Michigan Partial Assignment of Life Insurance Policy as Collateral is a financial agreement that allows individuals to use a portion of their life insurance policy as collateral for a loan or other financial obligation. This type of arrangement provides a way for policyholders to access the cash value of their life insurance policy without surrendering it entirely. In a Michigan Partial Assignment of Life Insurance Policy as Collateral, the policyholder assigns a specific amount of the death benefit or cash value of their policy to the lender as collateral for the loan. The assigned portion is determined based on the loan amount or the agreed-upon collateral value. This assignment helps to secure the lender's interest in case of default or inability to repay the loan. There are different types of Michigan Partial Assignment of Life Insurance Policy as Collateral: 1. Percentage-based Assignment: In this type, the policyholder assigns a fixed percentage of the death benefit or cash value as collateral. For example, if the policy has a cash value of $100,000 and the policyholder assigns 50%, then $50,000 becomes the collateral. 2. Fixed Amount Assignment: Here, the policyholder assigns a specific dollar amount of the death benefit or cash value as collateral. For instance, if the policy has a cash value of $100,000 and the policyholder assigns $25,000, then $25,000 becomes the collateral. 3. Loan-to-Value (LTV) Assignment: This type of assignment calculates the collateral value based on the loan amount. The insurance policy's cash value or death benefit assigned as collateral depends on the lender's specified loan-to-value ratio. For example, if the lender approves a loan with an LTV ratio of 80%, and the policy's cash value is $100,000, then $80,000 would be the collateral. Michigan Partial Assignment of Life Insurance Policy as Collateral offers policyholders flexibility by allowing them to retain ownership of their policy while still leveraging its value to meet their financial needs. It is essential to carefully review the terms and conditions of the assignment agreement before entering into such arrangements to ensure full understanding of the obligations and consequences. Consulting with a financial advisor or insurance professional in Michigan is advised to navigate this process effectively.

