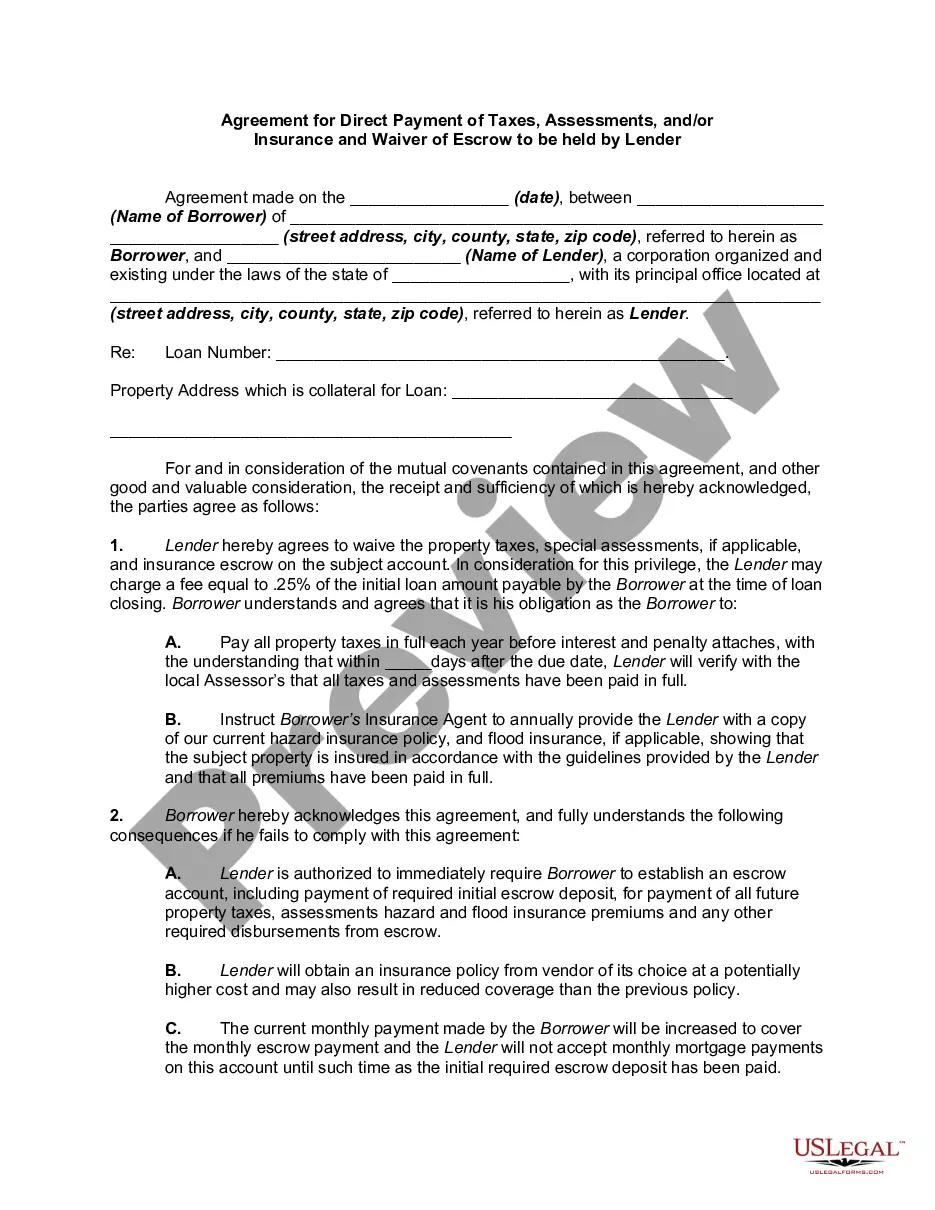

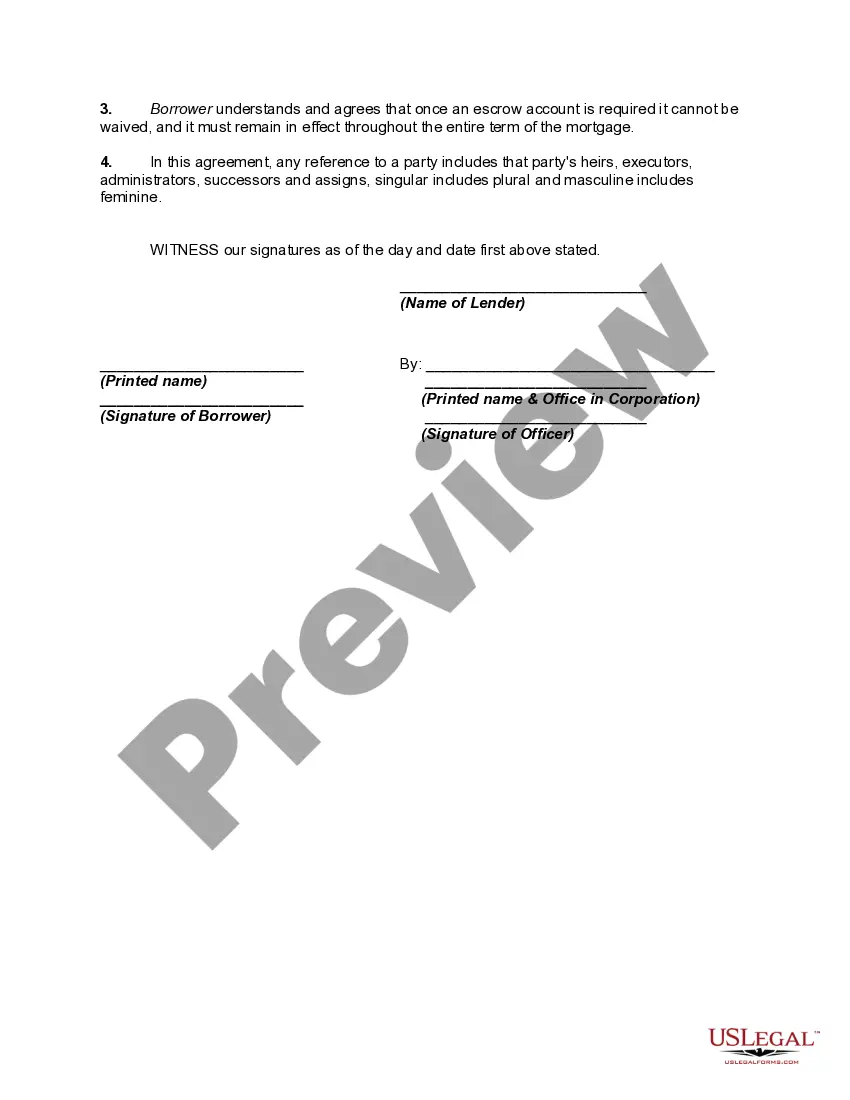

An escrow account refers to an account held in the name of the borrower which is returnable to the borrower on the performance of certain conditions.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Maine Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender is a legal document that outlines the arrangement between a borrower and a lender regarding the payment of property taxes, assessments, and insurance. The agreement allows the borrower to directly pay these expenses instead of setting up an escrow account with the lender. This type of agreement is commonly used in mortgage transactions to give borrowers more control over their finances. By waiving the escrow account requirement, the borrower takes on the responsibility of paying these expenses directly to the appropriate authorities or insurance providers. Maine offers different types of Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender, tailored to specific situations. Some of these agreements may include: 1. Residential Mortgage Agreement: This agreement is designed for borrowers who are purchasing a residential property. It allows the borrower to pay taxes, assessments, and insurance directly, providing flexibility in managing their finances. 2. Commercial Mortgage Agreement: This type of agreement is suitable for borrowers who are financing a commercial property. It enables them to handle tax, assessment, and insurance payments independently, aligning with their business requirements and financial planning. 3. Vacation Property Mortgage Agreement: Borrowers who own vacation properties in Maine can benefit from this agreement. It allows for direct payment of taxes, assessments, and insurance, enabling convenient management of these expenses throughout the year. 4. Condominium Mortgage Agreement: Specifically designed for borrowers purchasing a condominium, this agreement allows individuals to make direct payments for taxes, assessments, and insurance related to their unit. It offers flexibility and control over financial obligations. In all of these agreements, the borrower assumes responsibility for timely payment of property taxes, assessments, and insurance premiums. It is crucial for borrowers to understand the terms and obligations outlined in the Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender to ensure compliance with Maine state laws and regulations. Note that specific agreement names might vary depending on the lender or financial institution. It is