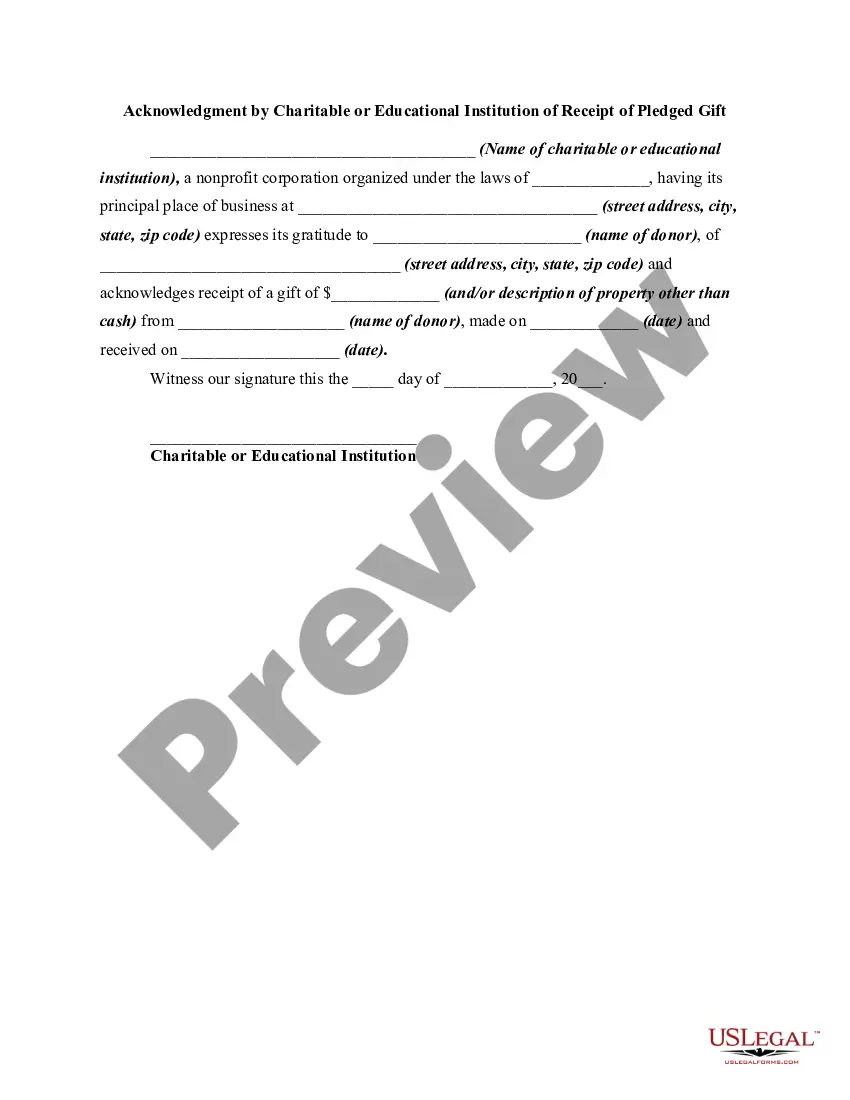

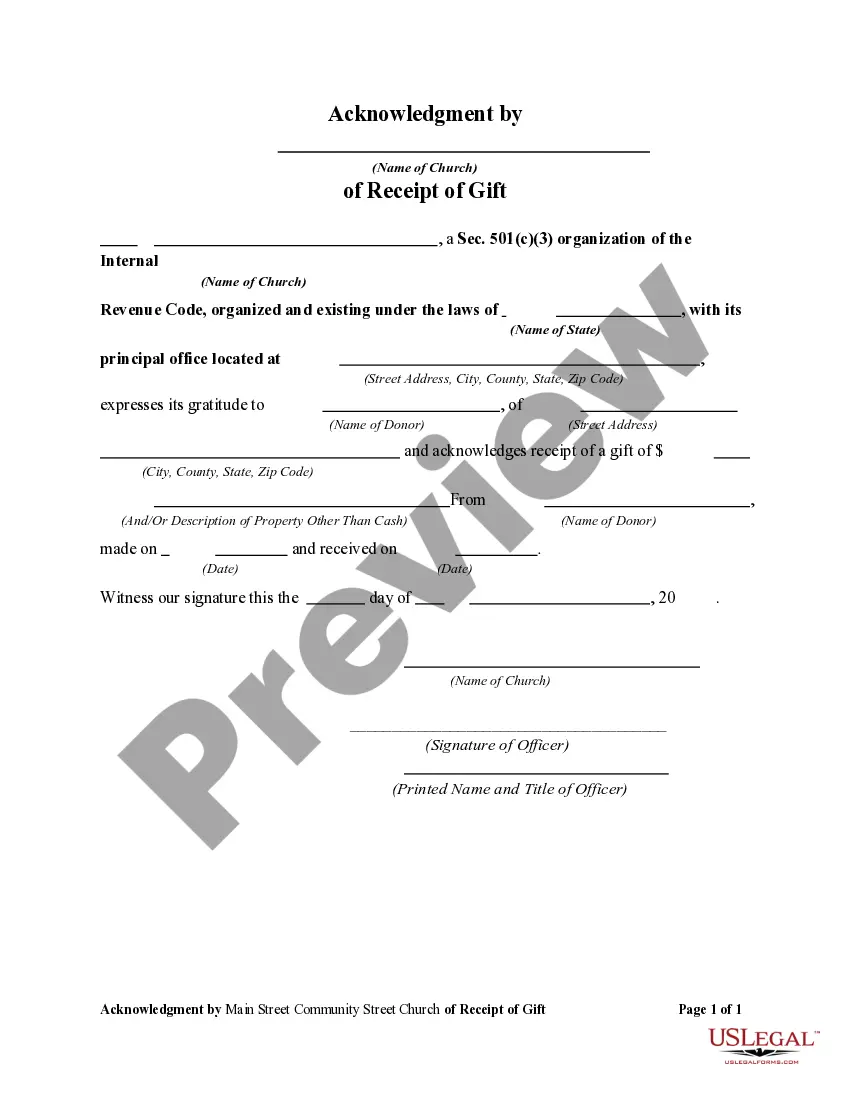

Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

US Legal Forms - one of the largest repositories of legal documents in the United States - offers a range of legal document templates for you to download or print. By utilizing the site, you can discover thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of forms like the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift in moments.

If you already have a monthly subscription, Log In and download the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift from the US Legal Forms library. The Download button will appear on each form you view. You can access all previously downloaded forms in the My documents section of your account.

If you are using US Legal Forms for the first time, here are simple instructions to help you begin: Ensure you have selected the correct form for your city/county. Click on the Preview button to check the form's content. Review the form description to confirm that you have chosen the correct form. If the form does not meet your requirements, use the Search box at the top of the page to find one that does. If you are satisfied with the form, confirm your choice by clicking on the Get now button. Then, select the subscription plan you prefer and provide your information to sign up for an account. Process the transaction. Use your credit card or PayPal account to complete the purchase. Choose the file format and download the form to your device. Make edits. Complete, modify, print, and sign the downloaded Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Every template you added to your account has no expiration date and is yours indefinitely. Therefore, to download or print another copy, simply go to the My documents section and click on the form you desire.

- Access the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift with US Legal Forms, the most comprehensive collection of legal document templates.

- Utilize thousands of professional and state-specific templates that cater to your business or personal requirements and preferences.

Form popularity

FAQ

A written acknowledgment for a charitable contribution typically includes specific details about the donation. For example, it may state, 'Thank you for your generous contribution of $500 to Organization Name. This gift supports our mission to briefly describe mission. No goods or services were provided in exchange for this donation.' Using the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift helps ensure clarity and professionalism in your communication.

