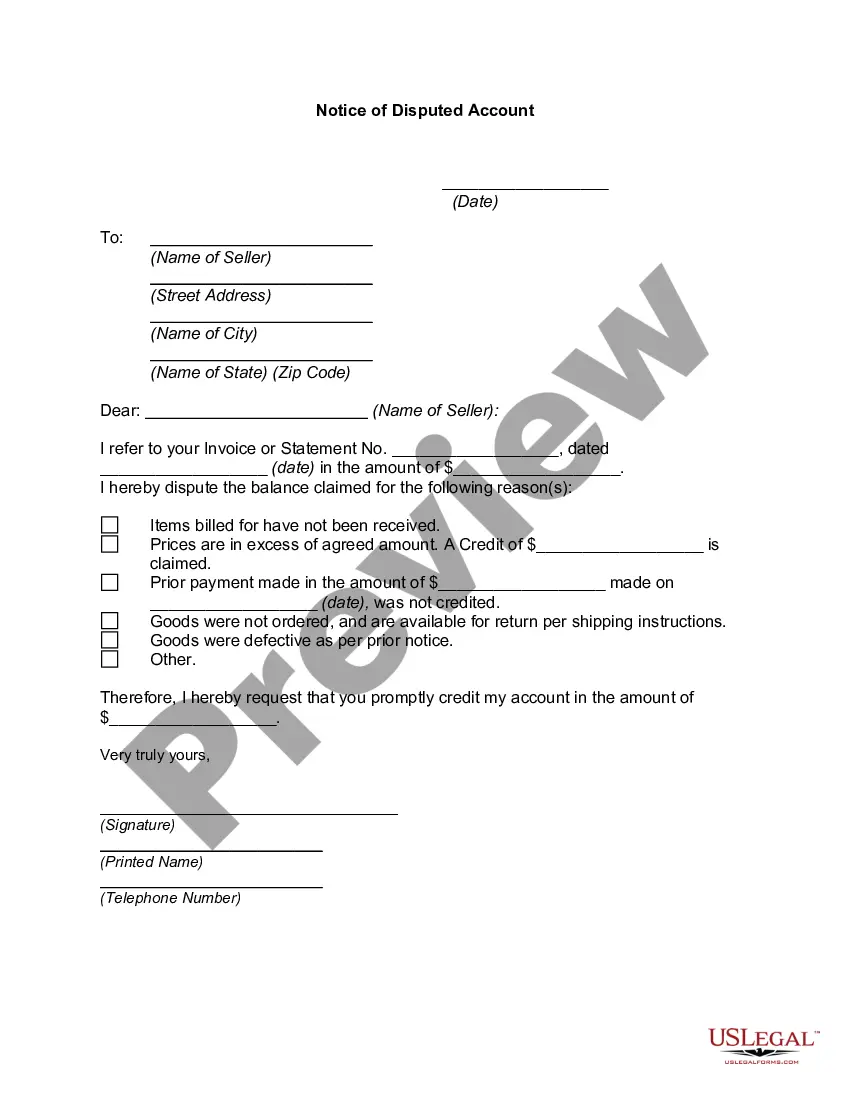

Maine Notice of Disputed Account is a legal document used in the state of Maine to initiate the disputing process for an account. When a consumer believes that there is an error or fraudulent activity in their account, they can send a Notice of Disputed Account to the creditor or collection agency responsible for the account. This notice serves as a formal communication to inform the creditor about the disputed charges or inconsistencies. Maine Notice of Disputed Account includes essential details such as the consumer's personal information, account number, and a clear description of the disputed charges. It is crucial to provide specific and detailed information about each disputed item to aid in the investigation process. The notice should also indicate the desired resolution, whether it be removing the charges or providing additional documentation to clarify the situation. It is essential to send the Maine Notice of Disputed Account via certified mail, return receipt requested, to create a documented record of the dispute. This ensures that the creditor or collection agency cannot claim ignorance of the dispute. Additionally, consumers should retain copies of all correspondences for their records. There are different types of Maine Notice of Disputed Account, depending on the situation. These can include: 1. Maine Notice of Disputed Credit Card Account: Used when disputing charges related to a credit card account, such as unauthorized transactions or billing errors. 2. Maine Notice of Disputed Bank Account: Used when disputing errors or fraudulent activity within a bank account, such as unauthorized withdrawals or incorrect balances. 3. Maine Notice of Disputed Loan Account: Used when disputing loan-related charges, such as incorrect interest rates, improper fees, or unauthorized changes to the loan terms. 4. Maine Notice of Disputed Collection Account: Used when disputing collection accounts, which may contain errors due to inaccurate or outdated information, or cases of mistaken identity. It is important to note that sending a Maine Notice of Disputed Account does not guarantee immediate resolution. The creditor or collection agency is legally required to investigate the dispute within 30 days of receipt and provide a response. During this time, consumers should monitor their accounts closely and maintain all necessary documentation as evidence. Familiarity with the Maine Statute of Limitations is advisable, as it specifies the timeframe within which a creditor can take legal action to collect a debt. If the creditor fails to respond within the allotted time or does not satisfactorily resolve the dispute, consumers may consider seeking legal advice or filing a complaint with the relevant regulatory authorities. In summary, a Maine Notice of Disputed Account is a crucial tool for consumers to address and resolve errors or fraudulent activities within their accounts. By providing a detailed description of the dispute and following the appropriate legal procedures, consumers can protect their rights and ensure a fair resolution.

