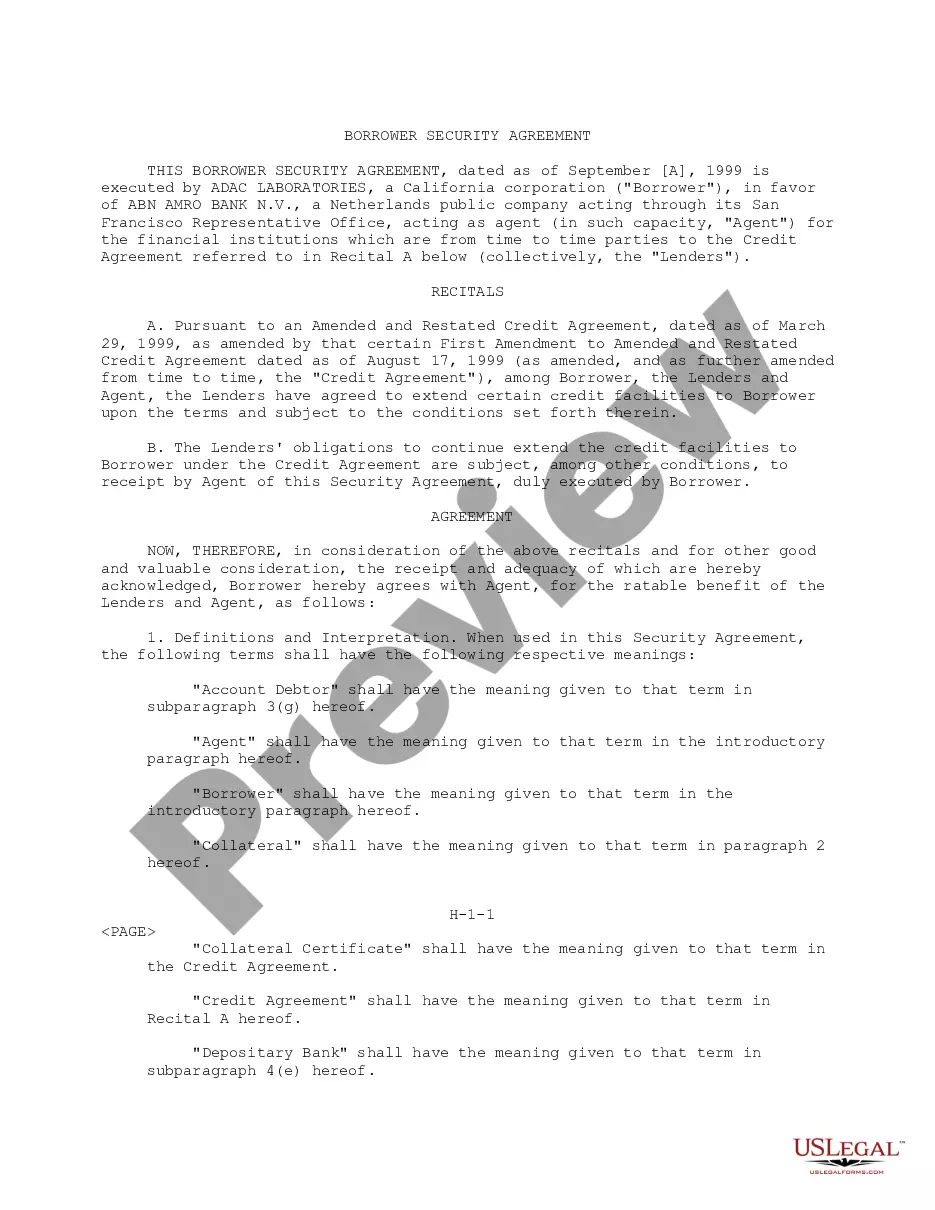

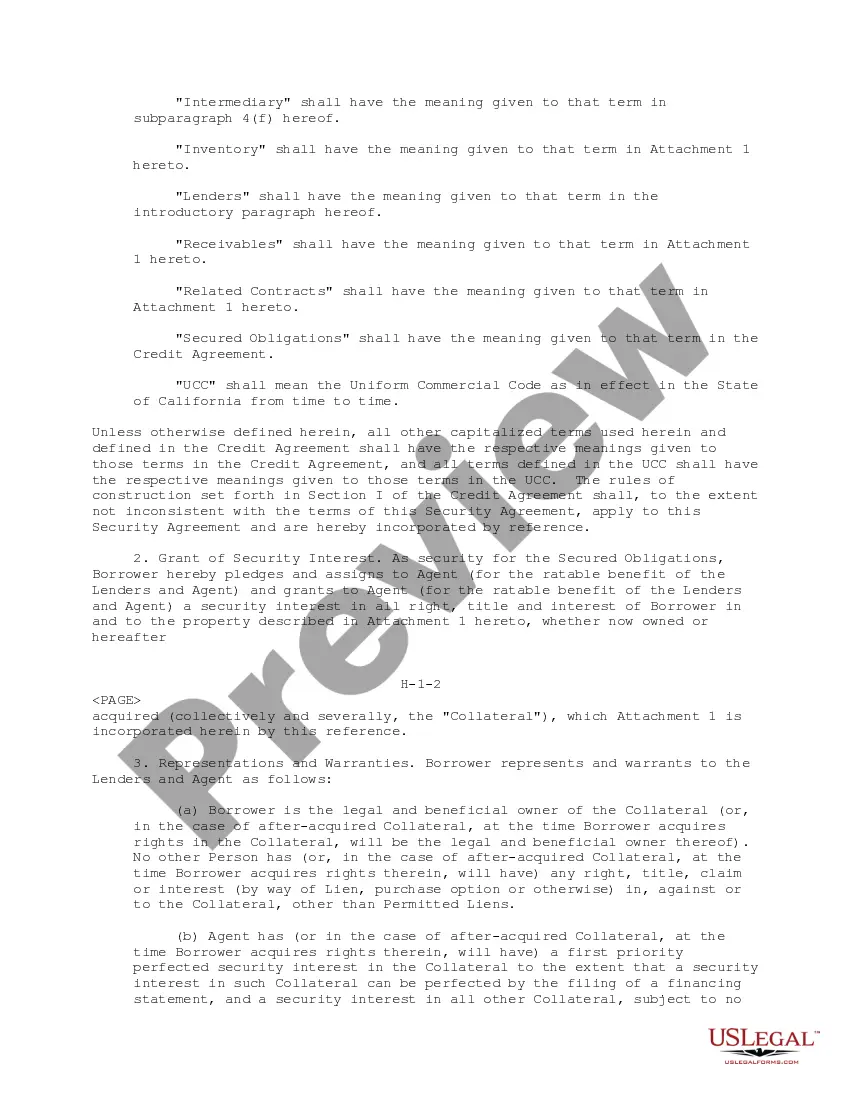

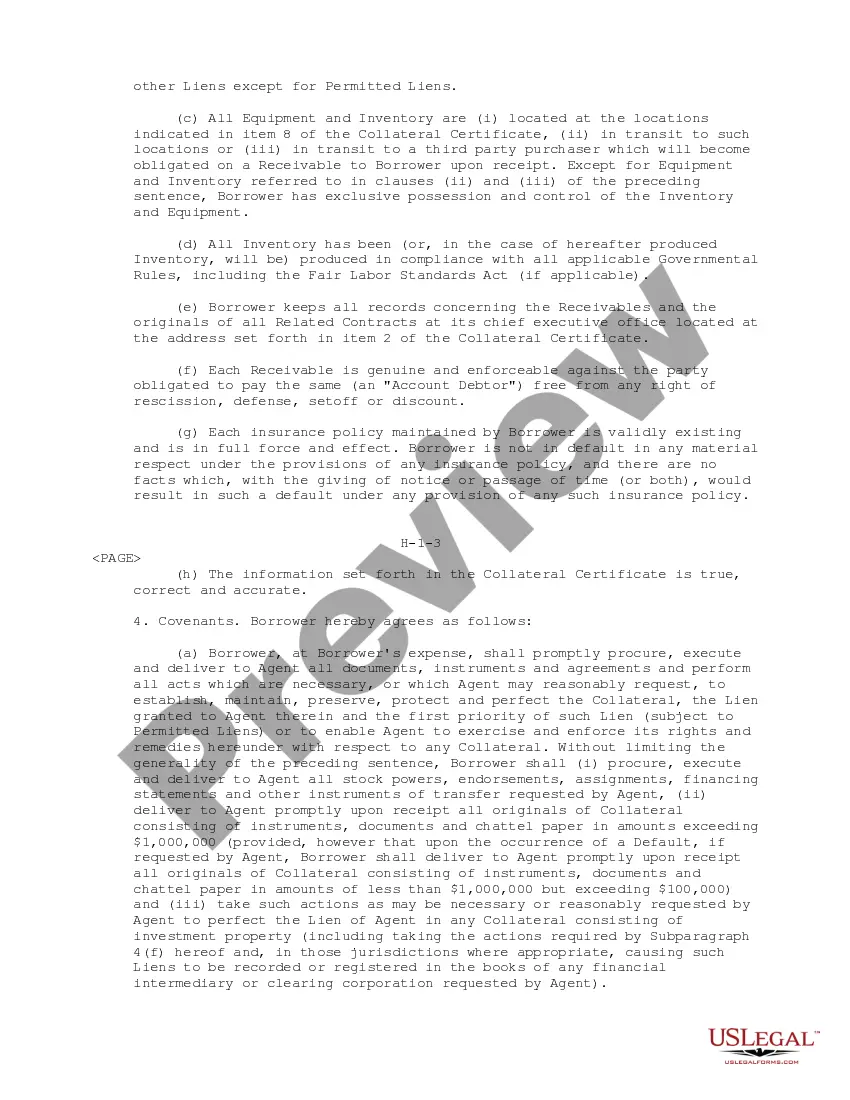

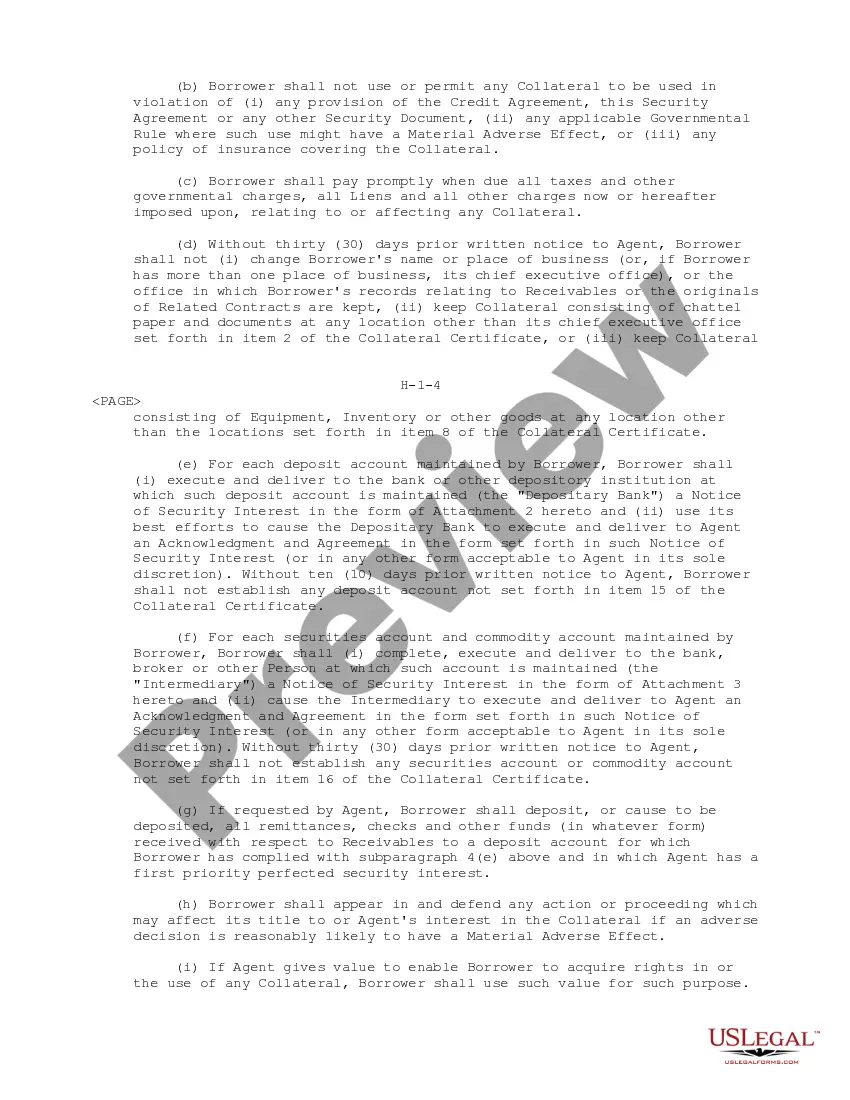

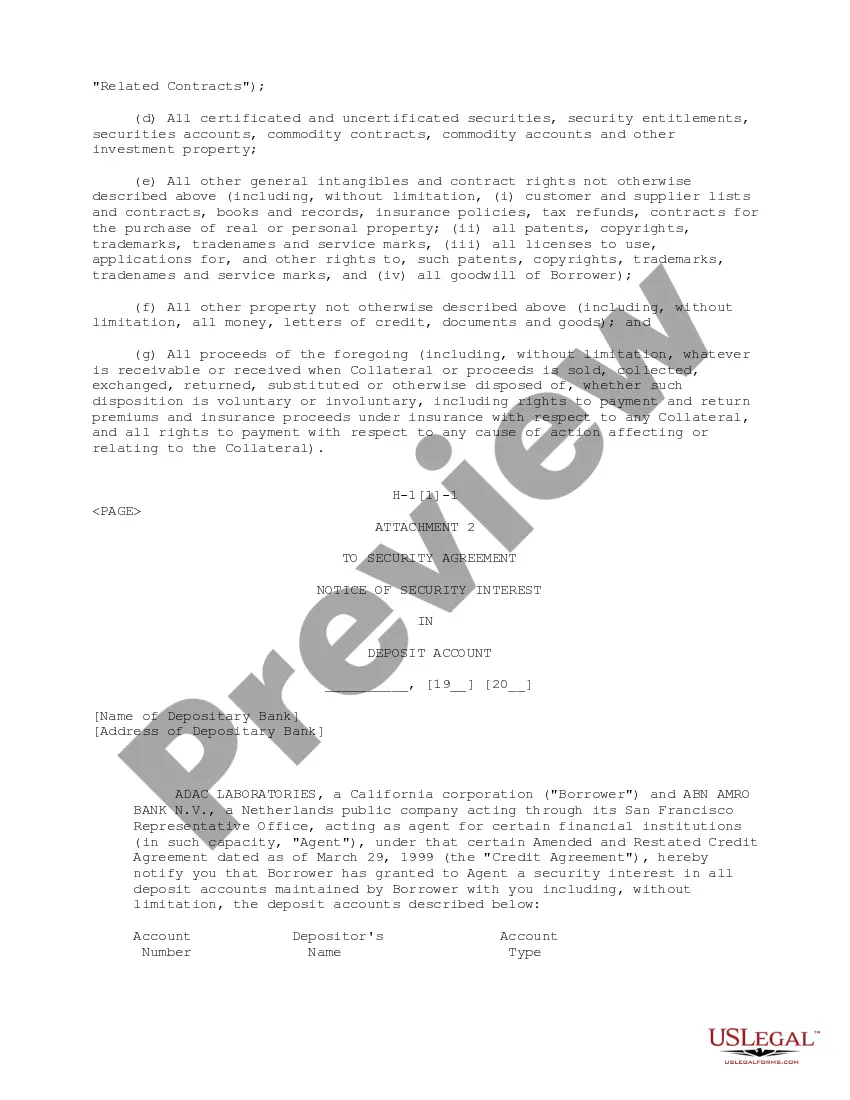

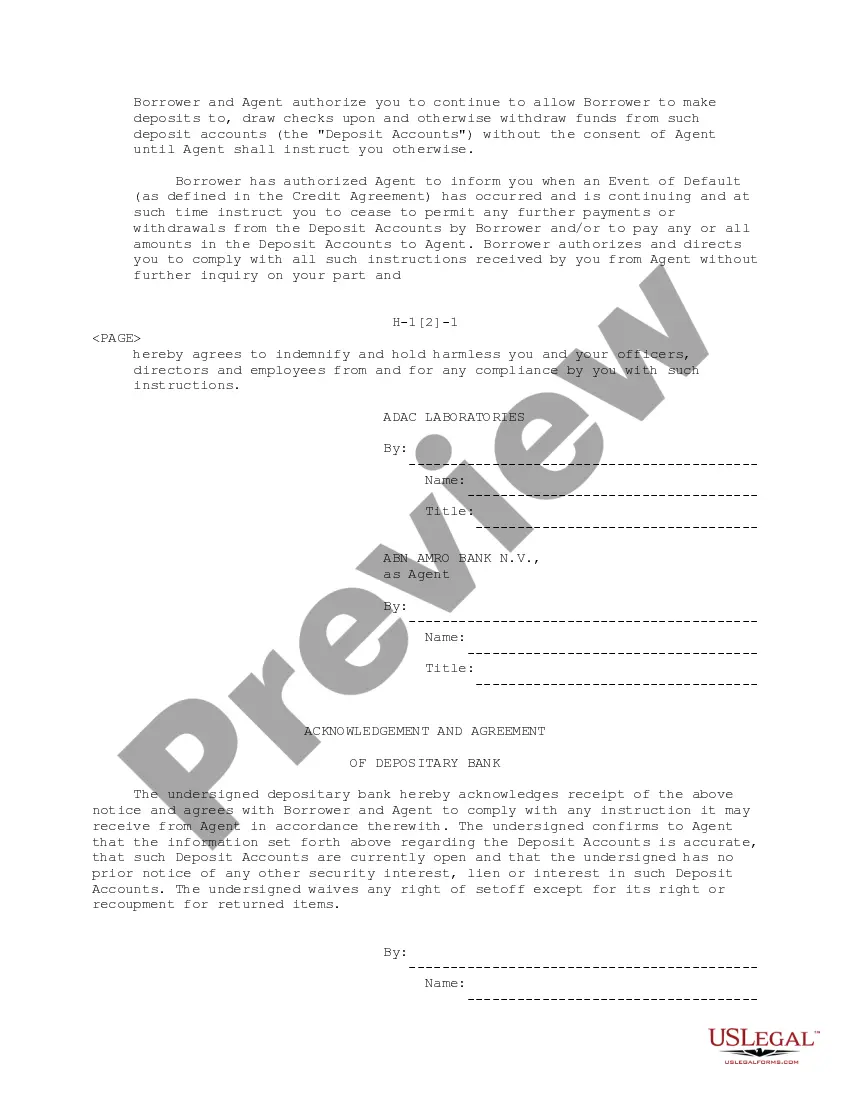

Maine Borrower Security Agreement is a legally binding contract between a borrower and a lending institution or lender regarding the extension of credit facilities. This agreement serves as collateral or security for the lender in case the borrower defaults on the loan or fails to fulfill their repayment obligations. It ensures that the lender has a legal right to seize the designated assets and properties in order to recoup the outstanding loan amount. The Maine Borrower Security Agreement consists of several key components that outline the terms and conditions of the credit extension. It begins with a comprehensive description of the borrower's obligations, including repayment