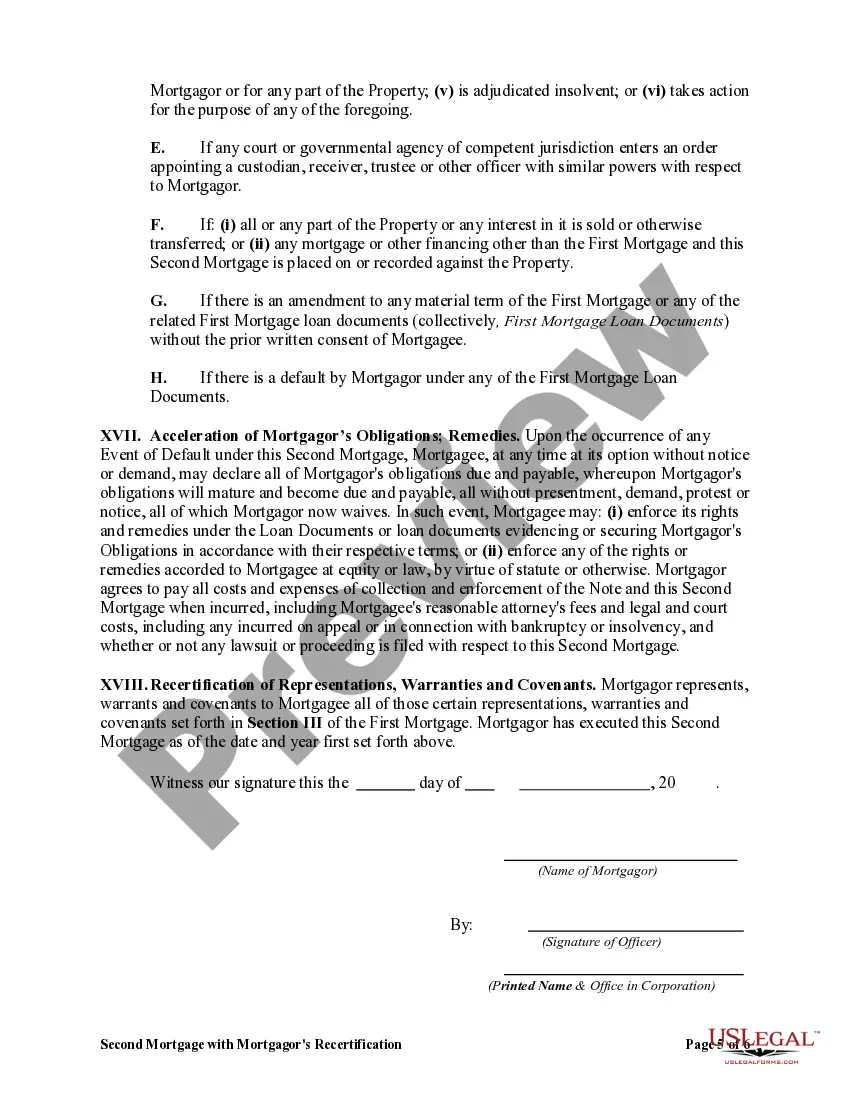

Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a specific type of mortgage agreement prevalent in the state of Maine. It is crucial to understand the key details and accompanying terms associated with this mortgage to make informed decisions. This content will explain the purpose of the mortgage, provide information about the recertification process, and highlight any variations or additional types of Maine Second Mortgages with similar characteristics. A Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a legal agreement between a lender (mortgagee) and a borrower (mortgagor) that enables the borrower to secure additional financing while using their property as collateral. This secondary mortgage is established after an initial primary mortgage has already been secured on the property. The purpose of a Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is to provide borrowers with a means to access additional funds without refinancing or jeopardizing their existing primary mortgage. It allows homeowners to tap into their home equity for various purposes, such as home improvements, debt consolidation, or covering unexpected expenses. In this specific mortgage agreement, a noteworthy aspect is the requirement for the mortgagor to recertify the representations, warranties, and covenants made in the first mortgage. This recertification process ensures that the borrower reaffirms the truthfulness and accuracy of the information provided during the initial mortgage application. By doing so, the mortgagor confirms that there have been no material changes or misrepresentations in their financial standing, property condition, or other relevant factors since the first mortgage was obtained. The specific language and content of the recertification clause may vary depending on the lender and the terms negotiated between the parties involved. However, typically, the recertification process involves the borrower signing a document stating the continued validity of the original representations, warranties, and covenants. This recertification reinforces the integrity of the mortgage agreement and protects the lender's interests. While the Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is the primary form of this mortgage in the state, there can be some variations or other related types. These may include: 1. Maine Second Mortgage with Modified Recertification: This variant of the second mortgage may have minor modifications to the recertification process to suit specific borrower or lender requirements. The modified recertification may involve additional clauses or alterations to the recertification language. 2. Maine Second Mortgage with Amended Representations and Warranties: In this type of second mortgage, rather than solely recertifying the original representations and warranties, the borrower may be required to amend or update certain aspects based on new circumstances or changes in the property or financial condition. 3. Maine Second Mortgage with Limited Recertification: Some second mortgages may feature a limited recertification requirement, whereby the borrower is only required to provide updated information related to specific aspects, such as income or employment, without revisiting the entire set of representations and warranties. It is essential for borrowers considering a Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage to carefully review the specific terms and conditions provided by the lender. Obtaining professional advice from mortgage specialists, attorneys, or financial advisors can help ensure a thorough understanding of the mortgage agreement and assist in making an informed decision.

Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Maine Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

Have you been within a placement that you require documents for sometimes enterprise or personal purposes nearly every day? There are a variety of authorized papers templates available on the net, but getting types you can rely on isn`t easy. US Legal Forms delivers thousands of develop templates, much like the Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, which can be written to meet federal and state demands.

When you are presently familiar with US Legal Forms site and also have a merchant account, just log in. Following that, you may download the Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage web template.

If you do not provide an profile and would like to start using US Legal Forms, adopt these measures:

- Obtain the develop you want and make sure it is for that correct city/county.

- Use the Preview option to examine the shape.

- Look at the explanation to actually have chosen the right develop.

- In case the develop isn`t what you are seeking, use the Research industry to get the develop that meets your needs and demands.

- Once you get the correct develop, simply click Acquire now.

- Pick the pricing prepare you need, fill in the required information and facts to make your account, and buy your order utilizing your PayPal or bank card.

- Decide on a practical file formatting and download your copy.

Find all of the papers templates you may have purchased in the My Forms menus. You can get a additional copy of Maine Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage whenever, if possible. Just click on the necessary develop to download or print the papers web template.

Use US Legal Forms, the most extensive collection of authorized varieties, in order to save some time and steer clear of mistakes. The support delivers expertly made authorized papers templates that can be used for a range of purposes. Produce a merchant account on US Legal Forms and initiate generating your life easier.

Form popularity

FAQ

TL;DR: The primary mortgage market is used for homebuyers and lenders. Lenders finance a borrower's purchase of a home. The secondary mortgage market is between lenders and mortgage investors. Lenders will sell the debt to the investor who will buy it to make a profit.

First Mortgagee means any person named as a mortgagee or beneficiary in any First Mortgage, or any successor to the interest of any such person under such First Mortgage.

How to Combine Two Mortgages Review Your Refinance Options. Before you start the consolidation process, read up on the different refinancing options available. ... Apply for the Refinance Loan. ... Get an Appraisal. ... Close on the New Loan. ... Lower Interest Rate. ... Switch From ARM to Fixed-Rate. ... Shorter Loan Term. ... Lower Monthly Payments.

A second mortgage is a loan made in addition to the homeowner's primary mortgage. Home equity lines of credit (HELOCs) are often used as second mortgages. Homeowners might use a second mortgage to finance large purchases like college, a new vehicle, or even a down payment on a second home.

Key Takeaways. A first mortgage is a primary lien on the property that secures the mortgage. The second mortgage is money borrowed against home equity to fund other projects and expenditures.