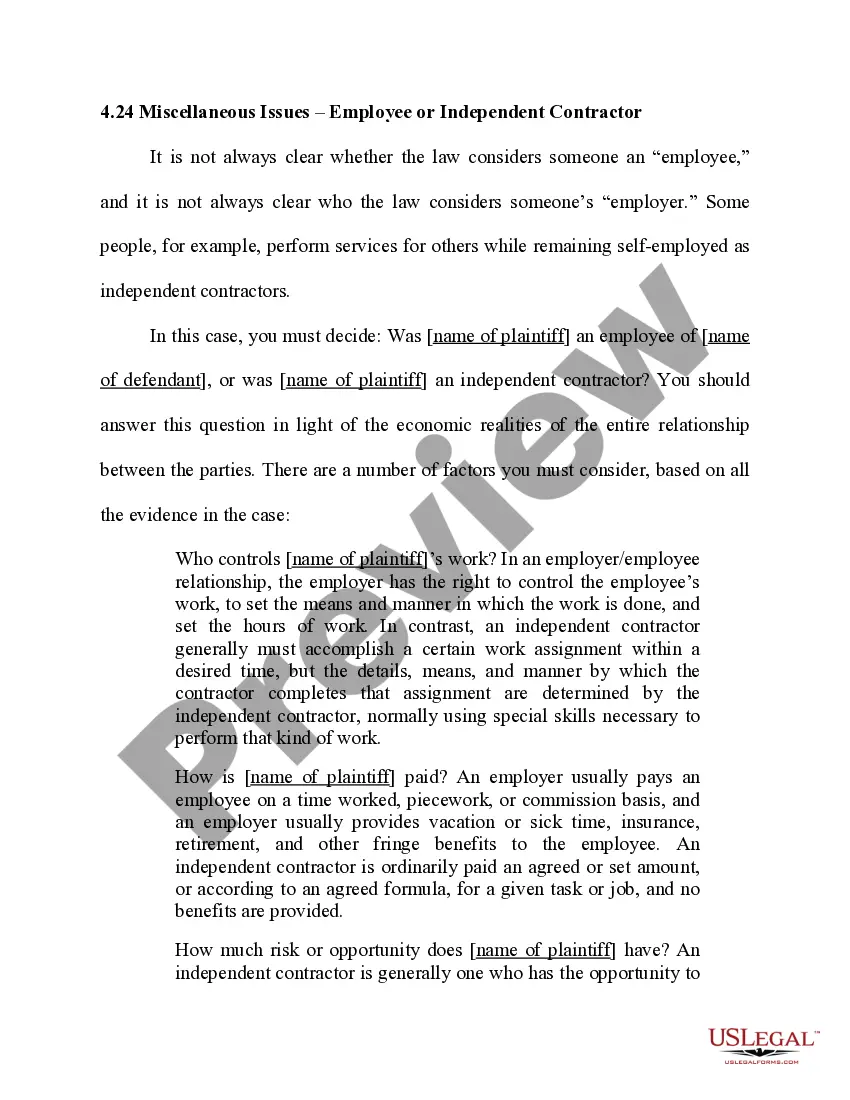

Maine Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor

Description

How to fill out Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor?

If you need to comprehensive, obtain, or print out legal file templates, use US Legal Forms, the greatest collection of legal types, that can be found on the web. Take advantage of the site`s simple and easy handy research to get the papers you need. A variety of templates for enterprise and person reasons are categorized by classes and claims, or search phrases. Use US Legal Forms to get the Maine Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor in just a couple of clicks.

If you are already a US Legal Forms buyer, log in to your account and click on the Acquire button to find the Maine Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor. Also you can gain access to types you in the past saved inside the My Forms tab of your respective account.

If you work with US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have chosen the shape for your appropriate city/region.

- Step 2. Use the Review solution to examine the form`s content material. Never neglect to learn the information.

- Step 3. If you are not happy together with the kind, utilize the Lookup field at the top of the display to get other types in the legal kind format.

- Step 4. After you have identified the shape you need, click on the Acquire now button. Pick the rates prepare you like and add your qualifications to register on an account.

- Step 5. Method the transaction. You can use your Мisa or Ьastercard or PayPal account to accomplish the transaction.

- Step 6. Choose the format in the legal kind and obtain it in your product.

- Step 7. Complete, change and print out or sign the Maine Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor.

Every single legal file format you acquire is your own permanently. You might have acces to every single kind you saved within your acccount. Go through the My Forms portion and choose a kind to print out or obtain again.

Remain competitive and obtain, and print out the Maine Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor with US Legal Forms. There are millions of skilled and status-distinct types you may use to your enterprise or person needs.

Form popularity

FAQ

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

Pursuant to state law, the Maine Department of Labor and Maine Workers' Compensation Board presume a worker you hire is an employee unless you can demonstrate the worker meets the legal standard for being an independent contractor.

The law further states that independent contractor status is evidenced if the worker: (1) has a substantial investment in the business other than personal services, (2) purports to be in business for himself or herself, (3) receives compensation by project rather than by time, (4) has control over the time and place ...

The basic test for determining whether a worker is an independent contractor or an employee is whether the principal has the right to control the manner and means by which the work is performed.

For the employee, the company withholds income tax, Social Security, and Medicare from wages paid. For the independent contractor, the company does not withhold taxes. Employment and labor laws also do not apply to independent contractors.

Pay basis: If you pay a worker on an hourly, weekly, or monthly basis, the IRS will consider it a sign the worker is your employee. An independent is generally paid by the job, project, assignment, etc., or receives a commission or similar fee.