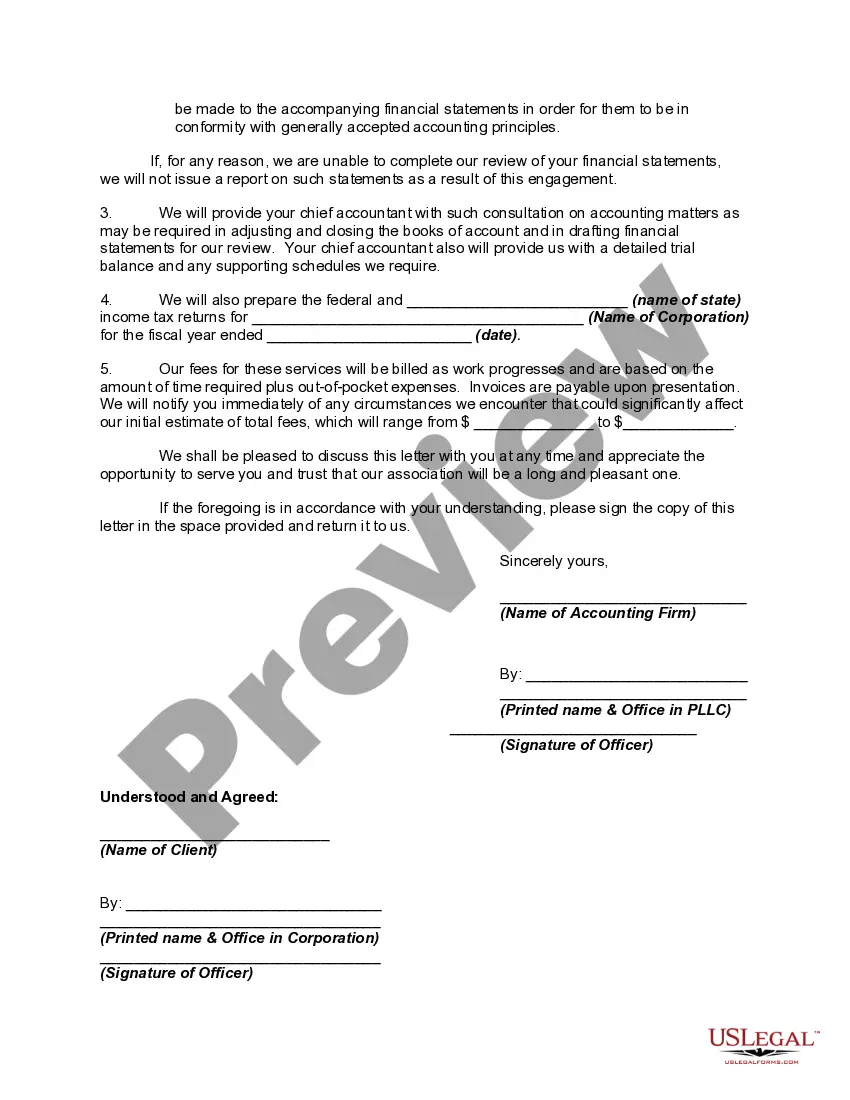

Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Maine Engagement Letter for Review by Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions of an engagement between the accounting firm and its client to perform a review of their financial statements. This engagement letter holds significant importance in the accounting profession as it establishes the scope of work, responsibilities, and expectations of both the client and the accounting firm. The Maine Engagement Letter for Review typically includes the following key components: 1. Background Information: This section includes the name and address of the accounting firm, the client's name and address, and a brief description of the client's business. 2. Objective of the Engagement: The engagement letter clearly states the purpose of the review engagement, which is usually to express limited assurance on the financial statements to provide users with credibility and reliability. 3. Scope of the Engagement: This section outlines the specific procedures that the accounting firm will perform during the review process. It should explicitly state that a review is substantially less in scope than an audit and that the firm's objective is to assess whether the financial statements are plausible and free from material misstatements. 4. Responsibilities of the Accounting Firm: This section describes the responsibilities of the accounting firm, which may include conducting the review in accordance with Generally Accepted Review Standards (GARS) and obtaining an understanding of the client's industry and business operations. 5. Responsibilities of the Client: The engagement letter highlights the client's responsibilities, including providing accurate and complete financial information, granting access to relevant records and personnel, and informing the accounting firm about any potential fraud or errors. 6. Timelines and Deadlines: This section specifies the commencement date of the engagement, the duration of the review process, and the expected dates for the completion of various review procedures. 7. Confidentiality and Data Security: This section ensures the client that the accounting firm will maintain the confidentiality of all client information and outlines the steps taken to safeguard data against unauthorized access or disclosure. 8. Fees and Billing Terms: The engagement letter discusses the compensation structure, expenses, and billing terms, including the basis for fees calculation, payment due dates, and any additional costs to be billed separately. Different types of Maine Engagement Letters for Review by an Accounting Firm with Form of Review Report may include: 1. Standard Engagement Letter for Review: This is the most commonly used engagement letter for review services in Maine, covering the general terms and conditions outlined above. 2. Limited Scope Review Engagement Letter: This type of engagement letter is used when the scope of the review engagement is limited to specific sections or accounts of the financial statements, rather than a comprehensive review. 3. Industry-Specific Review Engagement Letter: In cases where the client operates in a specific industry with unique accounting requirements, an engagement letter tailored to that industry may be used. This ensures that the accounting firm understands and addresses industry-specific considerations. In conclusion, the Maine Engagement Letter for Review by Accounting Firm with Form of Review Report is a critical document that sets the framework and expectations for the review engagement process between the accounting firm and its client. It outlines the scope, responsibilities, timelines, and fees associated with the review engagement to ensure