Acknowledging receipt of a donation involves providing a written statement to the donor. This acknowledgment should include the name of the charitable organization, the amount of the donation, and a statement indicating whether any goods or services were provided in exchange. Utilizing the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift can simplify this process, ensuring compliance with IRS requirements and enhancing donor relations.

In Michigan, a notary acknowledgment must include certain elements to be valid. First, it needs to be signed by the individual in front of the notary. Additionally, the notary must complete a certificate that includes their signature, seal, and the date of the acknowledgment. For organizations, the Michigan Acknowledgment by Charitable or Educational Institution of Receipt of Gift should also confirm the entity's capacity to receive donations.

This deduction is not added back to reach Michigan taxable income. For tax year 2021 a $300 (single) or $600 (joint) charitable contribution deduction is not deducted to arrive at adjusted gross income (AGI), but is instead deducted to arrive at federal taxable income.

(1) ?Gift? means a payment, advance, forbearance, or the rendering or deposit of money, services, or anything of value, the value of which exceeds $25.00, as adjusted under section 19a, in any 1-month period, unless consideration of equal or greater value is received therefor.

The gift makes up a large percentage of your income. Your deduction for charitable contributions is generally limited to 60% of your AGI. For tax years 2020 and 2021, you can deduct cash contributions in full up to 100% of your AGI to qualified charities. There are limits for non-cash contributions.

A written gift acceptance policy can help manage the expectations of donors (while treating them with respect) and also serve as guidance for board and staff members who are on either the asking or receiving end of contributions.

Our federal tax ID number is 38-6006309. Your gift may provide you with federal and state income tax benefits: If you itemize deductions on your federal income tax return, you may be able to deduct your contribution to U-M from your adjusted gross income.

Charitable donations to universities are tax-deductible, meaning that donors can claim a deduction on their federal income tax returns for the full value of the donation. This can result in significant tax savings for donors, especially those who make large donations.

The University of Michigan has 501(c)(3) non-profit tax exempt status; our federal tax ID number is 38-6006309.