schedules, interest rates, late payment penalties, and any additional fees or charges that may apply. Furthermore, this agreement specifies the types of collateral that the borrower must provide as security. These can range from tangible assets such as real estate properties, vehicles, or machinery, to intangible assets like intellectual property rights or shares in a business. The agreement must outline these assets in detail and include their current valuation or appraised worth. Additionally, the Maine Borrower Security Agreement details the rights and responsibilities of both parties involved. It clarifies the lender's authority to inspect, evaluate, and potentially sell the collateral in case of default, while also stipulating the borrower's right to cure any defaults and retain their assets through timely repayment. It is worth noting that different types of Maine Borrower Security Agreements regarding the extension of credit facilities may exist depending on the specific lending institution, borrower's circumstances, or loan purpose. Some common variations include: 1. Real Estate Mortgage: This type of security agreement is used when the loan is secured by a borrower's real property, such as a house or land. 2. UCC-1 Financing Statement: A Uniform Commercial Code (UCC) filing is used to establish a lender's security interest in a borrower's personal property, excluding real estate. It provides a public notice of the lender's claim. 3. Chattel Mortgage: This agreement is specific to loans secured by movable personal property, such as equipment, vehicles, or inventory. The borrower grants the lender a security interest in these assets. 4. Intellectual Property Security Agreement: When a borrower's intellectual property rights, such as trademarks, copyrights, or patents, serve as collateral, this type of agreement ensures the lender's security