Maine Mortgage Note

Description

How to fill out Mortgage Note?

If you have to complete, obtain, or printing lawful document themes, use US Legal Forms, the most important selection of lawful forms, which can be found on-line. Take advantage of the site`s easy and convenient look for to obtain the papers you want. Various themes for business and individual functions are categorized by categories and states, or keywords. Use US Legal Forms to obtain the Maine Mortgage Note with a few clicks.

If you are currently a US Legal Forms buyer, log in for your account and click on the Obtain option to find the Maine Mortgage Note. Also you can gain access to forms you in the past acquired within the My Forms tab of your account.

If you are using US Legal Forms the first time, follow the instructions below:

- Step 1. Make sure you have chosen the shape to the appropriate city/land.

- Step 2. Utilize the Review choice to look over the form`s content material. Do not neglect to read through the information.

- Step 3. If you are unsatisfied together with the develop, take advantage of the Look for field near the top of the display to get other models in the lawful develop web template.

- Step 4. When you have found the shape you want, go through the Purchase now option. Choose the prices strategy you choose and add your accreditations to sign up for an account.

- Step 5. Procedure the financial transaction. You may use your charge card or PayPal account to finish the financial transaction.

- Step 6. Choose the format in the lawful develop and obtain it in your gadget.

- Step 7. Complete, revise and printing or indication the Maine Mortgage Note.

Every single lawful document web template you buy is yours forever. You might have acces to each develop you acquired in your acccount. Select the My Forms section and select a develop to printing or obtain yet again.

Contend and obtain, and printing the Maine Mortgage Note with US Legal Forms. There are millions of professional and state-distinct forms you may use for your personal business or individual requirements.

