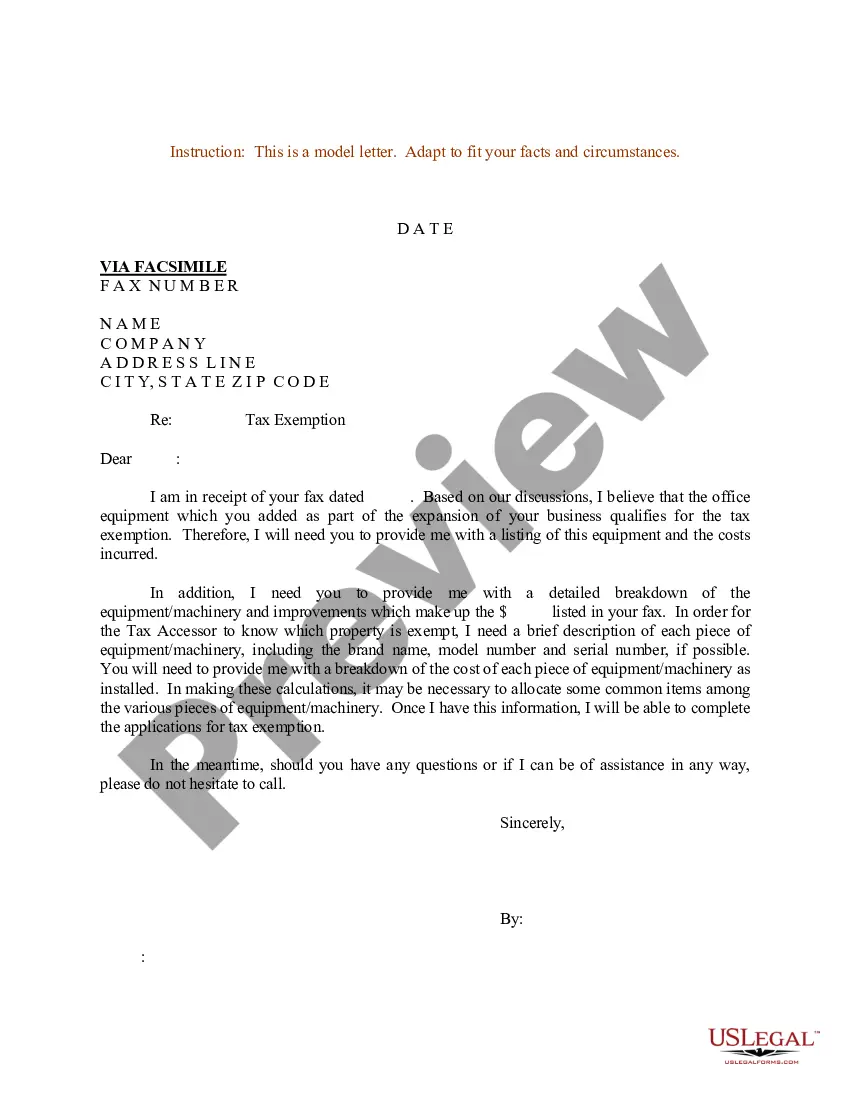

Title: Maine Sample Letter for Tax Exemption — Discussion of Office Equipment Qualifying for Tax Exemption Introduction: In the state of Maine, businesses and organizations may utilize tax exemptions for certain office equipment. This article presents a comprehensive overview of Maine's tax exemption process and provides a sample letter to request tax exemption for office equipment. It addresses the forms, requirements, and guidelines for this exemption. Maine Tax Exemption for Office Equipment: Maine provides a tax exemption for office equipment that meets specific criteria. The state aims to support businesses and organizations by relieving them of tax burdens associated with certain assets. Here, we discuss the qualification requirements and types of office equipment eligible for tax exemption. Types of Office Equipment Qualifying for Tax Exemption: 1. Computers and Laptops: Desktop computers, laptops, servers, computer peripherals such as monitors, keyboards, and mice, as well as related software, may be eligible for tax exemption. 2. Office Furniture: Desks, chairs, cabinets, tables, and other furniture items used exclusively for office purposes might qualify for tax exemption. 3. Communication Equipment: Telephone systems, fax machines, printers, copiers, answering machines, and other communication devices may be eligible for tax exemption if used solely for business purposes. 4. Security Systems: Surveillance cameras, alarm systems, access control devices, and other security-related equipment used exclusively for office security might qualify for tax exemption. 5. Office Machinery: This category may include printers, scanners, shredders, binding machines, laminators, and other machinery used strictly for office-related tasks. Requirements for Tax Exemption: To qualify for tax exemption on office equipment in Maine, several requirements must be met: a. Exclusive Business Use: The office equipment should be used solely for business or organization-related purposes. b. Non-Resale: The equipment must not be acquired for resale. It should be used to conduct day-to-day operations. c. Registration and Pre-Approval: Appropriate registration with the relevant tax authority or department is necessary. In some cases, obtaining pre-approval or an exemption certificate might be required. Sample Letter for Tax Exemption: The provided sample letter serves as a template to request tax exemption for office equipment in Maine. Use it as a reference to draft a customized letter, ensuring you include specific details about the office equipment and clearly state your eligibility for tax exemption. Conclusion: Maine's tax exemption for office equipment aims to promote business growth and reduce financial burdens on organizations. Understanding the qualifying criteria, including eligible equipment types, requirements, and utilizing a sample letter for tax exemption can streamline the process. Ensure compliance with all regulations while seeking tax exemption on office equipment in Maine.

Maine Sample Letter for Tax Exemption - Discussion of Office Equipment Qualifying for Tax Exemption

Description

How to fill out Maine Sample Letter For Tax Exemption - Discussion Of Office Equipment Qualifying For Tax Exemption?

Have you been in a situation that you require files for both company or person functions nearly every day? There are plenty of legitimate file themes accessible on the Internet, but locating types you can depend on isn`t effortless. US Legal Forms gives 1000s of kind themes, such as the Maine Sample Letter for Tax Exemption - Discussion of Office Equipment Qualifying for Tax Exemption, that are composed to meet state and federal requirements.

When you are already knowledgeable about US Legal Forms website and have an account, basically log in. After that, you are able to acquire the Maine Sample Letter for Tax Exemption - Discussion of Office Equipment Qualifying for Tax Exemption web template.

If you do not provide an bank account and would like to begin using US Legal Forms, follow these steps:

- Obtain the kind you require and ensure it is for the proper city/state.

- Use the Preview button to check the form.

- Browse the description to actually have chosen the correct kind.

- In case the kind isn`t what you are searching for, utilize the Look for area to obtain the kind that meets your needs and requirements.

- Whenever you find the proper kind, click on Acquire now.

- Select the costs prepare you need, complete the necessary details to generate your account, and purchase an order utilizing your PayPal or charge card.

- Decide on a hassle-free file file format and acquire your version.

Find each of the file themes you may have purchased in the My Forms menus. You can get a extra version of Maine Sample Letter for Tax Exemption - Discussion of Office Equipment Qualifying for Tax Exemption at any time, if required. Just click the needed kind to acquire or print the file web template.

Use US Legal Forms, by far the most comprehensive collection of legitimate kinds, to conserve efforts and avoid errors. The assistance gives appropriately created legitimate file themes that can be used for an array of functions. Produce an account on US Legal Forms and commence generating your life easier.