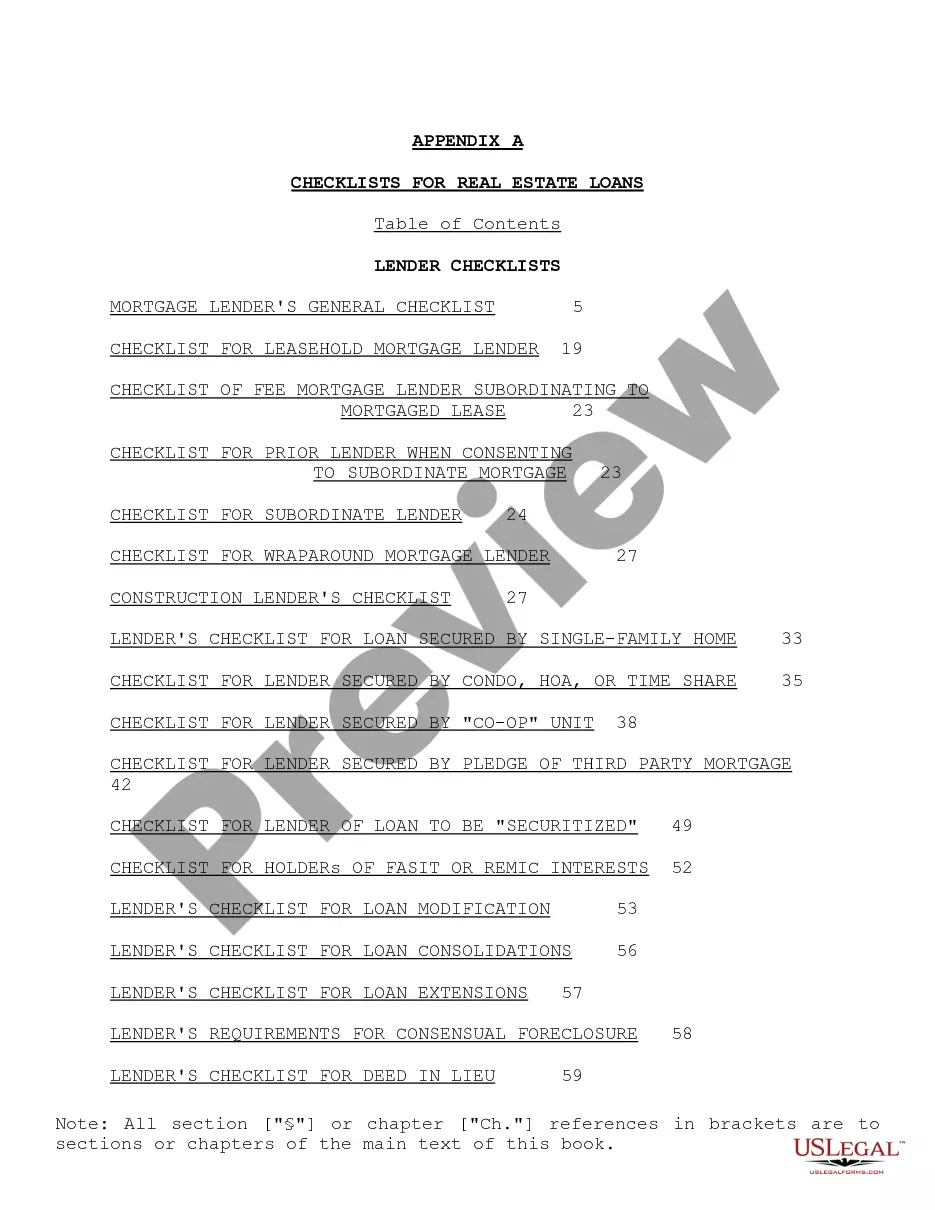

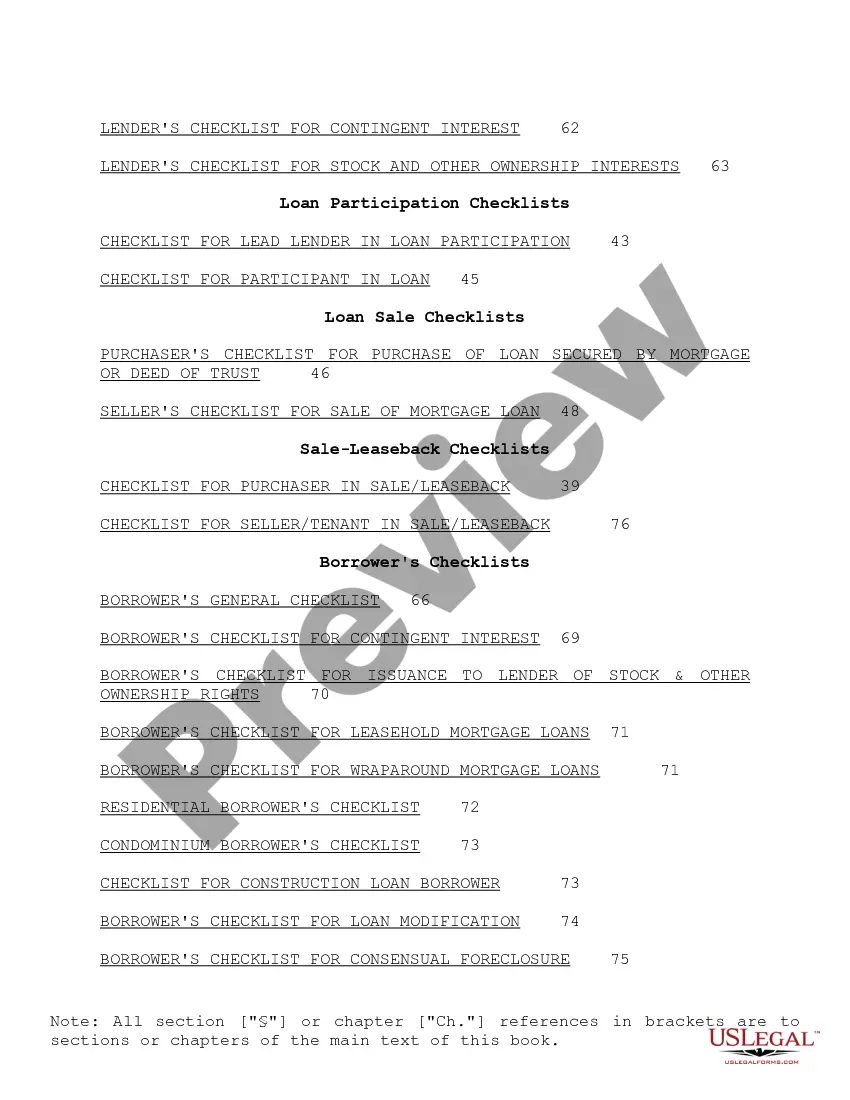

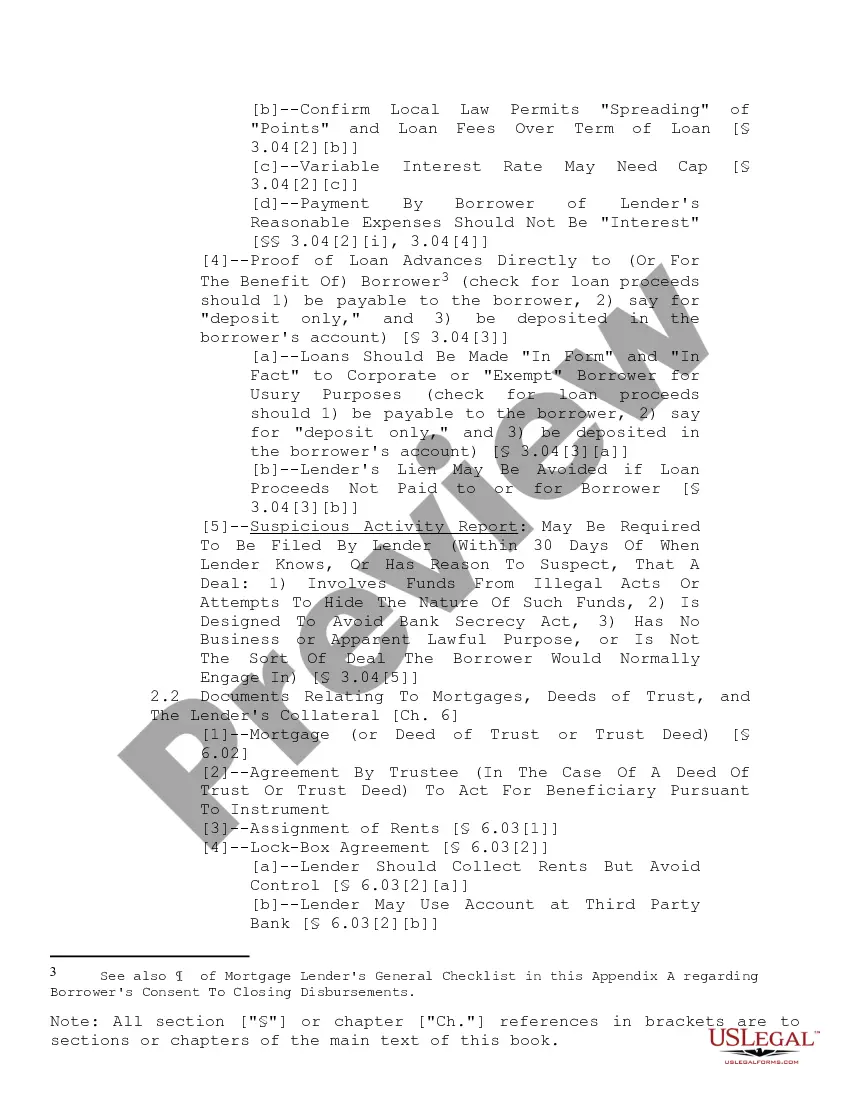

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Maine Real Estate Loans Checklist: A Comprehensive Guide to Ensure a Smooth Loan Process When it comes to obtaining a real estate loan in Maine, being prepared is key to streamline the lending process and increase your chances of securing the funding you need. To help you through this process, we have created a detailed Maine Checklist for Real Estate Loans that covers all the important aspects you need to consider. 1. Credit History: Start by reviewing your credit history and ensure it demonstrates responsible financial behavior. Lenders in Maine will take this into consideration when determining your loan eligibility and interest rates. Keep in mind any outstanding debts, missed payments, or errors that may affect your credit score. 2. Income and Employment Documentation: Compile all the necessary documents, including pay stubs, tax returns, and employment verification letters. Lenders will require this information to evaluate your financial stability and assess your ability to repay the loan. 3. Down Payment: Determine the amount you can comfortably put towards the down payment on your desired property. This will impact the loan-to-value ratio and affect the terms and interest rates offered by the lender. Having a solid down payment demonstrates your commitment to the investment and may improve your chances of securing the loan. 4. Property Evaluation: Conduct a thorough evaluation of the property you intend to purchase. This includes obtaining an appraisal and a home inspection report to assess its market value and condition. Lenders may require these reports to ensure the property is worth the loan amount. 