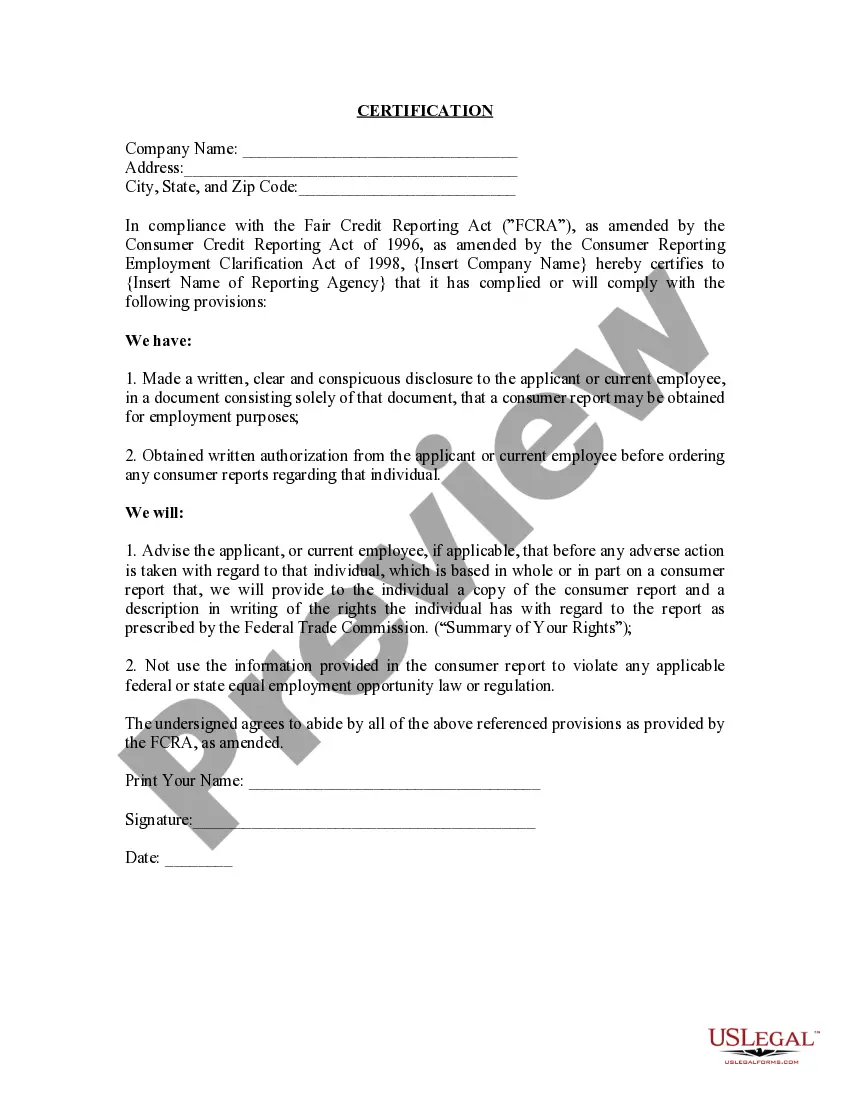

Maine FCRA Certification Letter to Consumer Reporting Agency: A Comprehensive Guide The Maine FCRA Certification Letter to Consumer Reporting Agency ensures compliance with the Fair Credit Reporting Act (FCRA) and enables individuals to exercise their rights as consumers regarding the accuracy and privacy of their credit information. This letter is a crucial tool for asserting consumer rights and rectifying errors or discrepancies in credit reports maintained by consumer reporting agencies (Crash). The Maine FCRA Certification Letter typically includes the following elements: 1. Personal Information: The letter should begin with the consumer's full name, current address, and contact details, including phone number and email address, to facilitate communication between the consumer and the CRA. 2. Identification: It is essential to include proof of identity, such as a copy of the consumer's driver's license or other official identification documents, to ensure the CRA can verify the legitimacy of the request. 3. Reference to the FCRA: The letter must make clear reference to the FCRA and state that the consumer is initiating a request in accordance with the Act. This emphasizes the consumer's understanding of their rights and ensures the CRA recognizes the legal obligations it must fulfill. 4. Nature of Dispute: The letter should accurately describe the nature of the dispute. This may include detailing the specific errors, inaccuracies, or incomplete information found within the credit report, such as incorrect personal information, inaccurate account details, or unauthorized inquiries. 5. Supporting Evidence: The consumer may choose to include supporting documents, such as receipts, correspondence, or account statements, to substantiate their claims. These documents will strengthen the consumer's case and provide the CRA with tangible evidence. 6. Request for Investigation: The Maine FCRA Certification Letter should explicitly request that the CRA promptly investigate the disputed items and make appropriate corrections or deletions according to the FCRA guidelines. 7. Timeframe for Response: The letter should state that the CRA must respond within 30 days of receiving the letter to comply with the FCRA. Additionally, the consumer may request a written confirmation of the actions taken by the CRA to resolve the dispute. Different types of Maine FCRA Certification Letters to Consumer Reporting Agency may include: 1. Standard Dispute: This is the most common type of letter, asserting the consumer's rights under the FCRA and requesting an investigation into disputed items on the credit report. 2. Identity Theft: In cases of suspected identity theft, consumers may submit a FCRA Certification Letter seeking the CRA's assistance in investigating fraudulent accounts or inquiries and recovering their identity. 3. Credit Freeze: Individuals concerned about potential unauthorized access to their credit reports may request a credit freeze through a Maine FCRA Certification Letter, ensuring that no new credit accounts can be opened without their explicit consent. 4. Opt-Out: Consumers who wish to limit the amount of unsolicited offers of credit and insurance they receive can use a FCRA Certification Letter to request that their names be removed from prescreened offer lists. In sum, the Maine FCRA Certification Letter is a crucial instrument for consumers to exercise their rights under the FCRA. By providing a detailed description of the disputed items and requesting a comprehensive investigation, individuals can rectify errors, protect their credit information, and maintain accurate credit reports.

Maine FCRA Certification Letter to Consumer Reporting Agency

Description

How to fill out Maine FCRA Certification Letter To Consumer Reporting Agency?

You may invest time on the Internet trying to find the authorized file format which fits the state and federal specifications you will need. US Legal Forms supplies thousands of authorized forms which can be evaluated by professionals. You can easily down load or print out the Maine FCRA Certification Letter to Consumer Reporting Agency from our service.

If you have a US Legal Forms account, you are able to log in and click the Acquire switch. Following that, you are able to full, change, print out, or sign the Maine FCRA Certification Letter to Consumer Reporting Agency. Each and every authorized file format you get is your own property forever. To acquire another backup for any purchased type, visit the My Forms tab and click the related switch.

If you are using the US Legal Forms website initially, follow the easy instructions beneath:

- Initially, make certain you have chosen the proper file format for that region/metropolis of your choice. Browse the type outline to ensure you have chosen the proper type. If offered, use the Review switch to check through the file format also.

- If you want to discover another variation in the type, use the Look for industry to obtain the format that meets your requirements and specifications.

- Upon having identified the format you need, simply click Buy now to carry on.

- Pick the rates plan you need, type your accreditations, and register for a merchant account on US Legal Forms.

- Comprehensive the financial transaction. You should use your bank card or PayPal account to fund the authorized type.

- Pick the structure in the file and down load it in your system.

- Make alterations in your file if possible. You may full, change and sign and print out Maine FCRA Certification Letter to Consumer Reporting Agency.

Acquire and print out thousands of file web templates making use of the US Legal Forms web site, that provides the largest collection of authorized forms. Use professional and state-specific web templates to take on your company or specific needs.