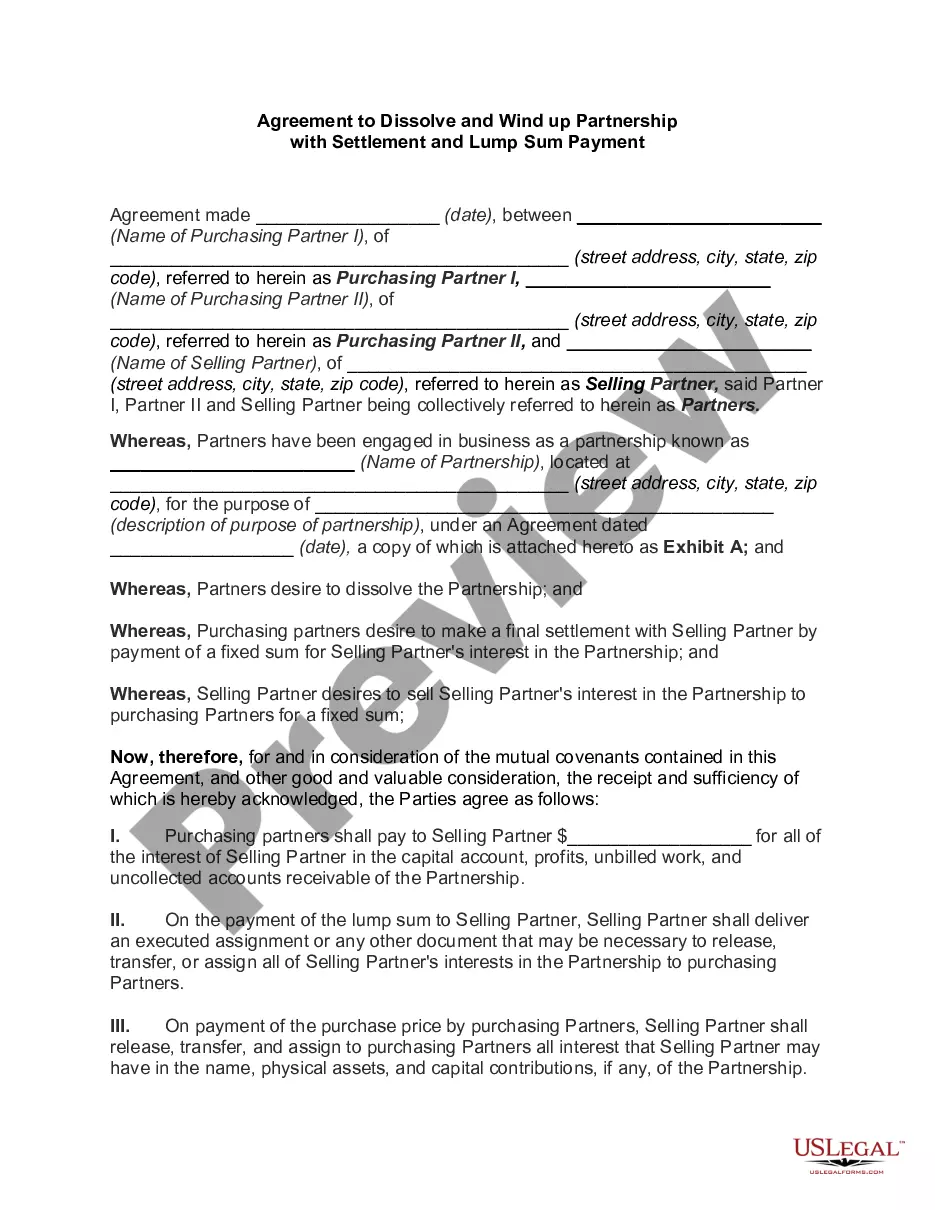

Maine Agreement to Dissolve and Wind up Partnership with Settlement and Lump-sum Payment

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement To Dissolve And Wind Up Partnership With Settlement And Lump-sum Payment?

