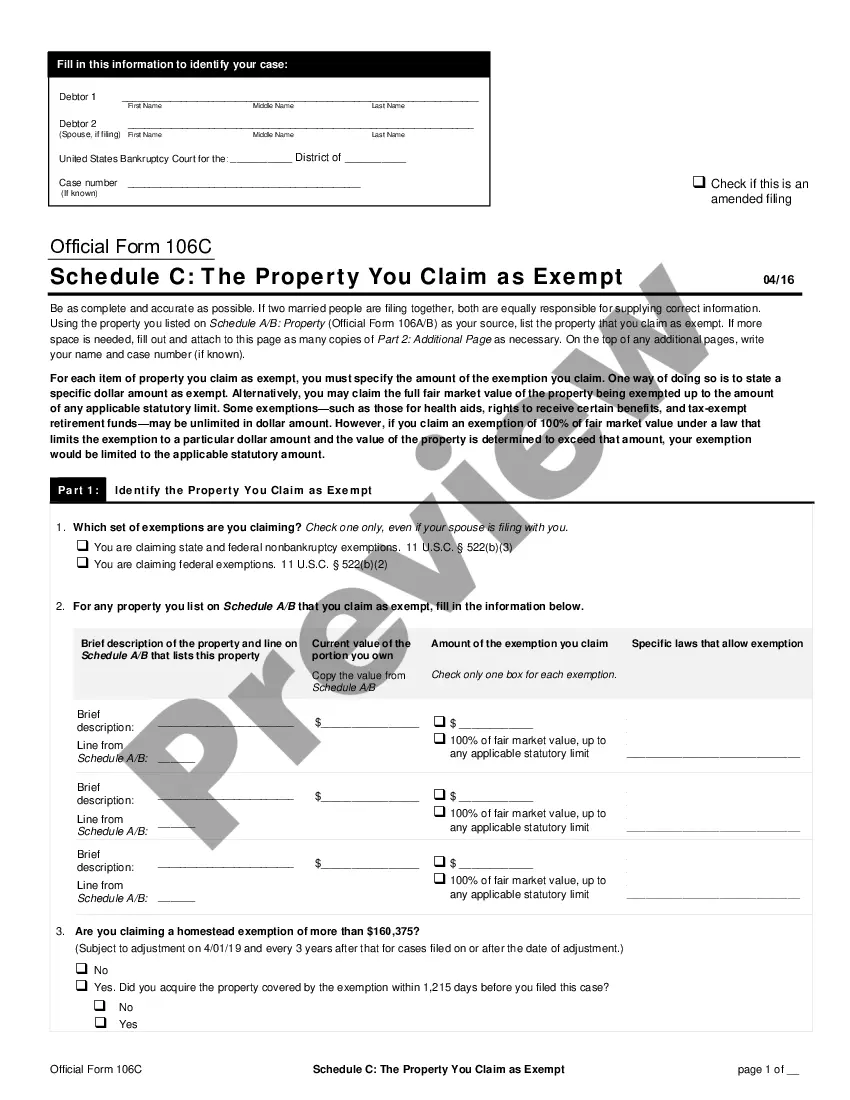

This form is Schedule C. The form may be used to list information concerning exempt property. The form contains the following categories: description of the property; value of the claimed exemption; and current market value of the property. This form is data enabled to comply with CM/ECF electronic filing standards. This form is for post 2005 act cases.

Maine Property Claimed as Exempt - Schedule C - Form 6C - Post 2005

Instant download

This website is not affiliated with any governmental entity

Public form

Description

How to fill out Property Claimed As Exempt - Schedule C - Form 6C - Post 2005?

US Legal Forms - one of several biggest libraries of legitimate kinds in the States - gives a variety of legitimate document layouts it is possible to down load or produce. While using internet site, you can find thousands of kinds for business and individual uses, sorted by types, states, or keywords and phrases.You can find the most recent versions of kinds like the Maine Property Claimed as Exempt - Schedule C - Form 6C - Post 2005 within minutes.

If you currently have a monthly subscription, log in and down load Maine Property Claimed as Exempt - Schedule C - Form 6C - Post 2005 from the US Legal Forms catalogue. The Acquire option will appear on each and every kind you see. You get access to all earlier saved kinds within the My Forms tab of your respective profile.

If you wish to use US Legal Forms the very first time, allow me to share easy instructions to help you get started out:

- Ensure you have chosen the right kind for your personal city/state. Click the Preview option to examine the form`s content material. See the kind explanation to ensure that you have chosen the correct kind.

- In case the kind does not match your requirements, make use of the Look for discipline near the top of the screen to get the one who does.

- Should you be happy with the form, affirm your choice by clicking the Purchase now option. Then, select the pricing prepare you like and supply your references to sign up to have an profile.

- Procedure the deal. Use your bank card or PayPal profile to complete the deal.

- Select the file format and down load the form on your own system.

- Make alterations. Complete, revise and produce and signal the saved Maine Property Claimed as Exempt - Schedule C - Form 6C - Post 2005.

Every single template you included with your bank account lacks an expiry day and is your own eternally. So, in order to down load or produce one more version, just check out the My Forms segment and click about the kind you want.

Gain access to the Maine Property Claimed as Exempt - Schedule C - Form 6C - Post 2005 with US Legal Forms, the most comprehensive catalogue of legitimate document layouts. Use thousands of skilled and condition-specific layouts that meet your business or individual needs and requirements.

Form popularity

FAQ

(Official Form 106C) lists the property that you believe you are entitled to keep. If you do not claim the property on this form, it will not be exempted, despite your rights under the law. Before filling out this form, you have to decide whether you will use your state exemptions or the federal exemptions.