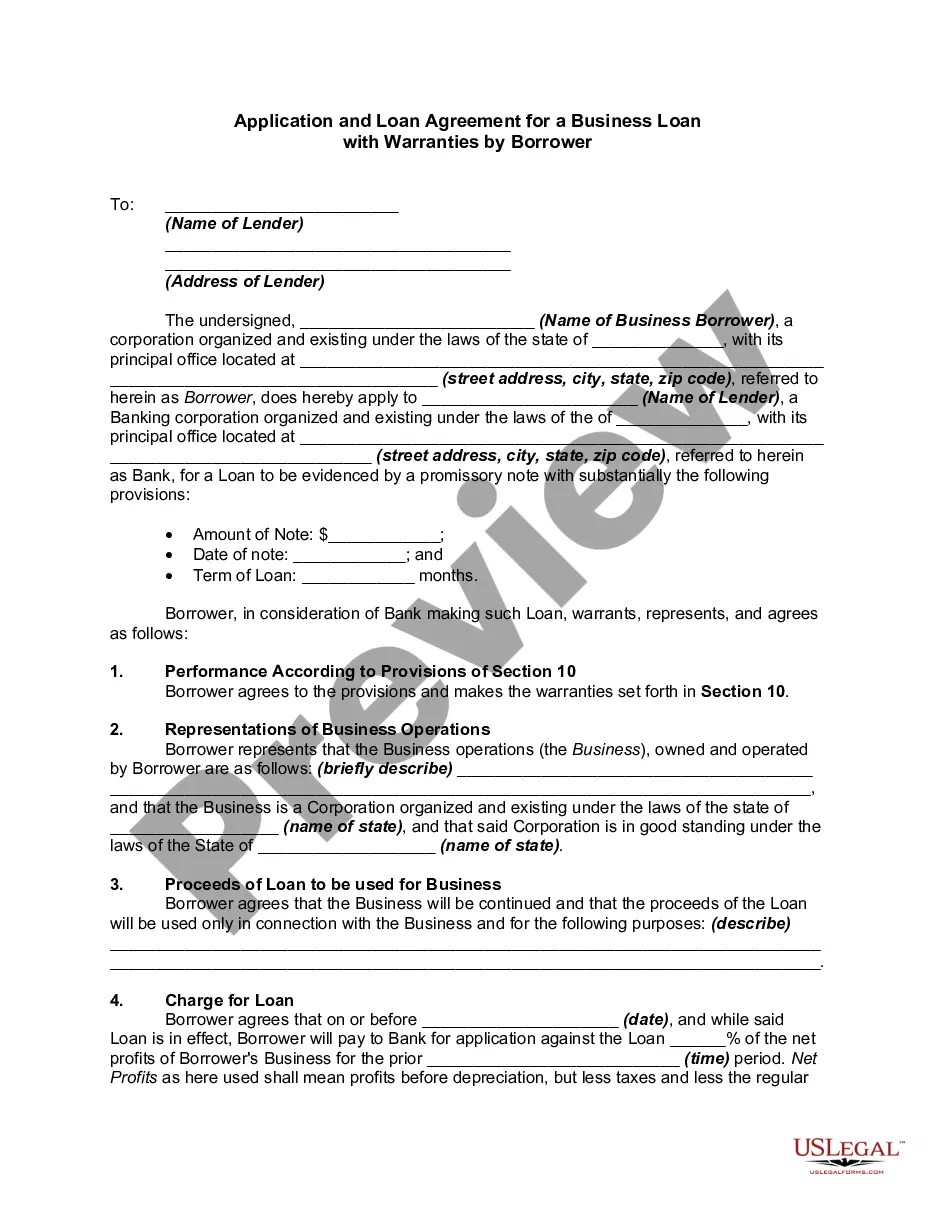

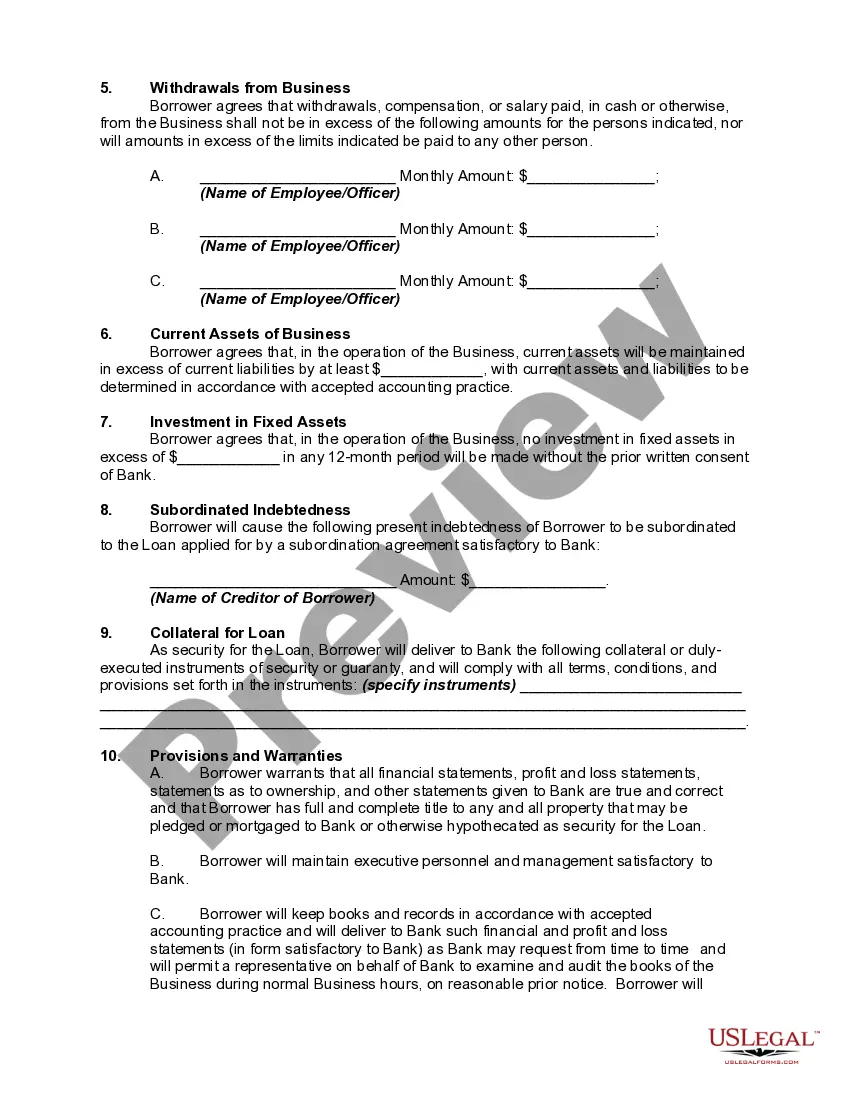

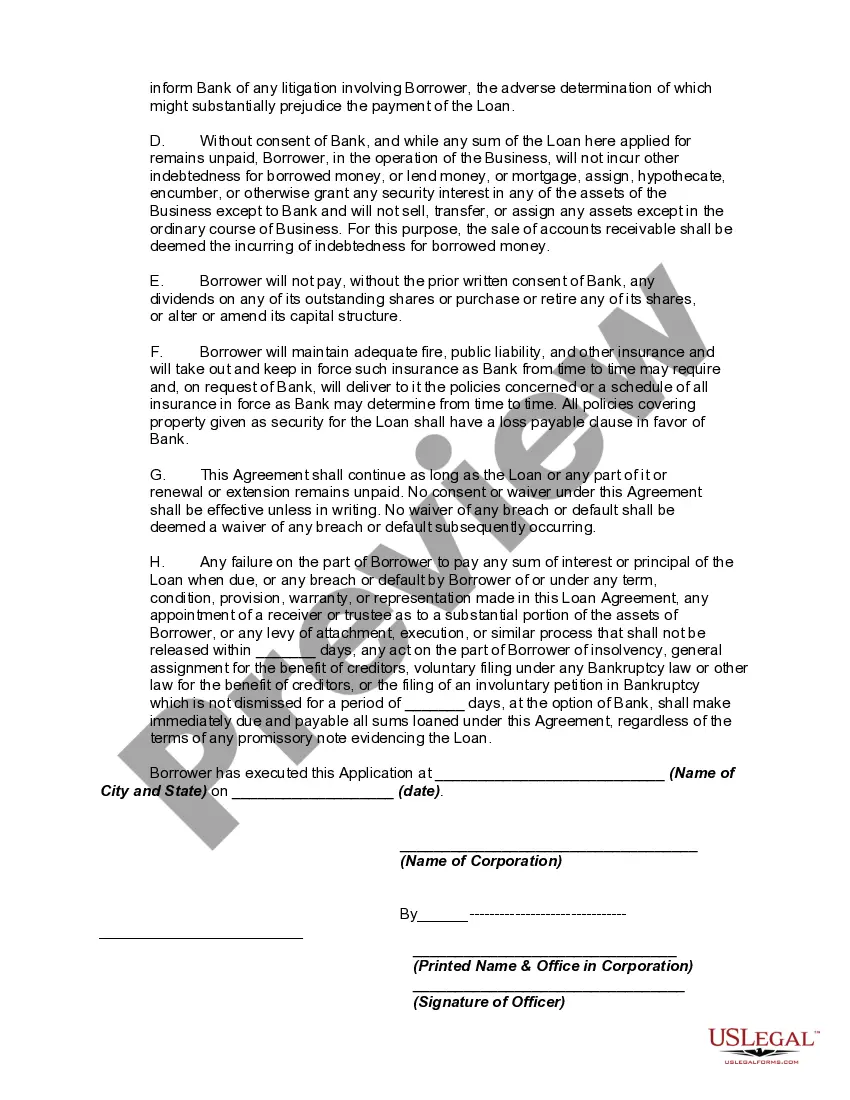

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Maine Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document that outlines the terms and conditions for obtaining a business loan in the state of Maine. This agreement serves as a formal contract between the borrower (the individual or company seeking the loan) and the lender (the financial institution or individual providing the loan). Keywords: Maine, application, loan agreement, business loan, warranties, borrower, terms and conditions, formal contract, financial institution. There are different types of Maine Application and Loan Agreement for a Business Loan with Warranties by Borrower, including: 1. Short-Term Business Loan Agreement: This agreement is designed for borrowers who require a loan with a shorter repayment