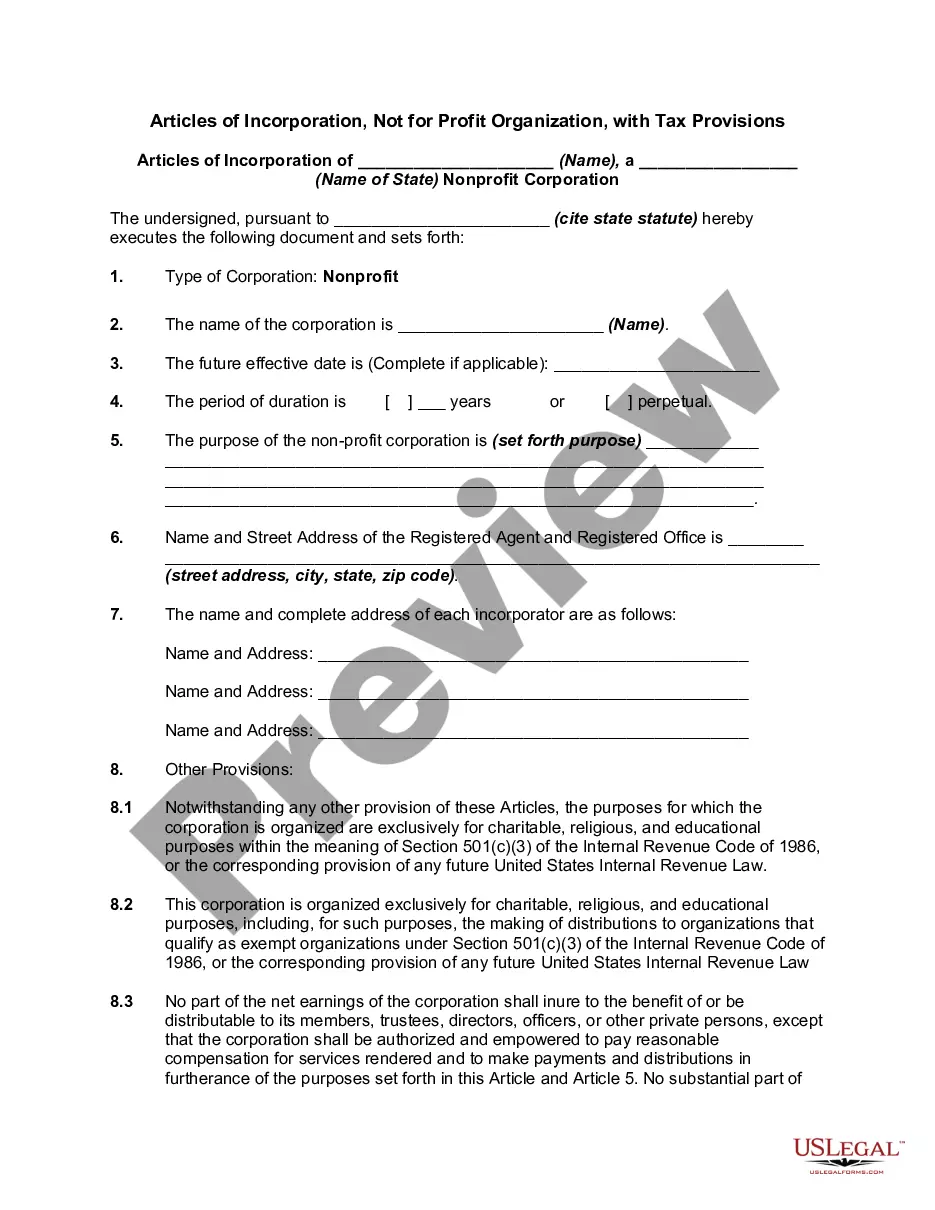

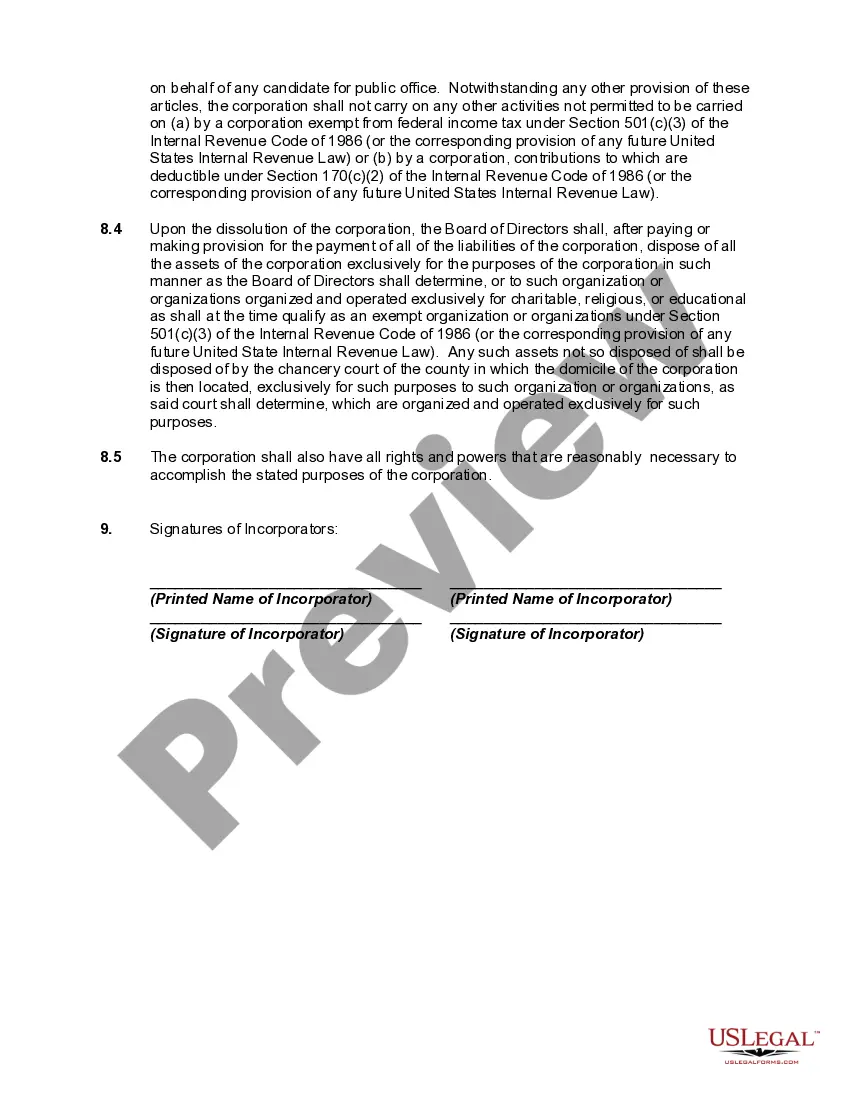

Maine Articles of Incorporation, Not for Profit Organization, with Tax Provisions The Maine Articles of Incorporation for a Not for Profit Organization with Tax Provisions are legal documents that outline the formation and operation of a non-profit organization in the state of Maine. These articles provide a detailed description of the organization's purpose, structure, and tax provisions that apply to its operation. To form a non-profit organization in Maine, the Articles of Incorporation must be filed with the Secretary of State. The document must include certain key information, such as the name of the organization, its principal office address, and the names and addresses of the initial directors or trustees. In addition to the basic information required for any non-profit organization, the Articles of Incorporation for a Not for Profit Organization with Tax Provisions in Maine should contain provisions related to the organization's tax-exempt status. These provisions are crucial to ensure compliance with federal and state tax laws, and they enable the organization to benefit from tax-exempt benefits. Common provisions related to tax-exempt status that may be included in the Maine Articles of Incorporation for a Not for Profit Organization are: 1. Purposes: The articles should clearly state that the organization is organized exclusively for charitable, educational, religious, scientific, or benevolent purposes, as defined by the Internal Revenue Code (IRC) section 501(c)(3). This ensures that the organization qualifies for tax-exempt status. 2. Dissolution: The articles should outline the procedure for the organization's dissolution, including the distribution of assets upon dissolution. This provision is crucial for maintaining tax-exempt status and avoiding any private increment, where individuals benefit from the organization's assets upon dissolution. 3. Prohibition of Private Increment: The articles should explicitly state that no part of the organization's income or assets may benefit any private individual or director, except as allowed by applicable laws. This provision helps prevent the misuse of organizational resources and ensures compliance with tax regulations. 4. Limitations on Activities: The articles should specify that the organization will not engage in activities that jeopardize its tax-exempt status or violate the restrictions set by the IRC. This provision helps prevent any actions that could lead to penalties or loss of tax-exempt status. Maine does not have different types of Articles of Incorporation specifically for non-profit organizations with tax