essential for borrowers to review and understand the terms tailored to their individual circumstances before entering into any mortgage agreement.The Maine Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender is a legal document that outlines the arrangement between a borrower and a lender regarding the payment of property taxes, assessments, and insurance. The agreement allows the borrower to directly pay these expenses instead of setting up an escrow account with the lender. This type of agreement is commonly used in mortgage transactions to give borrowers more control over their finances. By waiving the escrow account requirement, the borrower takes on the responsibility of paying these expenses directly to the appropriate authorities or insurance providers. Maine offers different types of Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender, tailored to specific situations. Some of these agreements may include: 1. Residential Mortgage Agreement: This agreement is designed for borrowers who are purchasing a residential property. It allows the borrower to pay taxes, assessments, and insurance directly, providing flexibility in managing their finances. 2. Commercial Mortgage Agreement: This type of agreement is suitable for borrowers who are financing a commercial property. It enables them to handle tax, assessment, and insurance payments independently, aligning with their business requirements and financial planning. 3. Vacation Property Mortgage Agreement: Borrowers who own vacation properties in Maine can benefit from this agreement. It allows for direct payment of taxes, assessments, and insurance, enabling convenient management of these expenses throughout the year. 4. Condominium Mortgage Agreement: Specifically designed for borrowers purchasing a condominium, this agreement allows individuals to make direct payments for taxes, assessments, and insurance related to their unit. It offers flexibility and control over financial obligations. In all of these agreements, the borrower assumes responsibility for timely payment of property taxes, assessments, and insurance premiums. It is crucial for borrowers to understand the terms and obligations outlined in the Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender to ensure compliance with Maine state laws and regulations. Note that specific agreement names might vary depending on the lender or financial institution. It is essential for borrowers to review and understand the terms tailored to their individual circumstances before entering into any mortgage agreement.