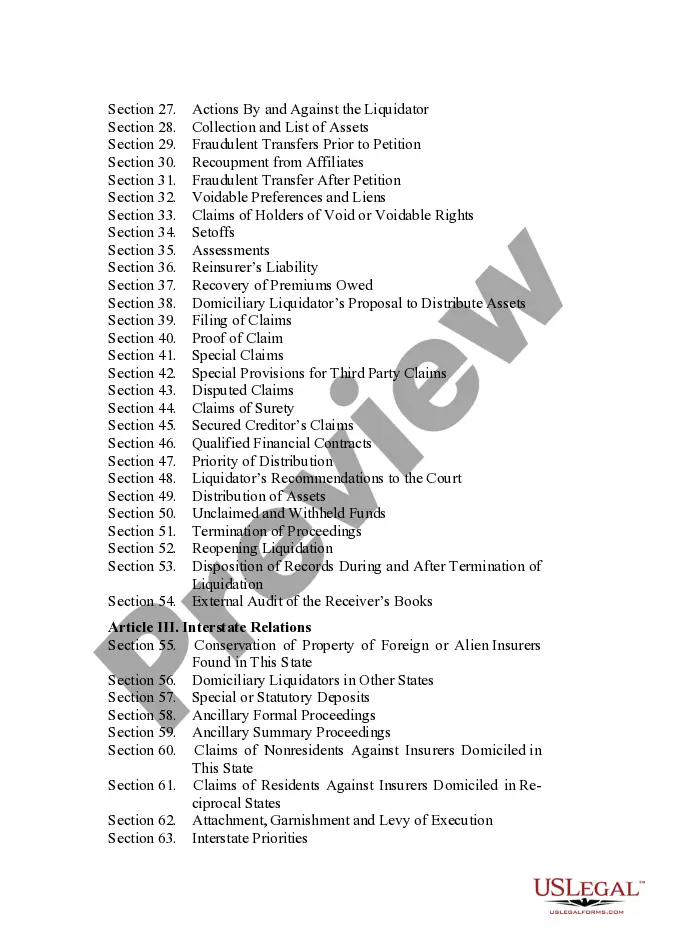

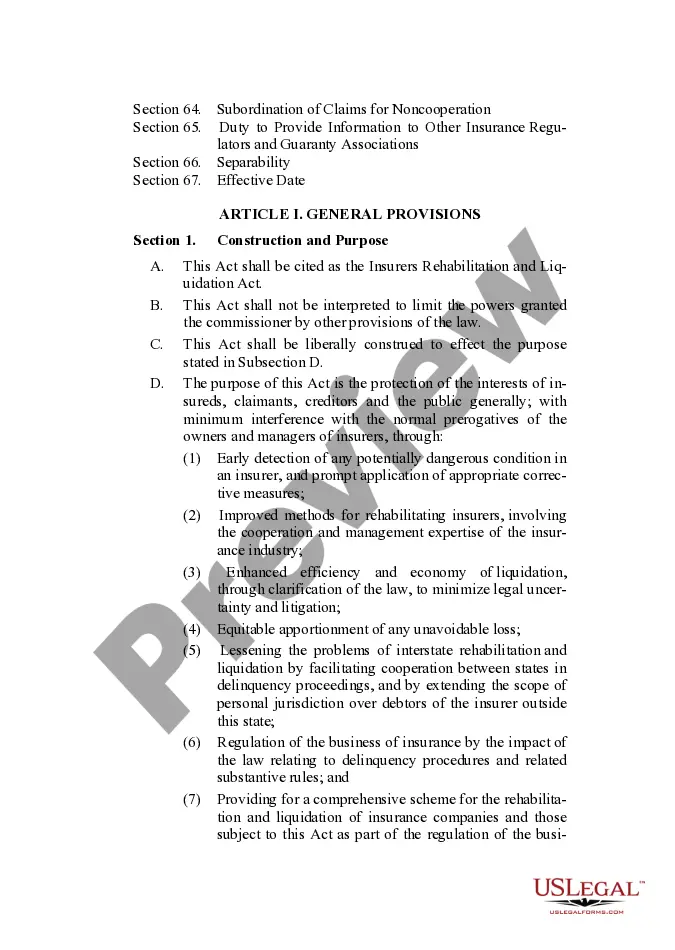

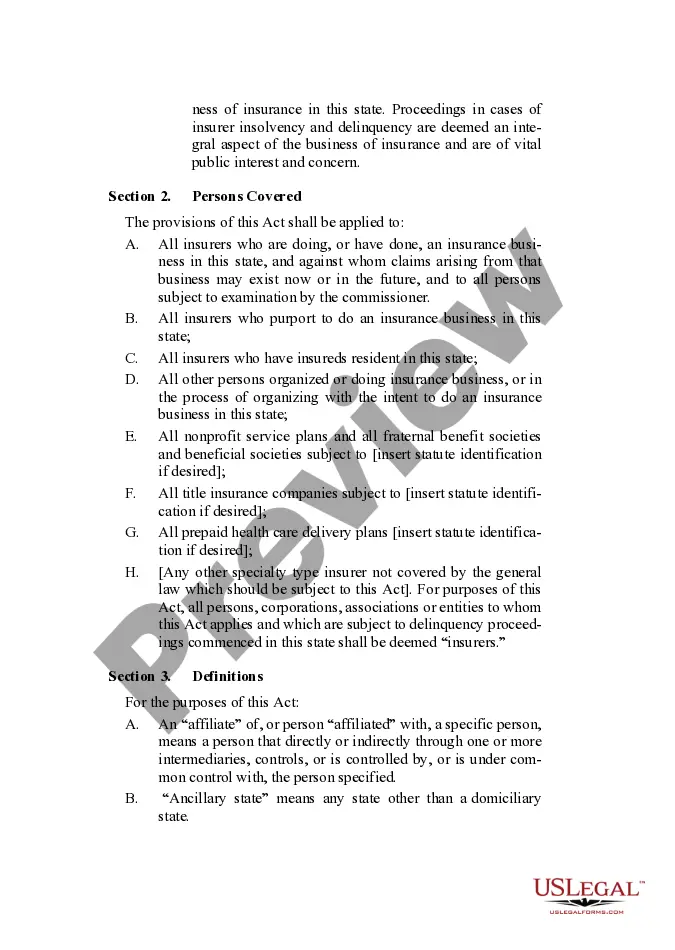

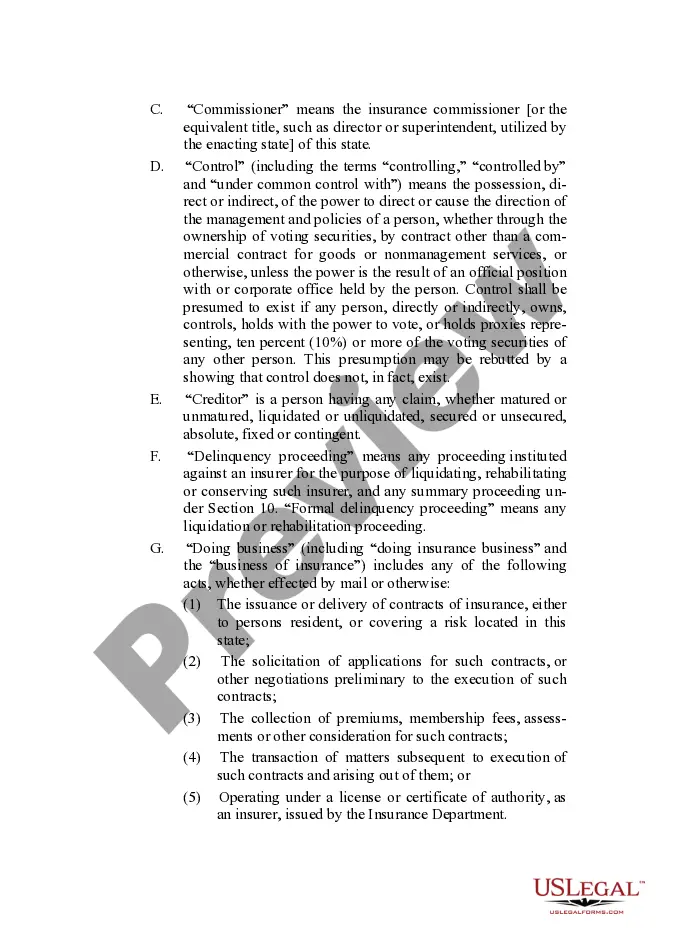

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

Maine Insurers Rehabilitation and Liquidation Model Act is a legal framework introduced by the state of Maine to govern the rehabilitation and liquidation of insurance companies. This act provides guidelines and procedures to protect policyholders and other interested parties in case of insolvency or financial distress of an insurance company. Also known as the "Maine Model Act," it outlines the steps and actions that the Maine Bureau of Insurance (MOI) can take to rehabilitate or liquidate an insolvent insurer. The act aims to ensure the orderly and efficient process of resolving financial issues faced by insurance companies, safeguarding the interests of policyholders, creditors, and other stakeholders. Under the Maine Insurers Rehabilitation and Liquidation Model Act, the MOI has the authority to take control of an insolvent insurer and initiate rehabilitation efforts. Rehabilitation involves attempting to restore the insurer to a financially healthy state so that it can continue serving its policyholders. If rehabilitation is deemed unfeasible, the act allows for the liquidation of the insurer. Liquidation involves the sale of the insurer's assets to pay off its debts and obligations in an orderly manner. The act provides guidelines on asset distribution, creditor priorities, and the appointment of a liquidator to oversee the process. The Maine Insurers Rehabilitation and Liquidation Model Act contains several key provisions, including: 1. Rehabilitation Plan: The act outlines the requirements for developing a rehabilitation plan, which must be approved by the court overseeing the process. 