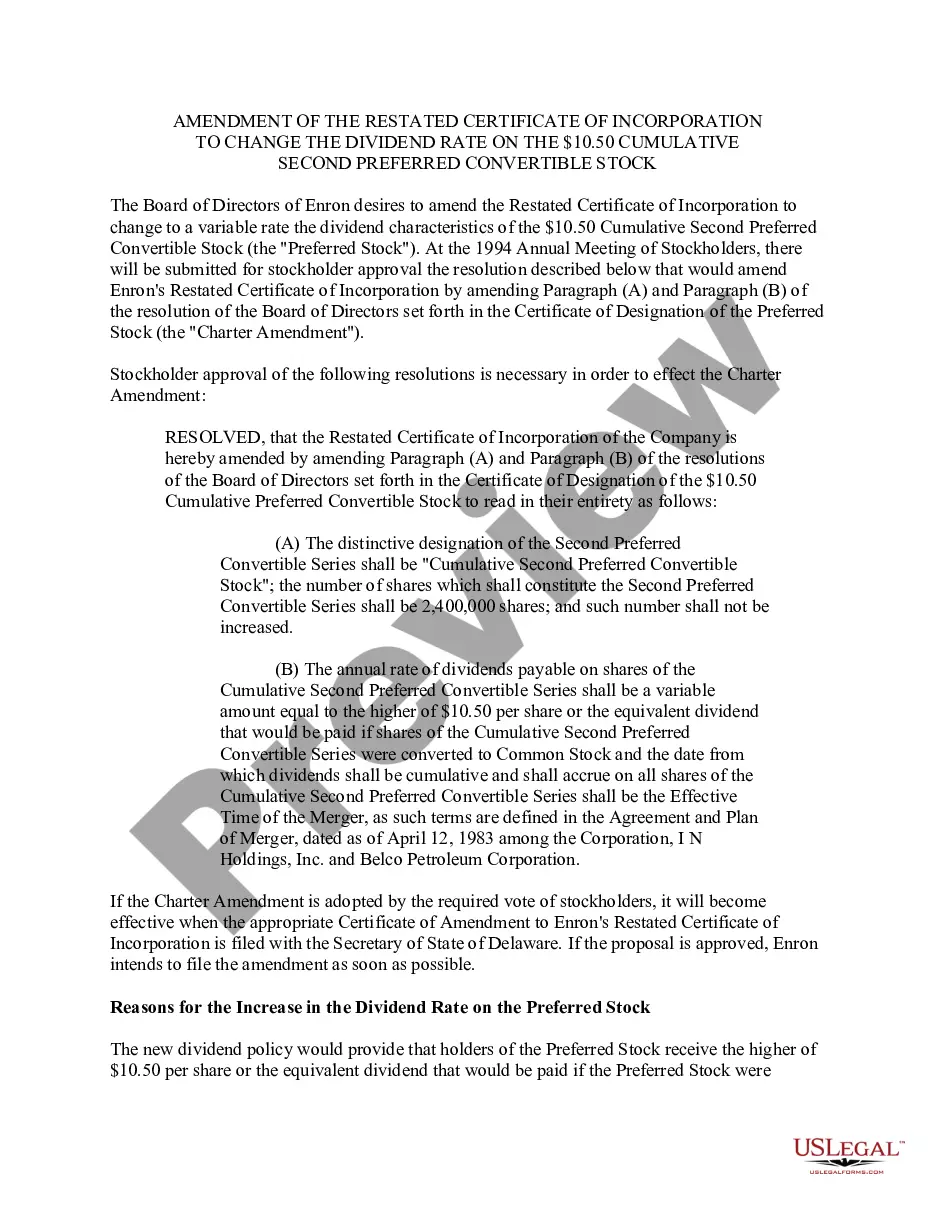

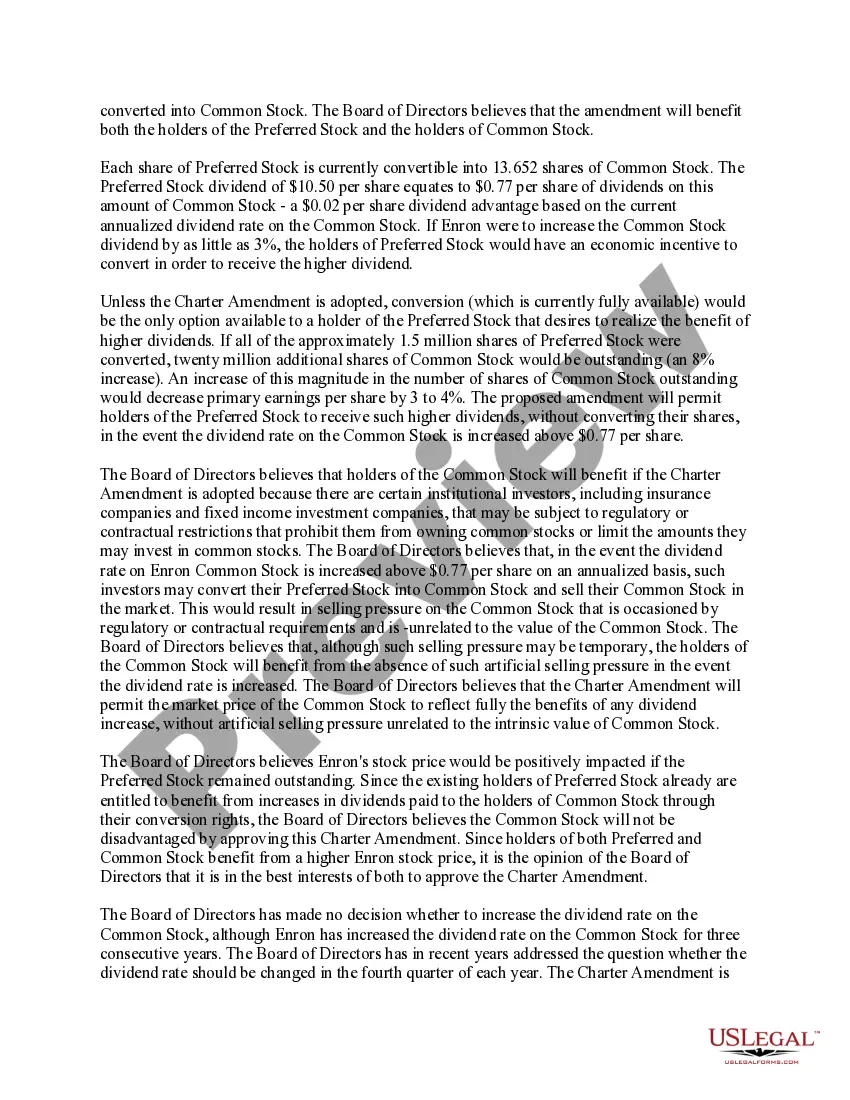

Maine Amendment of Restated Certificate of Incorporation to Change Dividend Rate on $10.50 Cumulative Second Preferred Convertible Stock The Maine Amendment of Restated Certificate of Incorporation is a legal document that allows a company to modify its existing dividend rate on the $10.50 cumulative second preferred convertible stock. This amendment alters the terms and conditions associated with this specific class of stock, providing potential benefits for both the company and its shareholders. Keywords: Maine Amendment, Restated Certificate of Incorporation, dividend rate, $10.50 cumulative second preferred convertible stock Types of Maine Amendments of Restated Certificate of Incorporation to Change Dividend Rate on $10.50 Cumulative Second Preferred Convertible Stock: 1. Increase in Dividend Rate: This type of Maine Amendment of Restated Certificate of Incorporation seeks to enhance the dividend rate associated with the $10.50 cumulative second preferred convertible stock. By modifying the terms, the company aims to provide a higher return to stockholders holding this particular class of stock. 2. Decrease in Dividend Rate: Conversely, this amendment decreases the dividend rate connected to the $10.50 cumulative second preferred convertible stock. Companies might undertake this change due to various factors such as financial constraints or strategic business decisions aimed at optimizing resources. 3. Variable Dividend Rate: In some cases, companies might choose to implement a variable dividend rate on the $10.50 cumulative second preferred convertible stock. This type of amendment allows the dividend rate to fluctuate based on specific predetermined criteria, such as the company's financial performance or industry dynamics. 4. Conversion Rate Adjustment: Apart from modifying the dividend rate, the Maine Amendment of Restated Certificate of Incorporation can also address adjustments to the conversion rate of the $10.50 cumulative second preferred convertible stock. This change ensures that stockholders receive a fair conversion ratio, taking into consideration factors like stock splits, stock dividends, or other corporate events. 5. Retrospective Dividend Rate Modification: This amendment type alters the dividend rate retroactively on the $10.50 cumulative second preferred convertible stock. It accounts for situations where the company determines that a different rate should have been in place previously due to errors, miscalculations, or other unforeseen circumstances. Overall, the Maine Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock allows for customized adjustments in the shareholder's benefits and represents an essential aspect of corporate governance.

