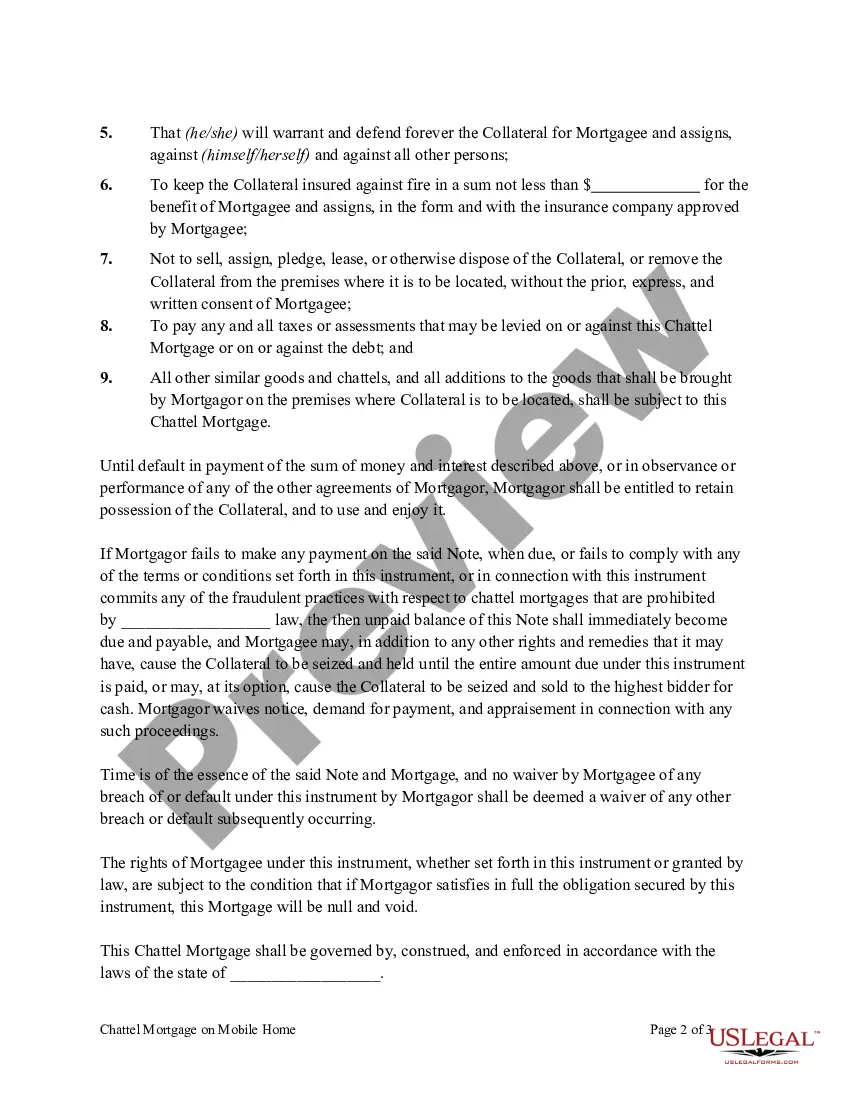

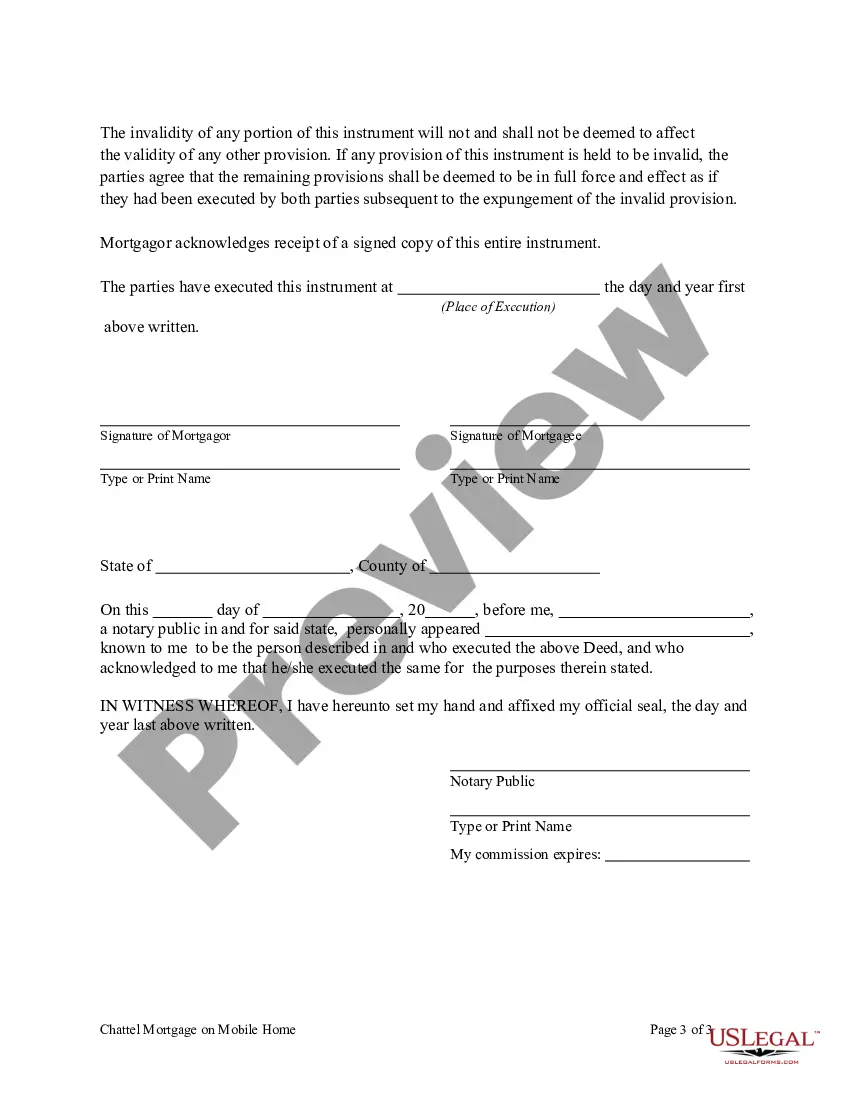

Michigan Chattel Mortgage on Mobile Home is a legal document that establishes a lien on a mobile home, allowing the lender to claim ownership if the borrower fails to repay the loan. Chattel mortgages are commonly used in Michigan to secure financing for the purchase of mobile homes. In Michigan, there are two main types of chattel mortgages on mobile homes: purchase money chattel mortgages and non-purchase money chattel mortgages. 1. Purchase Money Chattel Mortgage: This type of chattel mortgage is used when the mobile home is purchased with the loan proceeds. The lender holds a lien on the mobile home as collateral until the borrower repays the loan in full. Once the loan is fully paid, the lien is released, and the borrower becomes the sole owner of the mobile home. 2. Non-Purchase Money Chattel Mortgage: Unlike the purchase money chattel mortgage, this type of mortgage is used when the mobile home was not purchased with the loan proceeds. For example, if the borrower already owns a mobile home outright but needs financing for other purposes, they can use a non-purchase money chattel mortgage to secure the loan. The lender still holds a lien on the mobile home until the borrower repays the loan, similar to a purchase money chattel mortgage. It is crucial for both lenders and borrowers to understand the terms and conditions of the Michigan Chattel Mortgage on Mobile Home. The document should clearly state the loan amount, interest rate, repayment schedule, and any additional fees or charges. Lenders may require a down payment or minimum credit score to qualify for a chattel mortgage. Additionally, it is important to note that mobile homes, unlike traditional houses, are considered personal property as they can be moved. Chattel mortgages are specifically designed for these types of homes, providing a legal framework for financing and ownership rights. To ensure a smooth transaction, it is advisable for both parties to consult with a knowledgeable attorney or a trusted real estate professional who is familiar with Michigan laws regarding chattel mortgages on mobile homes. By adhering to the legal requirements and understanding the implications of this mortgage instrument, borrowers can secure financing for their mobile home while lenders protect their investment.

Michigan Chattel Mortgage on Mobile Home

Description

How to fill out Michigan Chattel Mortgage On Mobile Home?

Finding the right legal papers web template could be a struggle. Of course, there are plenty of themes available on the Internet, but how do you discover the legal form you want? Take advantage of the US Legal Forms web site. The support gives 1000s of themes, for example the Michigan Chattel Mortgage on Mobile Home, which you can use for company and personal requires. Each of the varieties are checked out by experts and meet state and federal demands.

