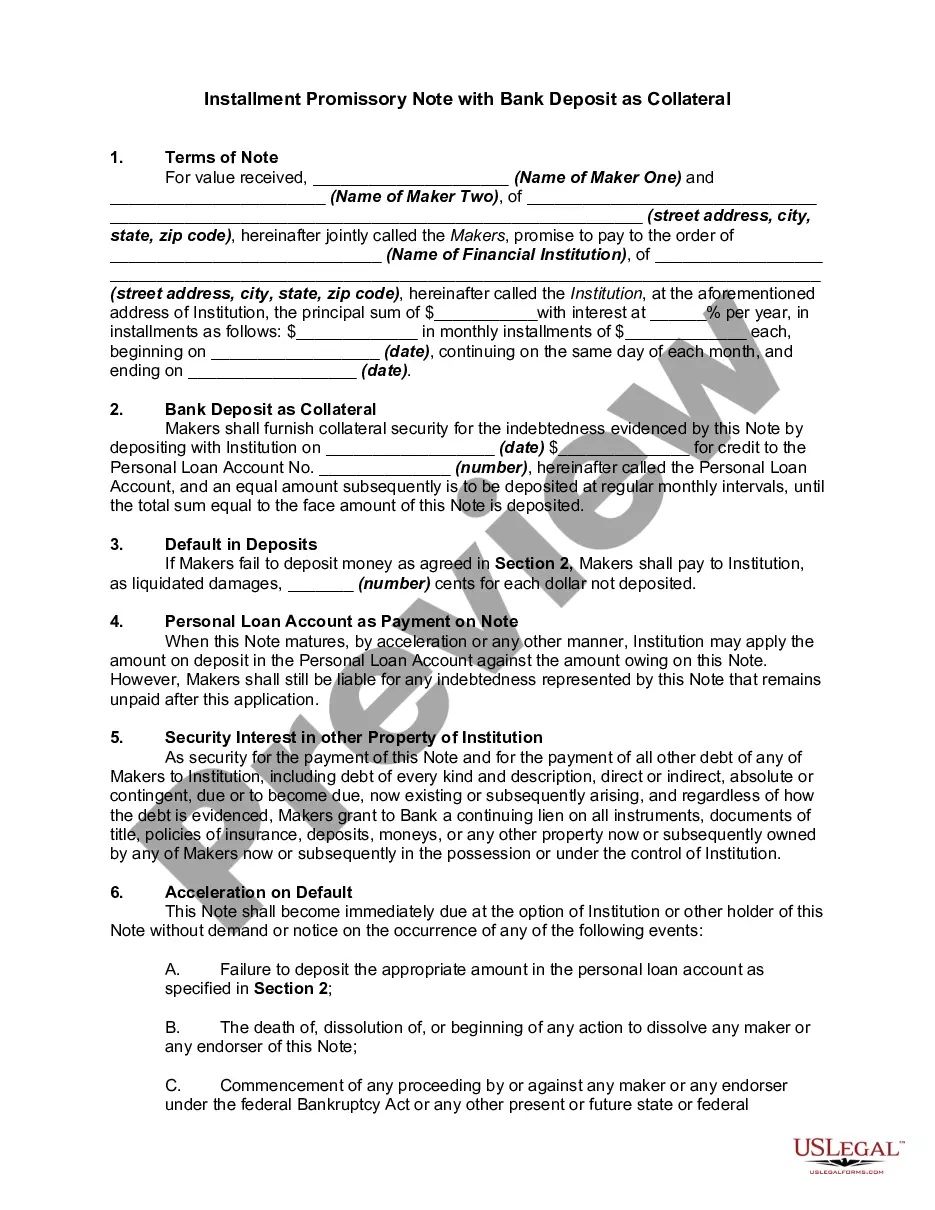

Maine Installment Promissory Note with Bank Deposit as Collateral is a legally binding document used in Maine that outlines the terms and conditions of a loan agreement between a borrower and a lender, with a bank deposit serving as collateral for the loan. This type of promissory note provides security for the lender by allowing them to use the bank deposit as repayment in the event of default by the borrower. The Maine Installment Promissory Note with Bank Deposit as Collateral typically includes important details such as the names and contact information of both parties involved, the loan amount, interest rate, repayment schedule, and any additional charges or fees. It also outlines the consequences of defaulting on the loan, including the rights of the lender to access and utilize the bank deposit as collateral. There are various types of Maine Installment Promissory Note with Bank Deposit as Collateral, depending on the specific terms and conditions agreed upon by the parties involved. Some common variations include: 1. Fixed-Rate Installment Promissory Note: This type of promissory note specifies a predetermined interest rate that remains constant throughout the loan term. The borrower agrees to make regular installment payments over a set period until the loan, along with interest, is fully repaid. 2. Adjustable-Rate Installment Promissory Note: In this variation, the interest rate is subject to change based on specific factors outlined in the note, such as market conditions or an index rate. The borrower's installment payments may fluctuate accordingly. 3. Balloon Payment Installment Promissory Note: This type of promissory note allows the borrower to make small monthly installments over a specified period, with a large "balloon" payment due at the end of the loan term. The bank deposit serves as collateral during the repayment period, and the borrower must either pay the remaining balance or refinance the loan to fulfill the balloon payment. Maine Installment Promissory Note with Bank Deposit as Collateral is essential for protecting the rights and interests of both the borrower and the lender. It provides a legal framework for loan agreements and ensures that all parties involved are aware of their obligations, rights, and potential consequences in the event of default.

Maine Installment Promissory Note with Bank Deposit as Collateral

Description

How to fill out Maine Installment Promissory Note With Bank Deposit As Collateral?

If you wish to total, download, or printing authorized record layouts, use US Legal Forms, the most important selection of authorized types, that can be found on the web. Utilize the site`s simple and handy search to obtain the files you require. Different layouts for organization and specific purposes are sorted by groups and says, or keywords and phrases. Use US Legal Forms to obtain the Maine Installment Promissory Note with Bank Deposit as Collateral with a handful of clicks.

When you are already a US Legal Forms buyer, log in in your accounts and click the Down load button to find the Maine Installment Promissory Note with Bank Deposit as Collateral. You may also gain access to types you previously saved inside the My Forms tab of your own accounts.

If you use US Legal Forms initially, refer to the instructions beneath:

- Step 1. Ensure you have selected the shape to the appropriate city/land.

- Step 2. Take advantage of the Preview method to check out the form`s content material. Don`t neglect to learn the explanation.

- Step 3. When you are not satisfied with the develop, utilize the Lookup industry towards the top of the screen to find other variations in the authorized develop format.

- Step 4. Upon having found the shape you require, select the Acquire now button. Choose the pricing strategy you like and add your credentials to sign up on an accounts.

- Step 5. Approach the financial transaction. You can utilize your charge card or PayPal accounts to perform the financial transaction.

- Step 6. Pick the structure in the authorized develop and download it on your own product.

- Step 7. Complete, edit and printing or sign the Maine Installment Promissory Note with Bank Deposit as Collateral.

Every single authorized record format you buy is yours forever. You may have acces to every single develop you saved with your acccount. Select the My Forms segment and decide on a develop to printing or download again.

Remain competitive and download, and printing the Maine Installment Promissory Note with Bank Deposit as Collateral with US Legal Forms. There are millions of skilled and express-certain types you may use for your organization or specific needs.