Maine Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Maine Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Have you been within a position the place you will need paperwork for possibly enterprise or individual purposes virtually every day? There are plenty of legal record templates available on the Internet, but finding versions you can rely is not straightforward. US Legal Forms delivers thousands of develop templates, just like the Maine Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, that happen to be created to satisfy federal and state requirements.

In case you are presently informed about US Legal Forms web site and also have an account, just log in. After that, it is possible to down load the Maine Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock format.

If you do not come with an profile and wish to begin to use US Legal Forms, abide by these steps:

- Discover the develop you will need and ensure it is for that correct area/area.

- Take advantage of the Preview button to review the shape.

- Browse the explanation to ensure that you have chosen the correct develop.

- When the develop is not what you`re searching for, make use of the Look for industry to find the develop that fits your needs and requirements.

- Once you obtain the correct develop, simply click Get now.

- Select the pricing prepare you want, fill out the necessary information to produce your account, and purchase your order using your PayPal or bank card.

- Decide on a hassle-free paper formatting and down load your duplicate.

Find all of the record templates you may have bought in the My Forms menus. You can get a additional duplicate of Maine Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock at any time, if possible. Just go through the required develop to down load or print out the record format.

Use US Legal Forms, the most considerable selection of legal forms, to conserve time and stay away from mistakes. The support delivers appropriately produced legal record templates that you can use for a selection of purposes. Generate an account on US Legal Forms and initiate making your life easier.