interest in these intangible assets. Remember, each lending institution might have its own unique variation or combination of these agreements. Borrowers must carefully review and understand the terms of the specific Maine Borrower Security Agreement provided by their lender before signing. Seeking legal advice is recommended to ensure full comprehension and protection of their rights and obligations throughout the credit facilities extension.

Maine Borrower Security Agreement regarding the extension of credit facilities

Description

How to fill out Maine Borrower Security Agreement Regarding The Extension Of Credit Facilities?

You may invest time on-line trying to find the legal papers web template that meets the state and federal needs you require. US Legal Forms supplies a huge number of legal varieties which can be reviewed by specialists. You can actually acquire or printing the Maine Borrower Security Agreement regarding the extension of credit facilities from my services.

If you already possess a US Legal Forms bank account, it is possible to log in and then click the Download option. After that, it is possible to complete, edit, printing, or signal the Maine Borrower Security Agreement regarding the extension of credit facilities. Every single legal papers web template you get is your own permanently. To obtain yet another duplicate associated with a obtained type, proceed to the My Forms tab and then click the corresponding option.

If you are using the US Legal Forms website the first time, keep to the straightforward guidelines beneath:

- First, be sure that you have selected the proper papers web template to the region/city of your liking. Read the type information to ensure you have chosen the appropriate type. If readily available, make use of the Review option to appear throughout the papers web template also.

- If you wish to discover yet another variation in the type, make use of the Search area to obtain the web template that suits you and needs.

- Upon having discovered the web template you would like, simply click Purchase now to move forward.

- Find the pricing plan you would like, enter your credentials, and sign up for a free account on US Legal Forms.

- Total the transaction. You should use your credit card or PayPal bank account to cover the legal type.

- Find the file format in the papers and acquire it for your product.

- Make adjustments for your papers if required. You may complete, edit and signal and printing Maine Borrower Security Agreement regarding the extension of credit facilities.

Download and printing a huge number of papers templates making use of the US Legal Forms Internet site, which offers the greatest variety of legal varieties. Use expert and status-specific templates to handle your small business or individual requires.