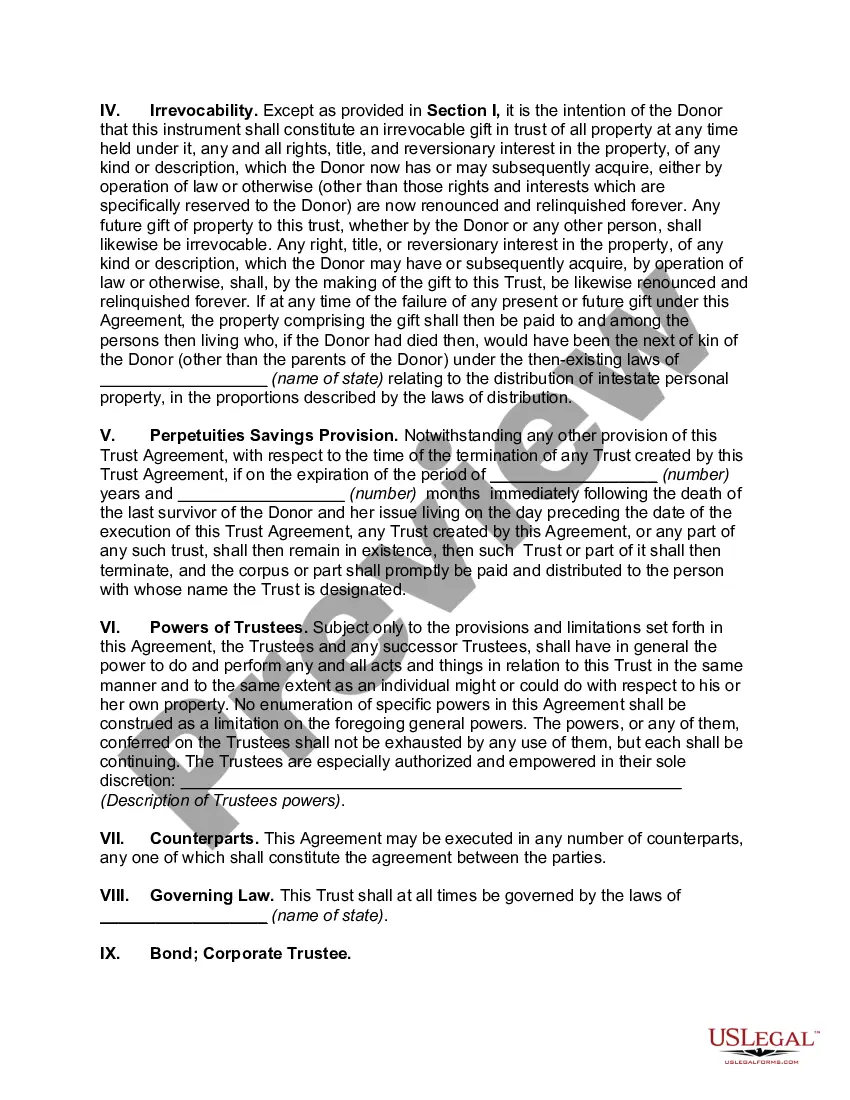

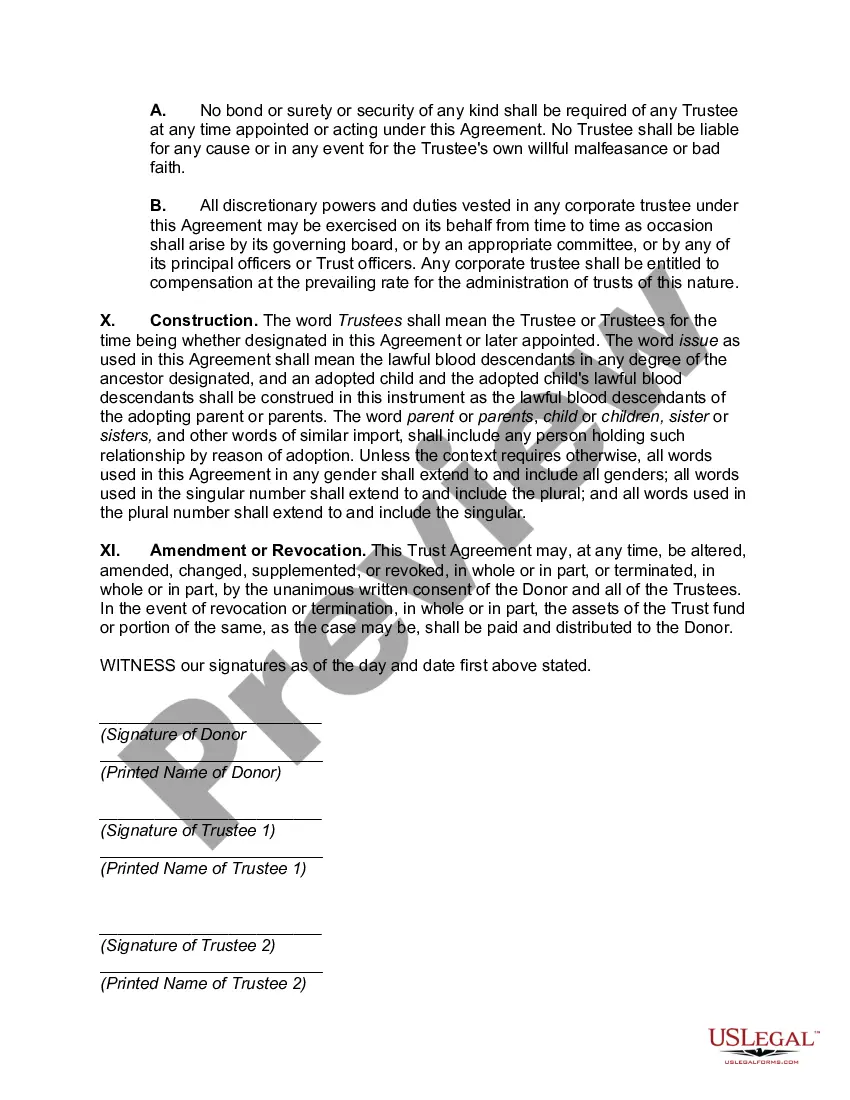

Maine Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is an important estate planning tool that allows individuals to transfer assets to their beneficiaries while retaining some level of income for a specified period. This type of trust is commonly used in Maine and offers several benefits for granters. The primary objective of a Maine Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is to reduce the granter's estate tax liability. By transferring assets into the trust, the granter removes them from their taxable estate, ultimately minimizing the potential tax burden on their beneficiaries. This can be particularly advantageous for individuals with substantial assets or those concerned about estate taxes. One significant feature of this type of trust is that the granter retains the right to receive income generated by the trust during the specified term. This ensures a steady stream of income for the granter, allowing them to maintain their financial security throughout the designated period. Once the specified term expires, the trust is divided into individual trusts for each named beneficiary or issue. These separate trusts are then distributed to the beneficiaries in accordance with the granter's wishes. This division allows for flexibility in distributing assets and can consider the specific needs and circumstances of each beneficiary. There may be variations of the Maine Granter Retained Income Trust with Division into Trusts for Issue after Term of Years, such as: 1. Fixed-Term Granter Retained Income Trust: This type of trust has a predetermined term, usually a specific number of years. Upon the trust's termination, the assets are divided into separate trusts for the beneficiaries. 2. Flexible-Term Granter Retained Income Trust: Unlike fixed-term trusts, flexible-term trusts allow the granter to determine the duration of the trust within certain defined limits. This enables greater flexibility and adaptability to changing circumstances or personal preferences. 3. Charitable Granter Retained Income Trust: This particular trust includes provisions to donate a portion of the trust's assets to qualified charitable organizations at the end of the term. This not only provides income to the granter but also offers potential estate tax benefits while supporting charitable causes. In conclusion, a Maine Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is an estate planning tool that allows individuals to transfer assets to their beneficiaries while retaining income for a specific period. Its main advantages are reducing estate tax liability and providing income for the granter during the term. Different variations of this trust include fixed-term, flexible-term, and charitable grantor-retained income trusts.

