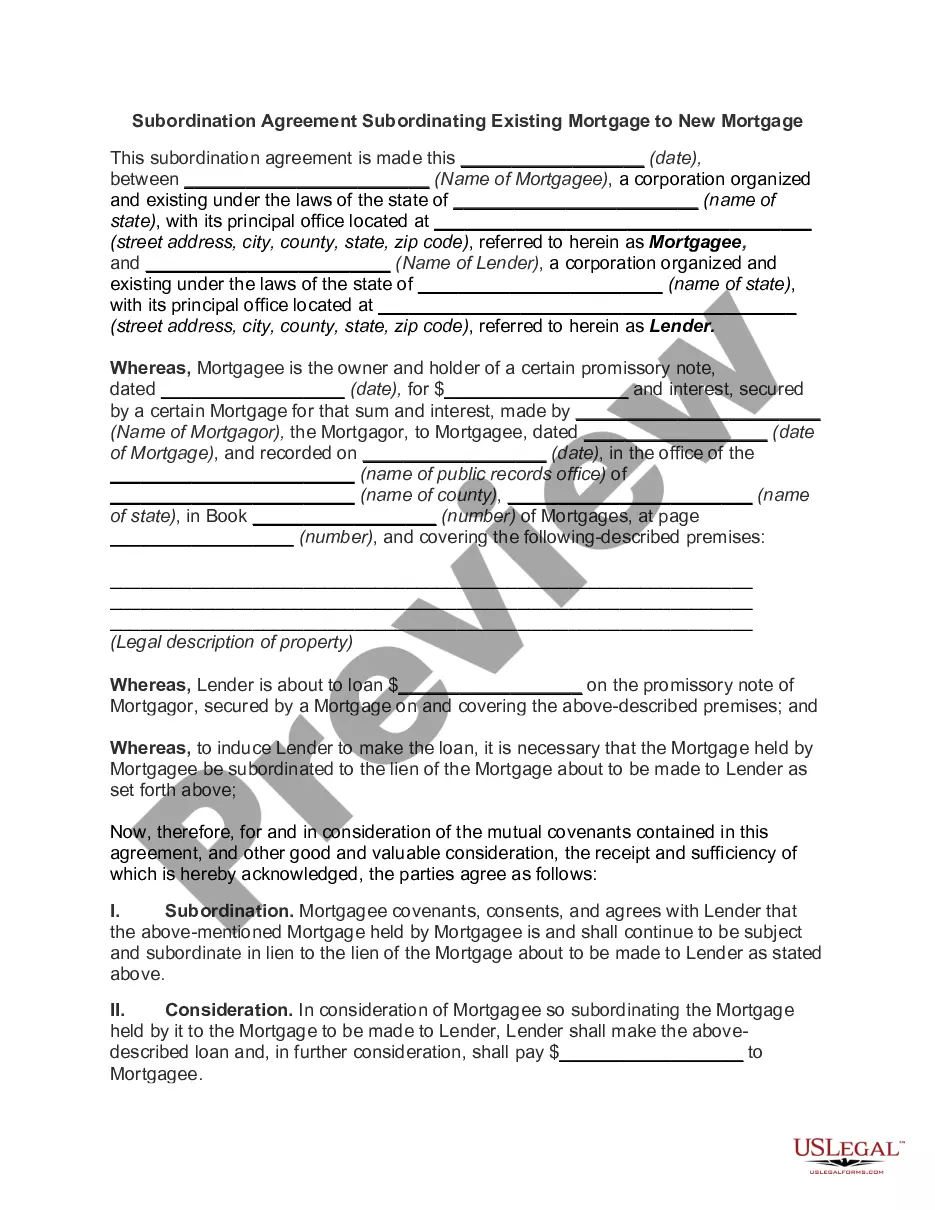

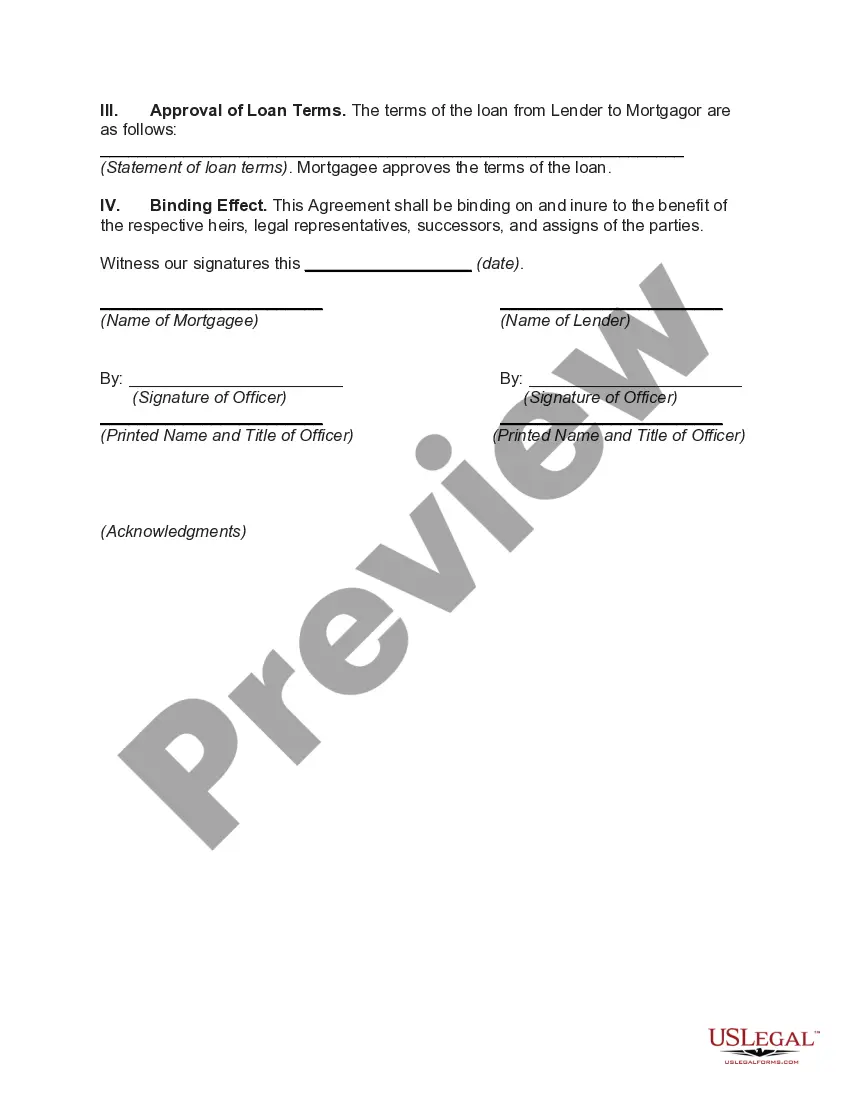

Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage: A Comprehensive Guide Introduction: A Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document that outlines the terms and conditions of subordination between two mortgages. This agreement is necessary when a borrower wants to secure a new mortgage while keeping the existing mortgage intact but subordinate to the new one. It ensures that the new mortgage takes priority in case of default or foreclosure. In Maine, specific types of subordination agreements may be used based on the specific circumstances. Let's explore the different types of Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage: 1. Maine Subordination Agreement for Refinancing: This type of subordination agreement is used when a homeowner wants to secure a refinancing loan to replace their existing mortgage. By signing this agreement, the homeowner acknowledges that the new mortgage will have priority over the existing mortgage. This agreement is crucial for lenders providing refinancing options as it protects their investment by ensuring that any subsequent mortgage takes precedence in case of default. 2. Maine Subordination Agreement for Home Equity Loan or Line of Credit: When borrowers seek additional funds using their home equity through a loan or line of credit, they may need a subordination agreement to establish the order of priority between the existing mortgage and the new loan. This subordination agreement protects the lending institution's interests, primarily if the borrower defaults on their mortgage and the property goes into foreclosure. 3. Maine Subordination Agreement for Second Mortgage: In certain situations, borrowers who need additional financing may choose to take out a second mortgage instead of refinancing or obtaining a home equity loan. In this case, a subordination agreement is necessary to define the relationship between the first mortgage (existing mortgage) and the second mortgage (new mortgage). This agreement clarifies that the second mortgage holder accepts a subordinate position and their lien is secondary to the first mortgage. Key Features of a Maine Subordination Agreement: 1. Lien Priority: The agreement specifies that the new mortgage will take priority over the existing mortgage. This detail ensures that the lender providing the new mortgage will be the first to be repaid in case of foreclosure or default. 2. Consent from Existing Mortgage Holder: The agreement requires the consent and acknowledgment of the existing mortgage holder, indicating their willingness to subordinate their lien to the new mortgage. This consent ensures that all parties involved are aware of and agree to the modified order of lien priority. 