5. Mortgage Options: Familiarize yourself with the different mortgage options available in Maine. Some common types include fixed-rate mortgages, adjustable-rate mortgages, FHA loans, and VA loans. Each option has its own set of requirements, benefits, and potential risks, so choose the one that aligns best with your financial goals and circumstances. 6. Loan Pre-Approval: Consider getting pre-approved for a loan before starting your property search. Mortgage pre-approval gives you a clear understanding of your budget, making it easier to narrow down your options and negotiate with sellers. It also demonstrates your seriousness as a buyer, potentially giving you an advantage in a competitive market. Types of Maine Checklist for Real Estate Loans: 1. Residential Real Estate Loans: Designed for individuals or families purchasing single-family homes, duplexes, condos, or townhouses in Maine. 2. Commercial Real Estate Loans: Aimed at entrepreneurs or businesses looking to purchase or refinance properties for commercial purposes, including office buildings, retail spaces, and warehouses. 3. Construction Loans: Intended for individuals or developers planning to build a residential or commercial property in Maine. This type of loan typically provides funds in installments as the construction progresses. 4. Refinancing Loans: These loans allow homeowners in Maine to replace their current mortgage with a new one to take advantage of lower interest rates, change loan terms, or access the equity built in the property. By following this detailed Maine Checklist for Real Estate Loans, you'll be well-prepared to navigate the loan process and increase your chances of securing financing on favorable terms. Remember to consult with a local mortgage professional