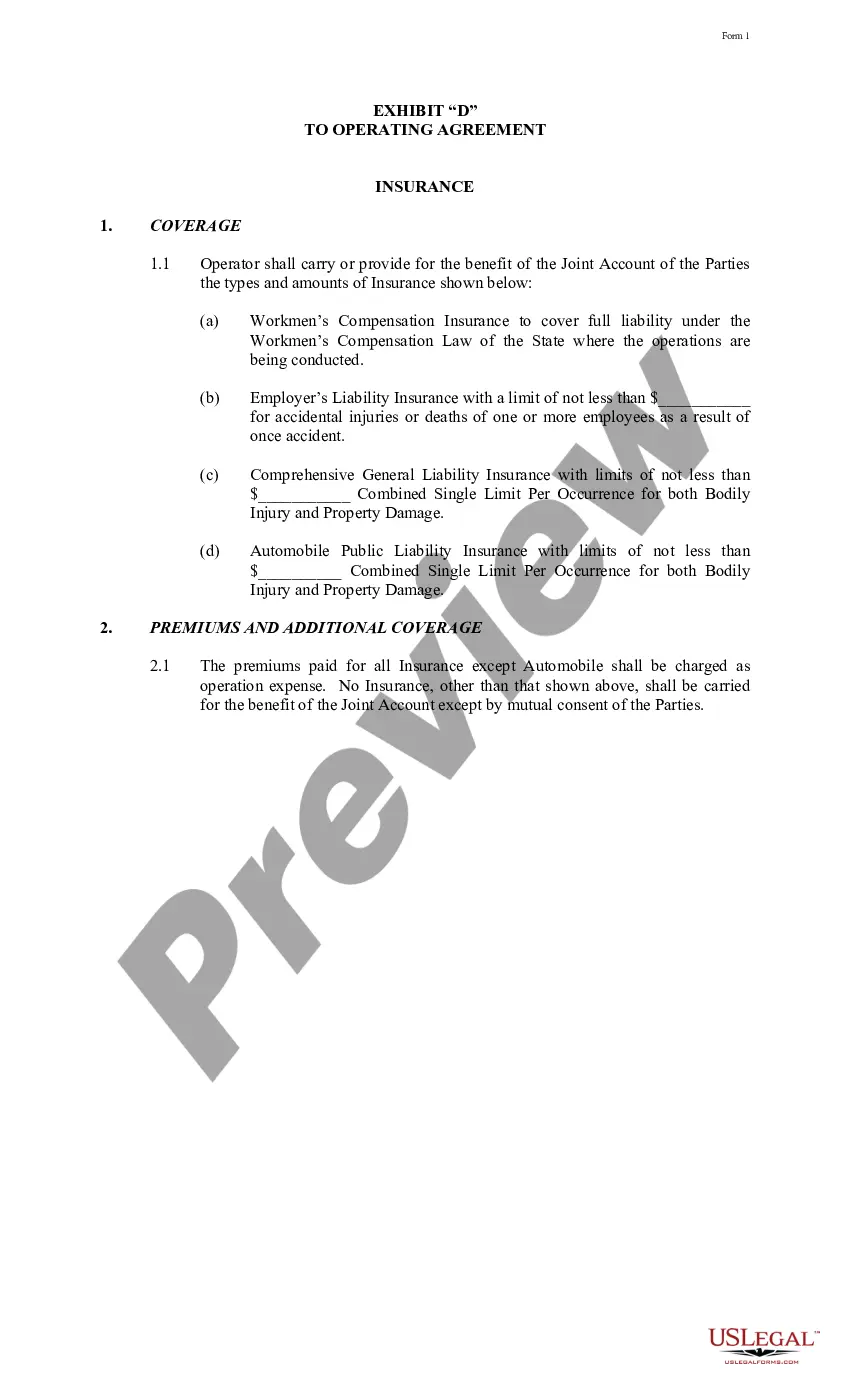

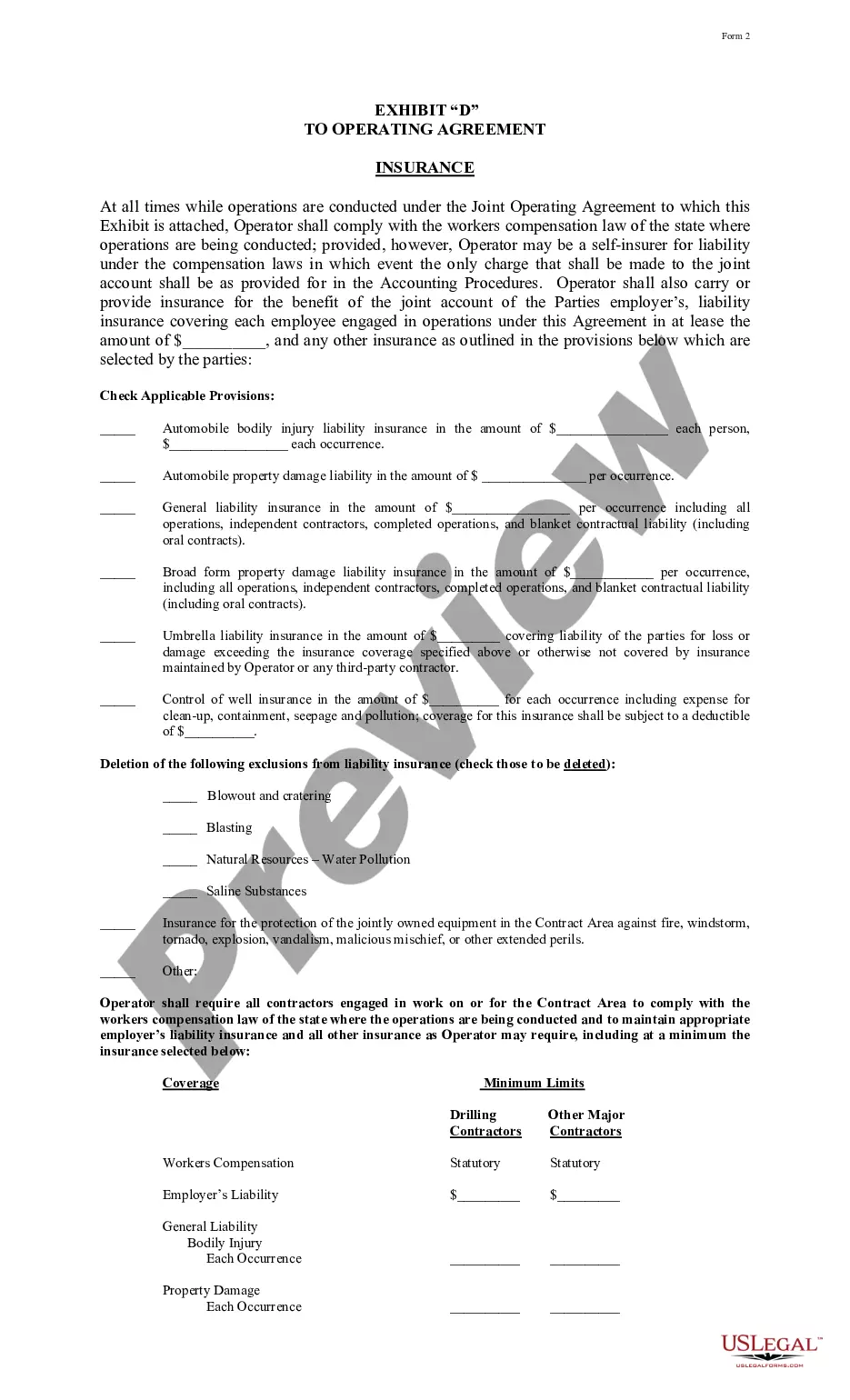

Maine Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Exhibit C Accounting Procedure Joint Operations?

You may commit hrs on-line looking for the lawful document format that suits the federal and state requirements you need. US Legal Forms offers a large number of lawful varieties which can be analyzed by specialists. It is simple to download or print out the Maine Exhibit C Accounting Procedure Joint Operations from my support.

If you already have a US Legal Forms accounts, you can log in and then click the Obtain option. Afterward, you can full, revise, print out, or indication the Maine Exhibit C Accounting Procedure Joint Operations. Every single lawful document format you get is the one you have for a long time. To get an additional backup of the purchased form, proceed to the My Forms tab and then click the related option.

If you are using the US Legal Forms site initially, stick to the simple guidelines below:

- Initially, make sure that you have chosen the best document format for the area/metropolis of your choice. Browse the form description to ensure you have picked out the proper form. If available, take advantage of the Preview option to search with the document format also.

- If you would like find an additional variation in the form, take advantage of the Research industry to obtain the format that suits you and requirements.

- After you have identified the format you would like, click on Get now to continue.

- Select the rates strategy you would like, type in your qualifications, and register for an account on US Legal Forms.

- Total the purchase. You may use your Visa or Mastercard or PayPal accounts to cover the lawful form.

- Select the format in the document and download it in your gadget.