3. Decoration: To make the subordination agreement legally binding and enforceable, it must be recorded in the appropriate county records office. This step ensures public notice and creates an official record that can be referenced in the future. Conclusion: Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a crucial legal document used in various situations such as refinancing, obtaining home equity loans or lines of credit, or taking out a second mortgage. It establishes the priority of liens, protecting the interests of lenders and ensuring a clear order of lien priority. By understanding the different types of subordination agreements available in Maine, borrowers and lenders can navigate the mortgage process with confidence.

Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Maine Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Choosing the right authorized record web template could be a have difficulties. Of course, there are tons of web templates accessible on the Internet, but how will you discover the authorized develop you need? Make use of the US Legal Forms website. The services delivers a large number of web templates, for example the Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage, that you can use for business and private needs. Each of the types are inspected by specialists and meet federal and state demands.

If you are presently listed, log in for your accounts and click the Download option to obtain the Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Make use of accounts to check through the authorized types you might have ordered formerly. Visit the My Forms tab of your respective accounts and have yet another copy of your record you need.

If you are a new user of US Legal Forms, listed below are straightforward recommendations that you should comply with:

- Very first, make sure you have chosen the correct develop to your metropolis/area. It is possible to examine the form using the Review option and browse the form information to guarantee it will be the right one for you.

- If the develop does not meet your requirements, use the Seach field to discover the proper develop.

- Once you are certain that the form is proper, go through the Buy now option to obtain the develop.

- Pick the prices program you would like and type in the necessary info. Build your accounts and pay for the order using your PayPal accounts or Visa or Mastercard.

- Opt for the document format and acquire the authorized record web template for your system.

- Total, edit and print and indicator the acquired Maine Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms will be the greatest collection of authorized types for which you can find a variety of record web templates. Make use of the company to acquire expertly-created papers that comply with state demands.