2. Automatic Stay: Once rehabilitation or liquidation proceedings are initiated, an automatic stay is put in place, preventing policyholders and creditors from taking legal action against the insurer. 3. Policyholder Protection: The act places emphasis on protecting policyholders' interests, ensuring that their claims are prioritized during the rehabilitation or liquidation process. 4. Guaranty Associations: The act addresses the role and involvement of state insurance guaranty associations, which may provide protection to policyholders to a certain extent in case an insurance company becomes insolvent. It is important to note that the Maine Insurers Rehabilitation and Liquidation Model Act is unique to the state of Maine. Other states may have their own versions of rehabilitation and liquidation acts, but the focus here is specifically on the Maine Model Act.Maine Insurers Rehabilitation and Liquidation Model Act is a legal framework introduced by the state of Maine to govern the rehabilitation and liquidation of insurance companies. This act provides guidelines and procedures to protect policyholders and other interested parties in case of insolvency or financial distress of an insurance company. Also known as the "Maine Model Act," it outlines the steps and actions that the Maine Bureau of Insurance (MOI) can take to rehabilitate or liquidate an insolvent insurer. The act aims to ensure the orderly and efficient process of resolving financial issues faced by insurance companies, safeguarding the interests of policyholders, creditors, and other stakeholders. Under the Maine Insurers Rehabilitation