Maine Notice of Disputed Account

Description

How to fill out Maine Notice Of Disputed Account?

It is feasible to invest numerous hours online looking for the valid document template that aligns with the federal and state requirements you need.

US Legal Forms provides thousands of valid forms that are reviewed by experts.

You can acquire or create the Maine Notice of Disputed Account from our services.

In order to find another edition of the form, utilize the Search section to locate the template that meets your needs and requirements.

- If you have a US Legal Forms account, you can Log In and then press the Acquire button.

- After that, you can complete, modify, generate, or sign the Maine Notice of Disputed Account.

- Every valid document template you purchase belongs to you indefinitely.

- To obtain another version of a purchased form, visit the My documents tab and click the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the simple instructions below.

- First, ensure you have selected the accurate document template for your chosen state/city.

- Review the form description to confirm you have selected the correct one.

Form popularity

FAQ

The statute of limitations on credit card debt in Maine is six years. This means creditors have six years from the date of default to sue for the recovery of funds. Understanding this timeframe is crucial, especially if you receive a collection notice. By utilizing a Maine Notice of Disputed Account, you can safeguard your rights and clarify any disputes regarding the debt.

Writing a letter to dispute a debt involves clearly stating your case and including relevant details. Start with your personal information, the creditor's details, and specify the debt in question. Be sure to mention that you are invoking your rights and that you will be using a Maine Notice of Disputed Account to formally show your disagreement with the charges. This letter can help protect you and clarify your position.

In Maine, debts become uncollectible after their statute of limitations expires, which is typically six years for credit cards. After this period, creditors cannot take legal action to collect the debt. However, they may still attempt to contact you for payment. If you face such situations, consider using a Maine Notice of Disputed Account to formally challenge any claims against you.

Slander of title refers to false statements that harm a person’s ownership rights, making it difficult to sell or transfer property. In Maine, a claim can arise if such statements are made maliciously. If you believe you have a case involving slander of title and you need to clarify your title options, ensuring your Maine Notice of Disputed Account reflects accurate statements is vital. Consulting legal resources can help you secure your interests.

Maine has specific regulations regarding medical debts, including limits on how creditors can collect these debts. They must provide clear documentation and disputes can be raised through a Maine Notice of Disputed Account. If you are confused about your rights or the validity of the debt, exploring resources like the UsLegalForms platform can give you the guidance you need to address your medical debt concerns.

In Maine, the time allowed to sue someone typically ranges from six to only 20 years, depending on the nature of the claim. For most personal injury cases, the limit is six years. If you plan to dispute an account or resolve a Maine Notice of Disputed Account, acting promptly is essential. Engaging with legal services can streamline your process.

In Maine, you generally have six years to file a personal injury claim after an accident. This timeframe allows victims to gather necessary evidence and assess their damages. If you find yourself navigating a Maine Notice of Disputed Account related to medical expenses from an accident, it is crucial to act within this period. Seeking professional assistance can help clarify your options.

Suing someone after 20 years can be challenging in Maine due to the statute of limitations. Most claims must be filed within a specific time frame, which, as mentioned, is typically six years for contracts. However, if the account is still valid under Maine law, addressing the Maine Notice of Disputed Account with the proper legal channels would be pivotal. Understanding your rights is essential.

In Maine, you typically have six years to file a civil lawsuit for most claims, including those associated with a Maine Notice of Disputed Account. However, specific time limits may apply based on the nature of the dispute. It is crucial to act quickly to ensure that your rights are protected. USLegalForms can provide you with the necessary tools and information to file your civil suit efficiently.

Rule of Civil Procedure 60 in Maine grants the court the authority to relieve a party from a judgment or order under specific circumstances. If you find yourself in a situation related to a Maine Notice of Disputed Account, this rule might allow you to reopen a case due to newly discovered evidence or errors. Understanding this rule can be instrumental in ensuring that justice is served. For detailed guidance, consider using the resources available on USLegalForms.

More info

General Provisions Maine state civil procedure law. Title 3-7A. Subchapter I-J. Litigants Rights-Misc. Maine Judiciary Code, Title 11, Section 3523 Title 11, Chapter 35. Statewide Judicial Services Title 12. General Provisions Maine General Statutes Chapter 11, Title 16, Chapter 13-A. Judicial Process Title 12, Chapter 13-A. Judicial Procedure Title 37. Legal Services Title 36. Labor Relations Title 38. Public Education Maine Revised Statutes Chapter 8B, Chapter 11. Discharge from Employment Title 28, Chapter 34, Chapter 35. Mental Health and Substance Abuse Services Title 40, Chapter 43. Workers' Compensation Maine Supreme Court Judicial Department — Civil Remedies Maine Supreme Court Judicial Department — Dismissal from Public Employment Maine Constitution — State Constitution New Hampshire — Judiciary in General Statutes New Hampshire Revised Statutes, Chapter 546: (a) The name, occupation or profession of the judge or justice or of the judge or justice's office.