to ensure you're well-informed about the specific requirements and regulations in Maine.Maine Real Estate Loans Checklist: A Comprehensive Guide to Ensure a Smooth Loan Process When it comes to obtaining a real estate loan in Maine, being prepared is key to streamline the lending process and increase your chances of securing the funding you need. To help you through this process, we have created a detailed Maine Checklist for Real Estate Loans that covers all the important aspects you need to consider. 1. Credit History: Start by reviewing your credit history and ensure it demonstrates responsible financial behavior. Lenders in Maine will take this into consideration when determining your loan eligibility and interest rates. Keep in mind any outstanding debts, missed payments, or errors that may affect your credit score. 2. Income and Employment Documentation: Compile all the necessary documents, including pay stubs, tax returns, and employment verification letters. Lenders will require this information to evaluate your financial stability and assess your ability to repay the loan. 3. Down Payment: Determine the amount you can comfortably put towards the down payment on your desired property. This will impact the loan-to-value ratio and affect the terms and interest rates offered by the lender. Having a solid down payment demonstrates your commitment to the investment and may improve your chances of securing the loan. 4. Property Evaluation: Conduct a thorough evaluation of the property you intend to purchase. This includes obtaining an appraisal and a home inspection report to assess its market value and condition. Lenders may require these reports to ensure the property is worth the loan amount. 