period, typically ranging from a few months to a year. It specifies the loan amount, interest rate, repayment terms, and warranties provided by the borrower. 2. Long-Term Business Loan Agreement: This type of agreement is suitable for borrowers seeking larger loan amounts with longer repayment periods, typically extending beyond a year. It includes detailed provisions on loan terms, interest rates, installment schedules, and the warranties made by the borrower. 3. Secured Business Loan Agreement: This agreement is specifically crafted for borrowers who are willing to provide collateral as security for their loan. It contains clauses related to the identification, valuation, and maintenance of the pledged assets, in addition to the regular loan terms and warranties. 4. Unsecured Business Loan Agreement: Unlike the secured loan agreement, this type of agreement does not require any collateral from the borrower. However, it may have stricter qualifications and higher interest rates, as it carries a greater risk for the lender. The agreement focuses on the loan terms, interest rates, repayment structure, and warranties made by the borrower. 5. Line of Credit Agreement: This agreement is suitable for borrowers who need flexible access to funds. It establishes a revolving line of credit, allowing the borrower to withdraw funds up to a certain limit and repay it as per agreed terms. The agreement outlines the terms of the line of credit, interest rates, repayment schedules, and borrower warranties. It is important for both borrowers and lenders to fully understand the Maine Application and Loan Agreement for a Business Loan with Warranties. Seeking legal advice before entering into any loan agreement is highly recommended ensuring compliance with state laws and protect the rights and interests of both parties involved.