Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

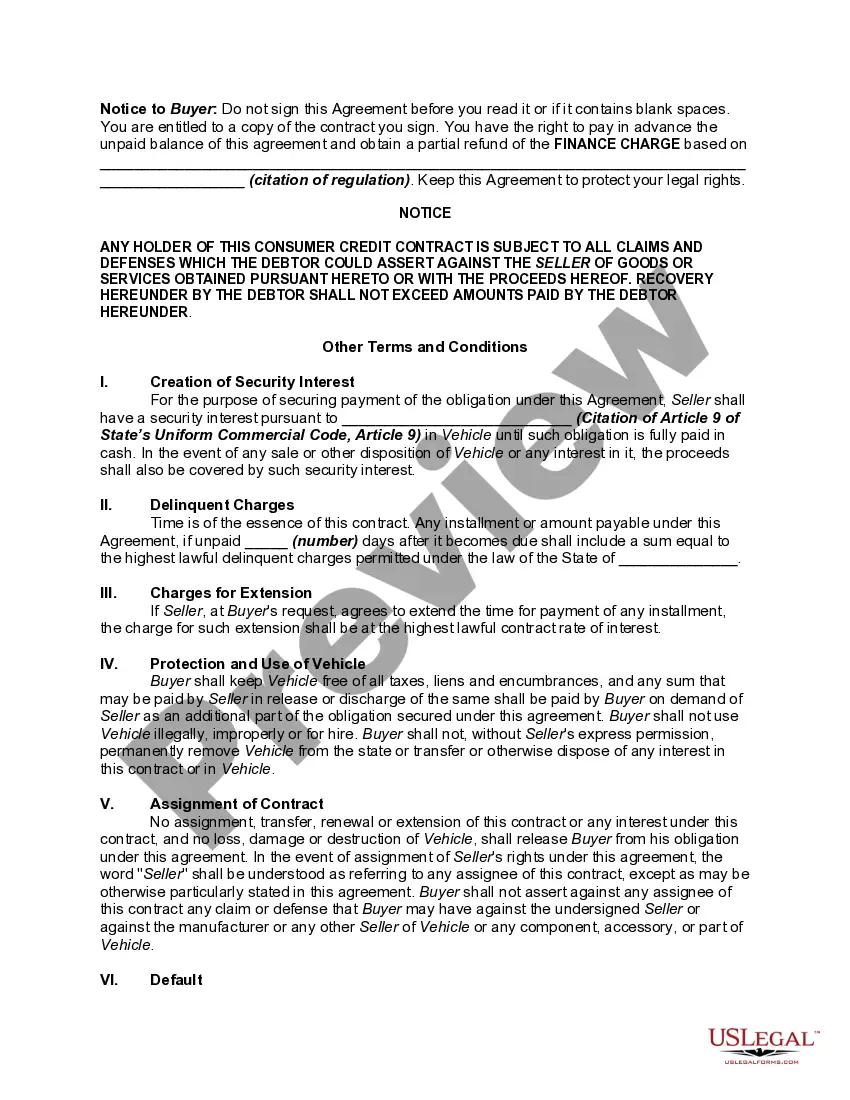

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

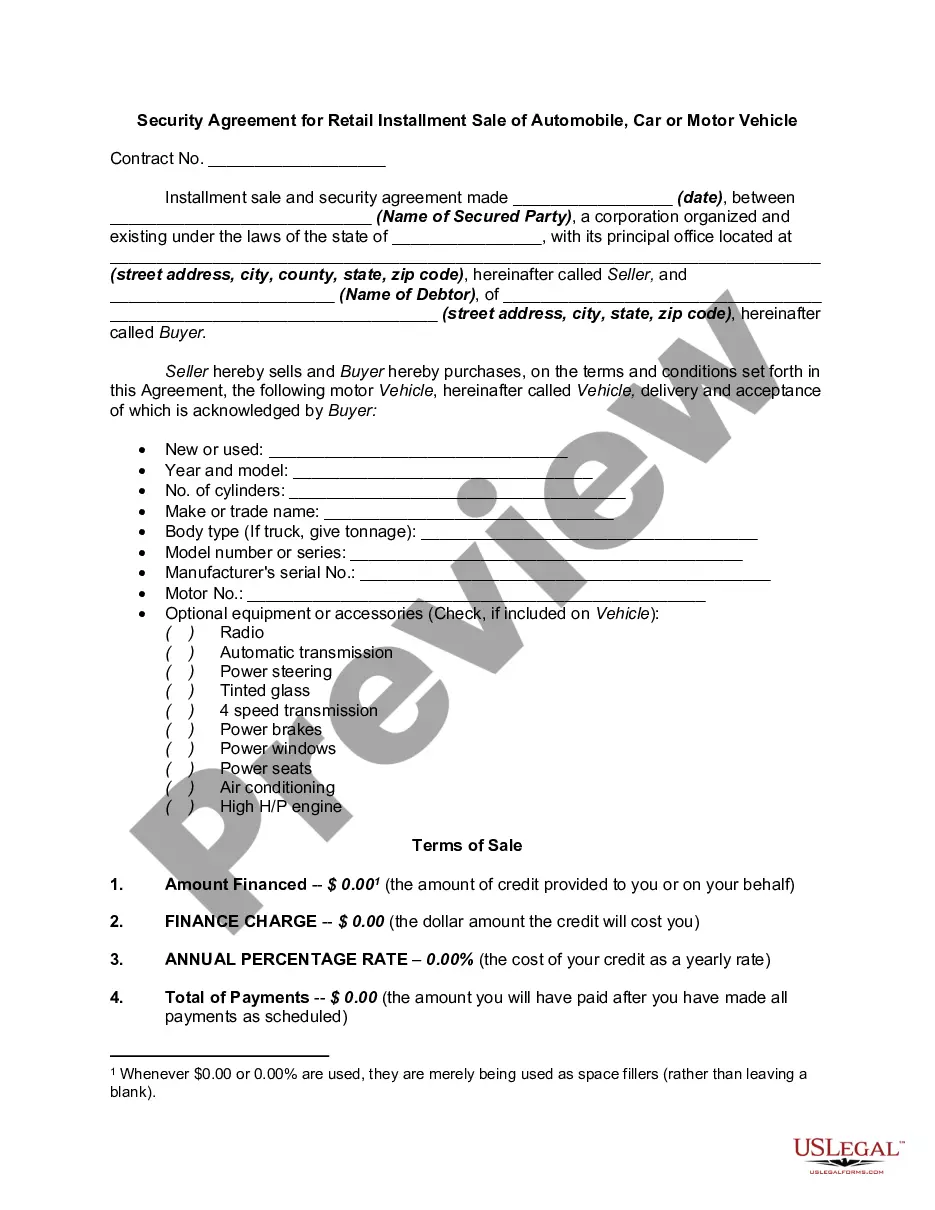

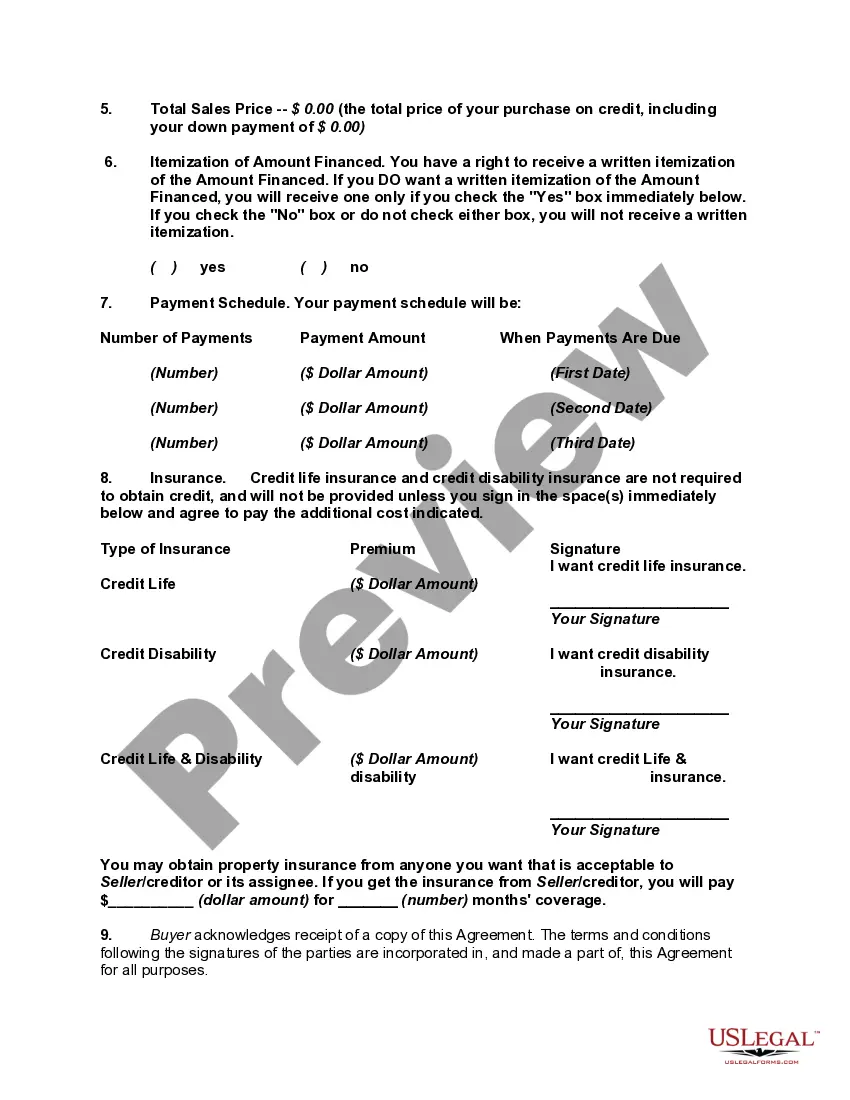

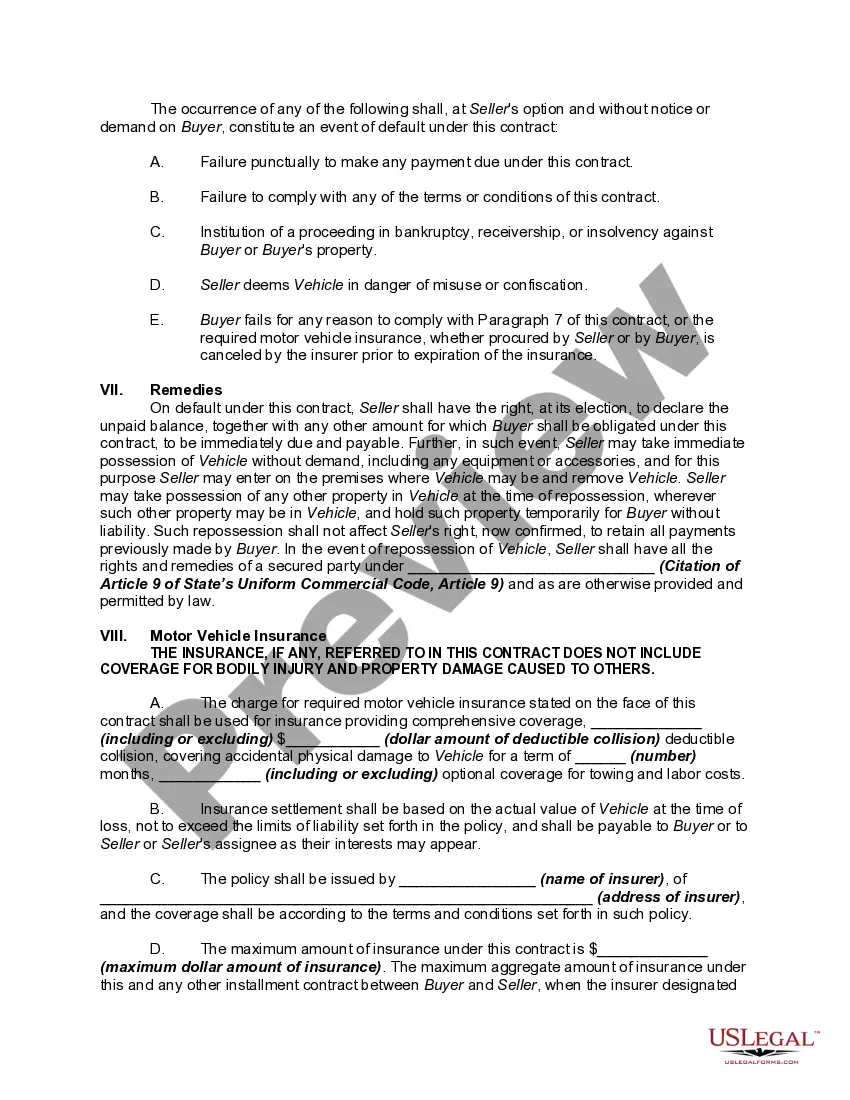

Title: Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle — A Comprehensive Overview Introduction: The Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legal document that outlines the terms and conditions of a financing arrangement for purchasing a vehicle in Maine. This agreement serves as a security measure to protect the lender's interest in the vehicle until the borrower completes the repayment of the loan. Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle Types: While there may not be distinct types of security agreements specific to Maine, the state does require adhering to certain regulations when drafting these agreements. Lenders may have their own unique templates or variations, but the primary purpose and elements remain the same. Key Elements of a Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle: 1. Parties Involved: The agreement names the parties involved: the lender (secured party) and the borrower (debtor). It also outlines their legal addresses for official correspondence. 2. Vehicle Description: Accurate details of the vehicle are included, such as make, model, year, Vehicle Identification Number (VIN), and license plate information. This ensures that the collateral is specifically identified within the agreement. 