5. Mortgage Options: Familiarize yourself with the different mortgage options available in Maine. Some common types include fixed-rate mortgages, adjustable-rate mortgages, FHA loans, and VA loans. Each option has its own set of requirements, benefits, and potential risks, so choose the one that aligns best with your financial goals and circumstances. 6. Loan Pre-Approval: Consider getting pre-approved for a loan before starting your property search. Mortgage pre-approval gives you a clear understanding of your budget, making it easier to narrow down your options and negotiate with sellers. It also demonstrates your seriousness as a buyer, potentially giving you an advantage in a competitive market. Types of Maine Checklist for Real Estate Loans: 1. Residential Real Estate Loans: Designed for individuals or families purchasing single-family homes, duplexes, condos, or townhouses in Maine. 2. Commercial Real Estate Loans: Aimed at entrepreneurs or businesses looking to purchase or refinance properties for commercial purposes, including office buildings, retail spaces, and warehouses. 3. Construction Loans: Intended for individuals or developers planning to build a residential or commercial property in Maine. This type of loan typically provides funds in installments as the construction progresses. 4. Refinancing Loans: These loans allow homeowners in Maine to replace their current mortgage with a new one to take advantage of lower interest rates, change loan terms, or access the equity built in the property. By following this detailed Maine Checklist for Real Estate Loans, you'll be well-prepared to navigate the loan process and increase your chances of securing financing on favorable terms. Remember to consult with a local mortgage professional to ensure you're well-informed about the specific requirements and regulations in Maine.