provisions. However, there may be variations in how organizations tailor their articles to meet their specific needs and goals, while ensuring compliance with state and federal tax laws. It's important to consult with an attorney or legal professional familiar with non-profit and tax laws when drafting the Articles of Incorporation for a Not for Profit Organization with Tax Provisions in Maine. They can provide guidance and ensure that the document meets all legal requirements and effectively protects the organization's tax-exempt status.

Maine Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Maine Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

Choosing the right legal record format could be a have a problem. Obviously, there are tons of templates available on the Internet, but how would you obtain the legal kind you will need? Make use of the US Legal Forms web site. The services delivers a large number of templates, for example the Maine Articles of Incorporation, Not for Profit Organization, with Tax Provisions, that can be used for enterprise and personal requirements. All the varieties are examined by specialists and meet up with state and federal demands.

In case you are currently registered, log in to the account and then click the Download switch to get the Maine Articles of Incorporation, Not for Profit Organization, with Tax Provisions. Make use of account to look throughout the legal varieties you might have purchased previously. Check out the My Forms tab of the account and obtain one more backup of the record you will need.

In case you are a brand new user of US Legal Forms, listed below are basic directions that you should comply with:

- Initial, make certain you have chosen the appropriate kind for your personal area/county. It is possible to look through the form using the Preview switch and look at the form description to make sure this is the best for you.

- If the kind does not meet up with your requirements, utilize the Seach industry to obtain the appropriate kind.

- When you are certain the form would work, click on the Buy now switch to get the kind.

- Pick the costs plan you need and enter in the needed details. Build your account and pay for the order utilizing your PayPal account or credit card.

- Pick the submit file format and download the legal record format to the gadget.

- Comprehensive, edit and print and sign the received Maine Articles of Incorporation, Not for Profit Organization, with Tax Provisions.

US Legal Forms is definitely the largest catalogue of legal varieties for which you will find a variety of record templates. Make use of the company to download professionally-produced paperwork that comply with status demands.