transparency and clarity between both parties.Maine Engagement Letter for Review by Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions of an engagement between the accounting firm and its client to perform a review of their financial statements. This engagement letter holds significant importance in the accounting profession as it establishes the scope of work, responsibilities, and expectations of both the client and the accounting firm. The Maine Engagement Letter for Review typically includes the following key components: 1. Background Information: This section includes the name and address of the accounting firm, the client's name and address, and a brief description of the client's business. 2. Objective of the Engagement: The engagement letter clearly states the purpose of the review engagement, which is usually to express limited assurance on the financial statements to provide users with credibility and reliability. 3. Scope of the Engagement: This section outlines the specific procedures that the accounting firm will perform during the review process. It should explicitly state that a review is substantially less in scope than an audit and that the firm's objective is to assess whether the financial statements are plausible and free from material misstatements. 4. Responsibilities of the Accounting Firm: This section describes the responsibilities of the accounting firm, which may include conducting the review in accordance with Generally Accepted Review Standards (GARS) and obtaining an understanding of the client's industry and business operations. 5. Responsibilities of the Client: The engagement letter highlights the client's responsibilities, including providing accurate and complete financial information, granting access to relevant records and personnel, and informing the accounting firm about any potential fraud or errors. 6. Timelines and Deadlines: This section specifies the commencement date of the engagement, the duration of the review process, and the expected dates for the completion of various review procedures. 7. Confidentiality and Data Security: This section ensures the client that the accounting firm will maintain the confidentiality of all client information and outlines the steps taken to safeguard data against unauthorized access or disclosure. 8. Fees and Billing Terms: The engagement letter discusses the compensation structure, expenses, and billing terms, including the basis for fees calculation, payment due dates, and any additional costs to be billed separately. Different types of Maine Engagement Letters for Review by an Accounting Firm with Form of Review Report may include: 1. Standard Engagement Letter for Review: This is the most commonly used engagement letter for review services in Maine, covering the general terms and conditions outlined above. 2. Limited Scope Review Engagement Letter: This type of engagement letter is used when the scope of the review engagement is limited to specific sections or accounts of the financial statements, rather than a comprehensive review. 3. Industry-Specific Review Engagement Letter: In cases where the client operates in a specific industry with unique accounting requirements, an engagement letter tailored to that industry may be used. This ensures that the accounting firm understands and addresses industry-specific considerations. In conclusion, the Maine Engagement Letter for Review by Accounting Firm with Form of Review Report is a critical document that sets the framework and expectations for the review engagement process between the accounting firm and its client. It outlines the scope, responsibilities, timelines, and fees associated with the review engagement to ensure transparency and clarity between both parties.