Maine Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years

Description

How to fill out Maine Grantor Retained Income Trust With Division Into Trusts For Issue After Term Of Years?

If you wish to comprehensive, obtain, or print out lawful record themes, use US Legal Forms, the largest variety of lawful types, that can be found on the web. Make use of the site`s simple and convenient search to find the paperwork you want. Numerous themes for business and personal functions are categorized by types and states, or keywords. Use US Legal Forms to find the Maine Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years in a few clicks.

In case you are previously a US Legal Forms client, log in to the bank account and click the Obtain key to obtain the Maine Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years. Also you can gain access to types you in the past saved inside the My Forms tab of the bank account.

If you work with US Legal Forms the very first time, follow the instructions below:

- Step 1. Be sure you have chosen the form for your right town/nation.

- Step 2. Utilize the Review method to look over the form`s information. Never forget about to learn the explanation.

- Step 3. In case you are not satisfied with all the kind, make use of the Look for industry at the top of the monitor to get other models of your lawful kind web template.

- Step 4. Upon having discovered the form you want, click on the Get now key. Select the costs program you prefer and add your references to register for the bank account.

- Step 5. Approach the financial transaction. You may use your Мisa or Ьastercard or PayPal bank account to perform the financial transaction.

- Step 6. Find the formatting of your lawful kind and obtain it on your own device.

- Step 7. Total, change and print out or indication the Maine Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years.

Each lawful record web template you acquire is yours for a long time. You may have acces to each kind you saved with your acccount. Click the My Forms segment and decide on a kind to print out or obtain once more.

Be competitive and obtain, and print out the Maine Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years with US Legal Forms. There are thousands of specialist and condition-certain types you may use for your business or personal needs.