Should you be previously authorized, log in to your accounts and click the Acquire option to have the Michigan Chattel Mortgage on Mobile Home. Make use of accounts to look with the legal varieties you possess purchased formerly. Visit the My Forms tab of the accounts and get yet another copy from the papers you want.

Should you be a fresh end user of US Legal Forms, listed below are easy directions for you to adhere to:

- Very first, be sure you have selected the correct form to your metropolis/region. You may look over the form utilizing the Review option and study the form explanation to guarantee it is the best for you.

- In the event the form fails to meet your expectations, make use of the Seach area to find the right form.

- When you are certain that the form is acceptable, select the Acquire now option to have the form.

- Pick the rates strategy you desire and enter in the necessary info. Make your accounts and purchase the order making use of your PayPal accounts or credit card.

- Choose the document file format and down load the legal papers web template to your device.

- Full, change and print out and sign the acquired Michigan Chattel Mortgage on Mobile Home.

US Legal Forms may be the most significant collection of legal varieties for which you can find a variety of papers themes. Take advantage of the company to down load skillfully-made documents that adhere to status demands.

Form popularity

FAQ

Prepare to meet these requirements to qualify for a chattel mortgage: Credit score: You'll need an excellent credit score (around 680 or higher) to qualify for this type of loan.

A chattel mortgage is a loan for a manufactured home or other movable piece of personal property, such as machinery or a vehicle. The movable property, called ?chattel,? also acts as collateral for the loan.

Chattel is any tangible personal property that is movable. Examples of chattel are furniture, livestock, bedding, picture frames, and jewelry.

A chattel mortgage is used to purchase movable personal property, other than real estate, which serves as collateral for the loan until it's repaid. Farm equipment, livestock, farm assets, and mobile and manufactured homes are a few examples of property you could purchase with a chattel loan.

Best Mobile Home Loans Reviews Best for Rural Areas: USDA. ... Best for a Variety of Loan Options: Vanderbilt Mortgage and Finance. ... Best for Low Credit Scores: Manufactured Nationwide. ... Best for Good Credit Scores: ManufacturedHome. ... Best for Mobile Homes Within a Community or Park: 21st Mortgage Corporation.

Mortgage for Mobile Homes in Michigan There are programs available for Double Wide Mobile Homes or even single wide mobile homes if you are on some acreage.