and Liquidation Model Act, the MOI has the authority to take control of an insolvent insurer and initiate rehabilitation efforts. Rehabilitation involves attempting to restore the insurer to a financially healthy state so that it can continue serving its policyholders. If rehabilitation is deemed unfeasible, the act allows for the liquidation of the insurer. Liquidation involves the sale of the insurer's assets to pay off its debts and obligations in an orderly manner. The act provides guidelines on asset distribution, creditor priorities, and the appointment of a liquidator to oversee the process. The Maine Insurers Rehabilitation and Liquidation Model Act contains several key provisions, including: 1. Rehabilitation Plan: The act outlines the requirements for developing a rehabilitation plan, which must be approved by the court overseeing the process. 2. Automatic Stay: Once rehabilitation or liquidation proceedings are initiated, an automatic stay is put in place, preventing policyholders and creditors from taking legal action against the insurer. 3. Policyholder Protection: The act places emphasis on protecting policyholders' interests, ensuring that their claims are prioritized during the rehabilitation or liquidation process. 4. Guaranty Associations: The act addresses the role and involvement of state insurance guaranty associations, which may provide protection to policyholders to a certain extent in case an insurance company becomes insolvent. It is important to note that the Maine Insurers Rehabilitation and Liquidation Model Act is unique to the state of Maine. Other states may have their own versions of rehabilitation and liquidation acts, but the focus here is specifically on the Maine Model Act.