3. Terms and Conditions: The agreement outlines the terms and conditions of the sale, including the total purchase price, the amount financed, interest rate, payment schedule, and duration of the loan. It may also mention any late payment penalties, prepayment penalties, or grace periods. 4. Loan Security: The primary purpose of the security agreement is to establish the vehicle as collateral for the loan. It specifies that the borrower grants the lender a security interest in the vehicle until the loan is fully paid. This allows the lender the right to repossess the vehicle in case of default or non-payment. 5. Insurance Requirements: To protect both parties, the agreement often stipulates that the borrower must maintain comprehensive and collision insurance coverage throughout the loan term, naming the lender as a loss payee. 6. Default and Repossession: The agreement defines the terms under which the borrower will be deemed in default (e.g., missed payments) and the lender's rights in the event of default. It may describe the repossession process, creditor's right to access the vehicle, and the rights of the borrower during the repossession process. Conclusion: The Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a crucial legal document used to finance vehicle purchases. It ensures that both the lender and borrower understand their rights and obligations. While there may not be distinct types of Maine security agreements, adhering to the state's regulations and including the aforementioned key elements is vital for a secure and lawful transaction.Title: Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle — A Comprehensive Overview Introduction: The Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legal document that outlines the terms and conditions of a financing arrangement for purchasing a vehicle in Maine. This agreement serves as a security measure to protect the lender's interest in the vehicle until the borrower completes the repayment of the loan. Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle Types: While there may not be distinct types of security agreements specific to Maine, the state does require adhering to certain regulations when drafting these agreements. Lenders may have their own unique templates or variations, but the primary purpose and elements remain the same. Key Elements of a Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle: 1. Parties Involved: The agreement names the parties involved: the lender (secured party) and the borrower (debtor). It also outlines their legal addresses for official correspondence. 2. Vehicle Description: Accurate details of the vehicle are included, such as make, model, year, Vehicle Identification Number (VIN), and license plate information. This ensures that the collateral is specifically identified within the agreement. 3. Terms and Conditions: The agreement outlines the terms and conditions of the sale, including the total purchase price, the amount financed, interest rate, payment schedule, and duration of the loan. It may also mention any late payment penalties, prepayment penalties, or grace periods. 4. Loan Security: The primary purpose of the security agreement is to establish the vehicle as collateral for the loan. It specifies that the borrower grants the lender a security interest in the vehicle until the loan is fully paid. This allows the lender the right to repossess the vehicle in case of default or non-payment. 5. Insurance Requirements: To protect both parties, the agreement often stipulates that the borrower must maintain comprehensive and collision insurance coverage throughout the loan term, naming the lender as a loss payee. 6. Default and Repossession: The agreement defines the terms under which the borrower will be deemed in default (e.g., missed payments) and the lender's rights in the event of default. It may describe the repossession process, creditor's right to access the vehicle, and the rights of the borrower during the repossession process. Conclusion: The Maine Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a crucial legal document used to finance vehicle purchases. It ensures that both the lender and borrower understand their rights and obligations. While there may not be distinct types of Maine security agreements, adhering to the state's regulations and including the aforementioned key elements is vital for a secure and lawful transaction.