Form popularity

FAQ

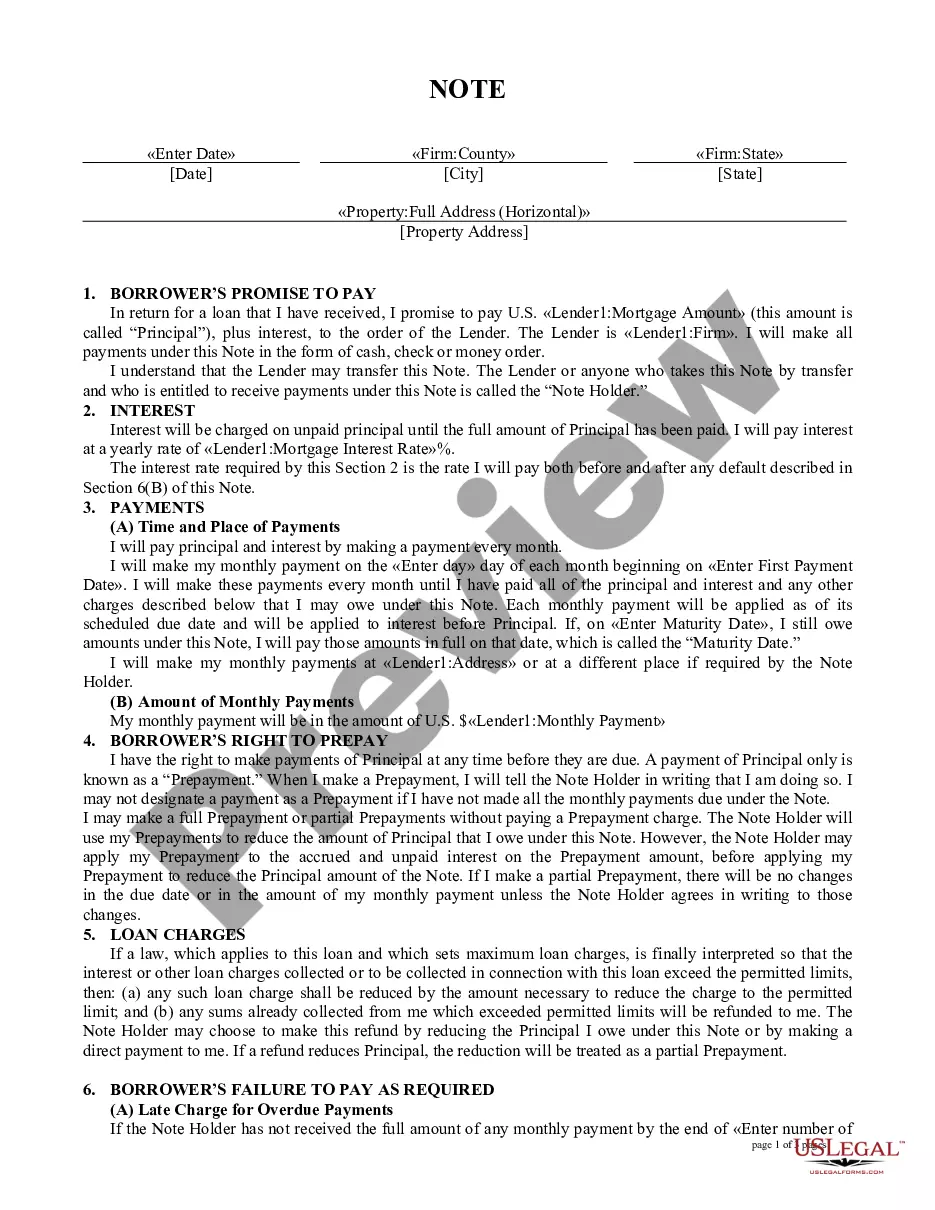

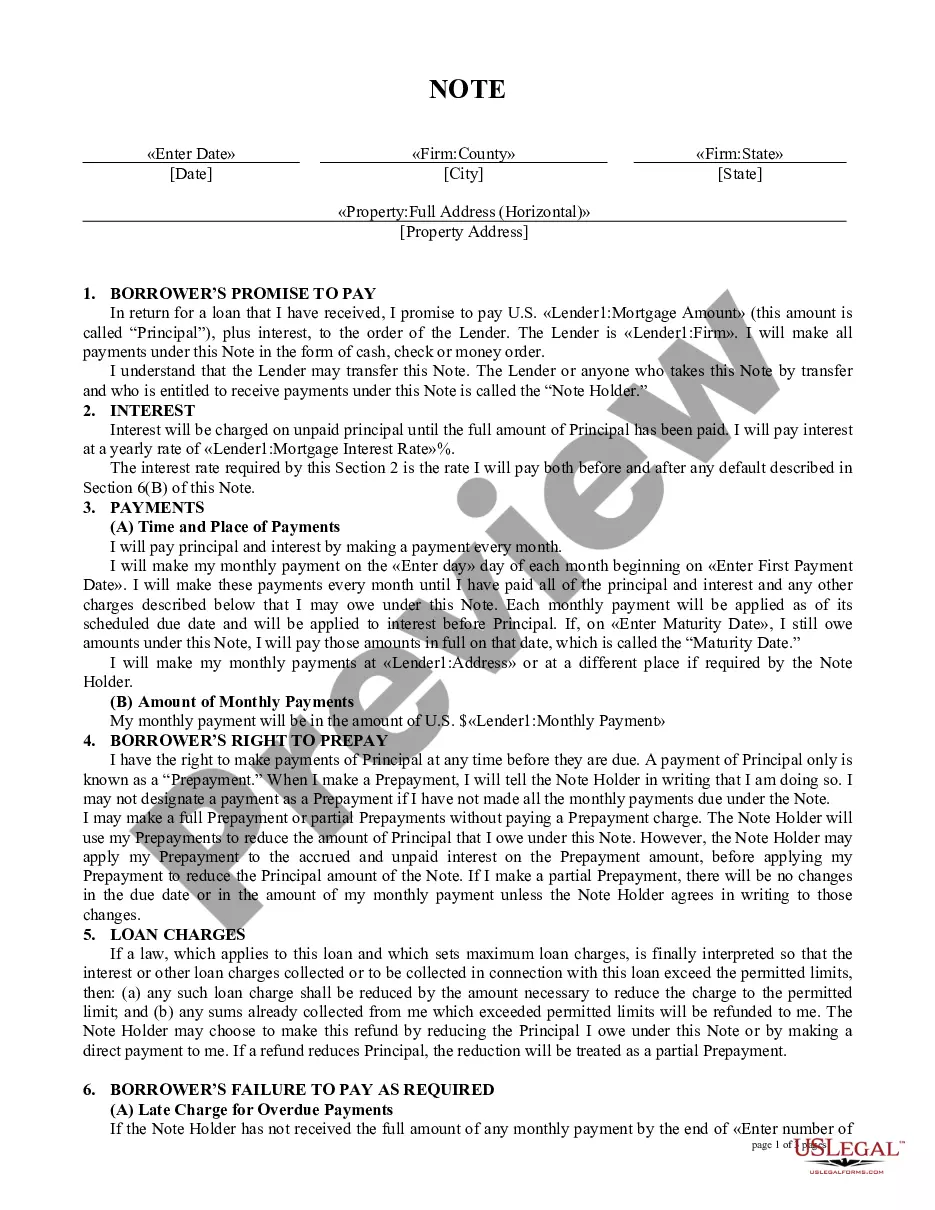

A mortgage note is a legal document in which borrowers agree to terms with the lender, or mortgagee. It is legally binding. Borrowers receive a mortgage note from a lender when taking out a loan for a new purchase or refinance. In some states, borrowers and lenders will use a deed of trust instead of a mortgage.

A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.

In the United States, a mortgage note (also known as a real estate lien note, borrower's note) is a promissory note secured by a specified mortgage loan. Mortgage notes are a written promise to repay a specified sum of money plus interest at a specified rate and length of time to fulfill the promise.

The Deed is a recorded document memorializing the transfer of property from the Grantor to the Grantee. The Note is an unrecorded paper that binds an individual who has assumed debt through a promise-to-pay instrument.

A "mortgage" is a contract between you and the lender that creates a lien on the property. Some states use mortgages to create the lien, while others typically use deeds of trust or another similar-sounding instrument.