If you want to be thorough, obtain, or print legal document templates, utilize US Legal Forms, the largest collection of legal forms available online.

Employ the website's user-friendly search function to retrieve the documents you require.

Various templates for business and personal purposes are organized by categories and states, or keywords.

Every legal document template you receive is yours indefinitely. You can access every form you obtained in your account. Click the My documents section and select a form to print or download again.

Stay competitive and acquire, and print the Maine Agreement to Dissolve and Wind Up Partnership with Settlement and Lump-sum Payment with US Legal Forms. There are numerous professional and state-specific forms you can utilize for your business or personal needs.

- Use US Legal Forms to acquire the Maine Agreement to Dissolve and Wind Up Partnership with Settlement and Lump-sum Payment in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and select the Download option to access the Maine Agreement to Dissolve and Wind Up Partnership with Settlement and Lump-sum Payment.

- You can also view forms you previously obtained under the My documents tab in your account.

- If this is your first time using US Legal Forms, follow these steps.

- Step 1. Confirm you have selected the form for the correct jurisdiction.

- Step 2. Use the Preview option to review the content of the form. Be sure to read the description.

- Step 3. If you are not satisfied with the form, utilize the Search area at the top of the screen to find alternative forms in the legal form template.

- Step 4. Once you have found the form you need, click the Get now option. Choose the pricing plan you prefer and enter your information to register for an account.

- Step 5. Complete the transaction. You can utilize your credit card or PayPal account to finalize the purchase.

- Step 6. Select the format of the legal form and download it to your device.

- Step 7. Fill out, modify, and print or sign the Maine Agreement to Dissolve and Wind Up Partnership with Settlement and Lump-sum Payment.

Form popularity

FAQ

The liabilities of the partnership shall rank in order of payment, as follows:Those owing to creditors other than partners,Those owing to partners other than for capital and profits,Those owing to partners in respect of capital,Those owing to partners in respect of profits.

On dissolution of firm, when assets are distributed, liabilities are disposed in a proper order wherein payment to third party debt is on priority, followed by amount due to partners and in the end the residual amount is divided amongst the partners in profit sharing ratio.

Settlement of accounts on dissolutionPayment of the debts of the firm to the third parties.Payment of advances and loans given by the partners.Payment of capital contributed by the partners.The surplus, if any, will be divided among the partners in their profit-sharing ratio.28-Aug-2020

When a partnership dissolves, the individuals involved are no longer partners in a legal sense, but the partnership continues until the business's debts are settled, the legal existence of the business is terminated and the remaining assets of the company have been distributed.

The proceeds from the sale of assets along with the contribution of the partners at the time of dissolution of the firm are first used up to pay off the external liabilities, i.e., the creditors, bank loans, bank overdrafts, bills payable etc.

Dissolution of a limited partnership is the first step toward termination (but termination does not necessarily follow dissolution). The limited partners have no power to dissolve the firm except on court order, and the death or bankruptcy of a limited partner does not dissolve the firm.

The firm will pay the losses including the deficiency of capital firstly out of the profits, secondly out of the partner's capital and lastly by the partners individually in their profit sharing ratio.

An agreement can spell out the order in which liabilities are to be paid, but if it does not, UPA Section 40(a) and RUPA Section 807(1) rank them in this order: (1) to creditors other than partners, (2) to partners for liabilities other than for capital and profits, (3) to partners for capital contributions, and

The proceeds from the sale of assets along with the contribution of the partners at the time of dissolution of the firm are first used up to pay off the external liabilities, i.e., the creditors, bank loans, bank overdrafts, bills payable etc.

An agreement can spell out the order in which liabilities are to be paid, but if it does not, UPA Section 40(a) and RUPA Section 807(1) rank them in this order: (1) to creditors other than partners, (2) to partners for liabilities other than for capital and profits, (3) to partners for capital contributions, and