- Make adjustments in your document if necessary. You may full, revise and indication and print out Maine Exhibit C Accounting Procedure Joint Operations.

Obtain and print out a large number of document layouts making use of the US Legal Forms web site, that provides the biggest selection of lawful varieties. Use professional and state-distinct layouts to take on your organization or personal demands.

Form popularity

FAQ

Achievements of the Committee on Accounting Procedure (CAP) comprised bulletins which provided solutions to instant issues that arose and decreased the scope of alternative practices. The Committee, however, failed to present a well-defined and systemized body of accounting principlesthat wereneeded.

The CAP decided early on that formulating a statement of broad principles would take too long and instead approached issues on a case-by-case basis. Without a framework and often without adequate research, the CAP relied on the members' collective experience for agreement on member-suggested solutions.

The Committee on Accounting Procedure (CAP) was the first private sector organization tasked with setting accounting standards in the United States. But its Accounting Research Bulletins never had binding authority.

In response to the SEC's Accounting Series Release No. 4, the American Institute of Accountants () reorganized its Committee on Accounting Procedure (CAP) in 1939 and increased it from 8 to 22 members, all accounting practitioners except for three academicians.

Committee on Accounting Procedure (CAP) 1938-1959 a. CAP was one of the committees of America Institute of Accountants (AICPA now). After the 1929 stock market crash, the government wanted to better regulate and protect the market with new accounting standards so they assigned this task to SEC.