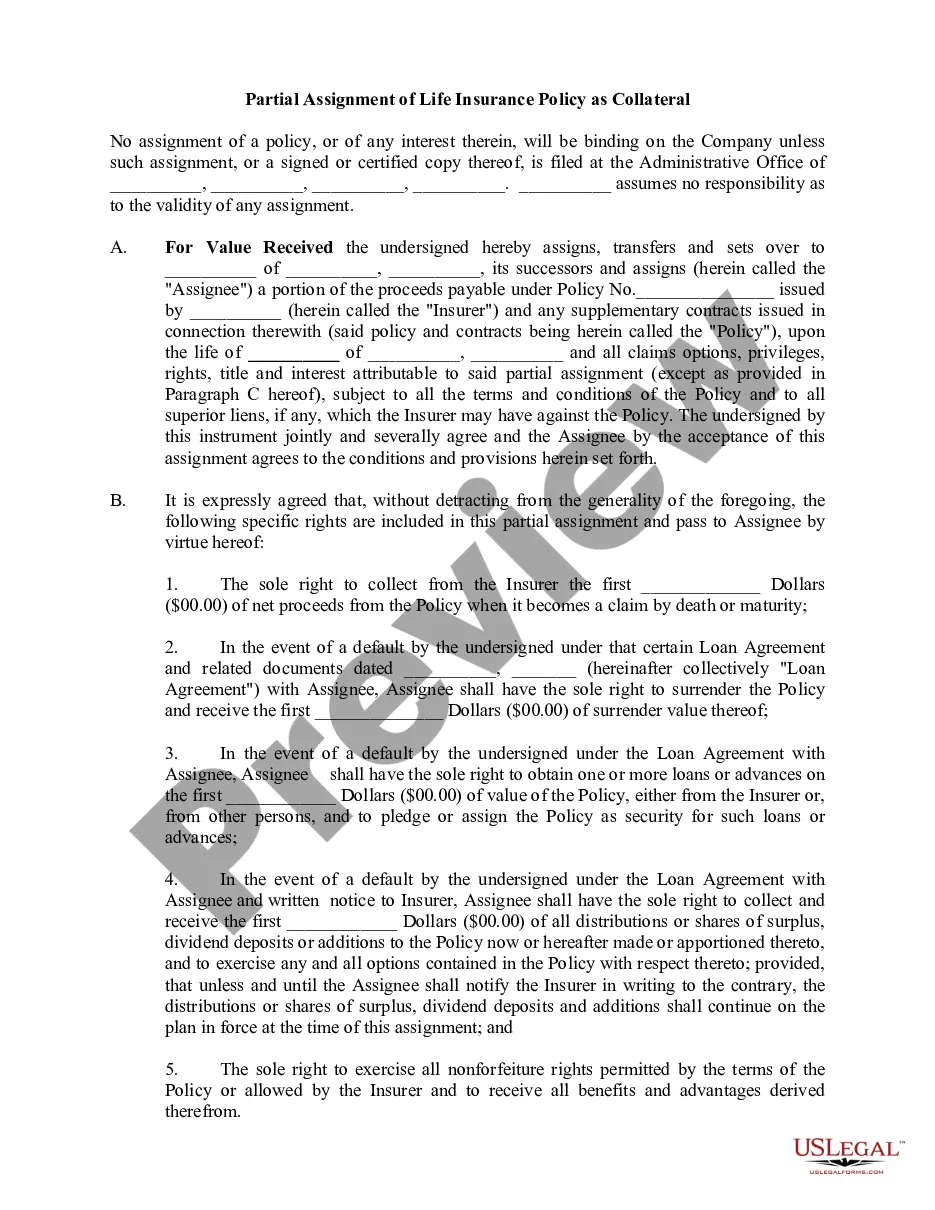

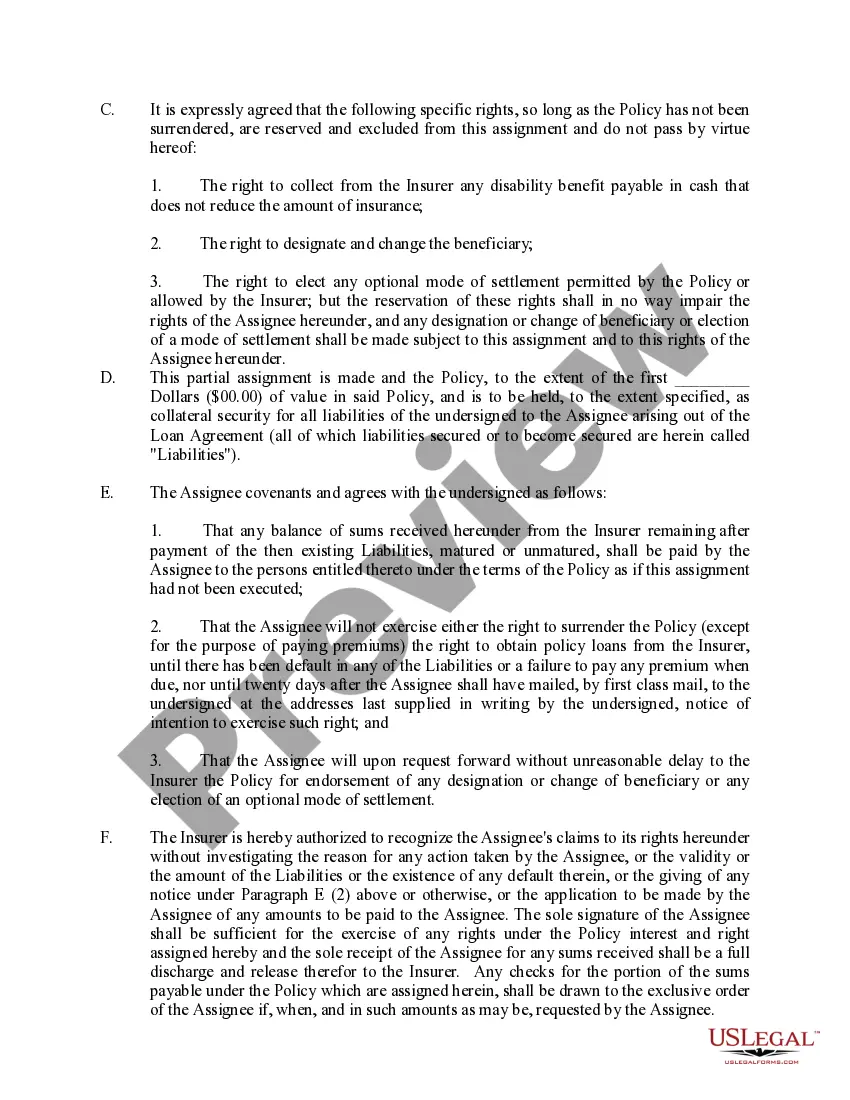

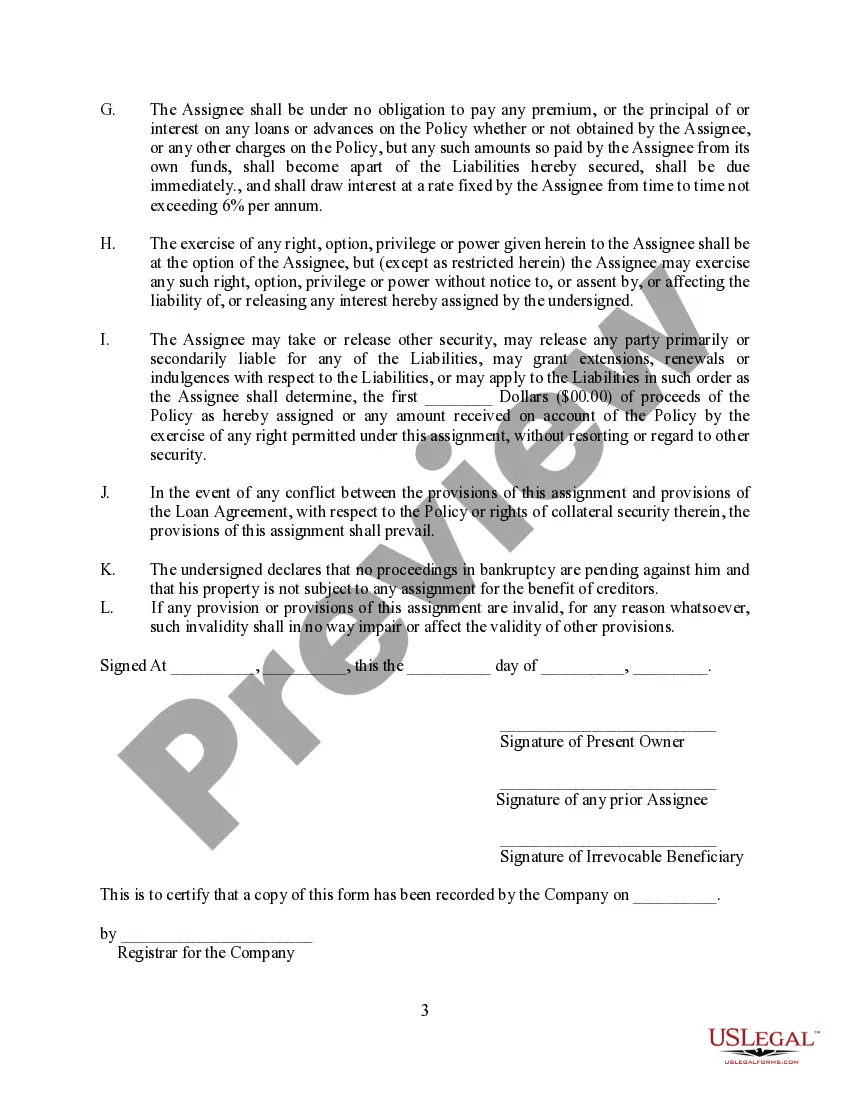

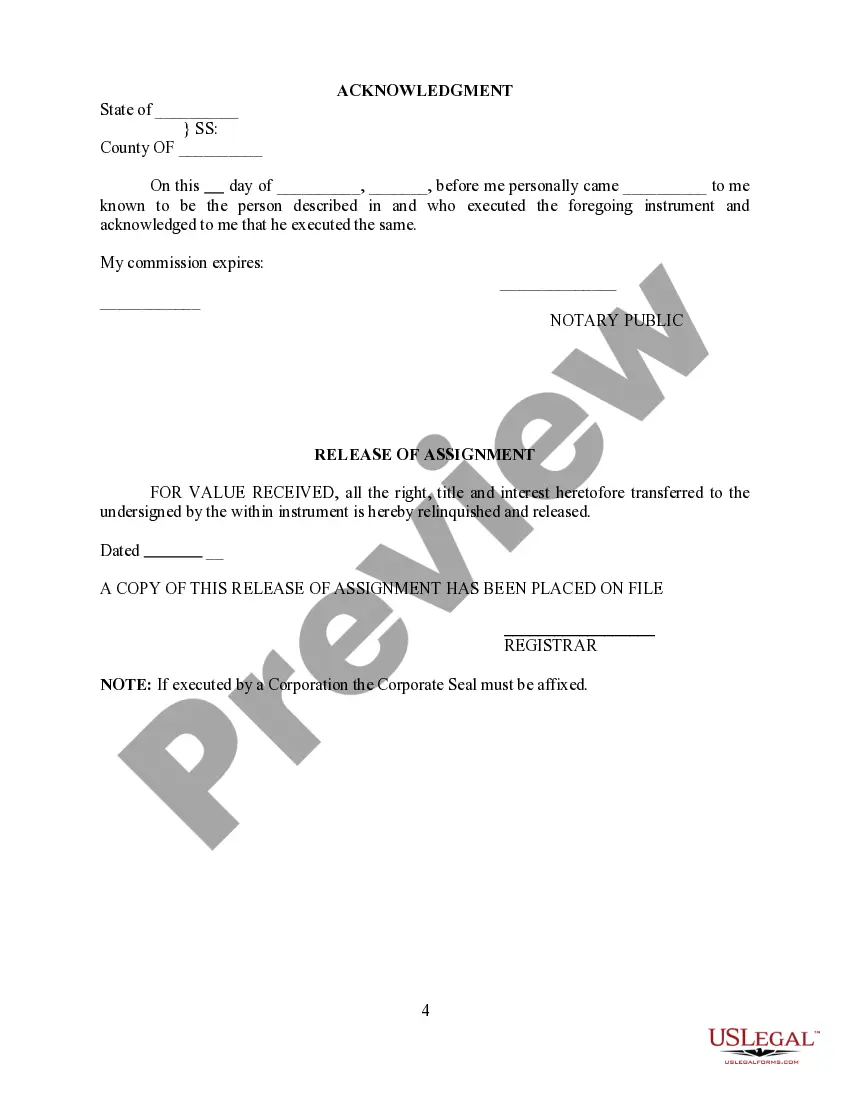

Michigan Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Michigan Partial Assignment Of Life Insurance Policy As Collateral?

US Legal Forms - one of several most significant libraries of authorized forms in the USA - delivers a wide array of authorized record layouts it is possible to acquire or print out. While using web site, you can get 1000s of forms for organization and personal purposes, sorted by categories, states, or keywords and phrases.You will find the most up-to-date variations of forms such as the Michigan Partial Assignment of Life Insurance Policy as Collateral in seconds.

If you have a subscription, log in and acquire Michigan Partial Assignment of Life Insurance Policy as Collateral from your US Legal Forms local library. The Down load option can look on each and every develop you look at. You gain access to all earlier downloaded forms from the My Forms tab of your respective bank account.

If you wish to use US Legal Forms for the first time, listed below are straightforward recommendations to get you started off:

- Be sure you have picked the correct develop for your personal city/area. Click the Preview option to analyze the form`s content. See the develop outline to actually have selected the appropriate develop.

- In case the develop doesn`t match your needs, take advantage of the Research area at the top of the screen to obtain the one that does.

- In case you are content with the form, confirm your option by clicking the Get now option. Then, select the pricing prepare you favor and supply your qualifications to sign up to have an bank account.

- Method the transaction. Utilize your Visa or Mastercard or PayPal bank account to finish the transaction.

- Select the format and acquire the form on your gadget.

- Make modifications. Complete, revise and print out and sign the downloaded Michigan Partial Assignment of Life Insurance Policy as Collateral.

Each template you added to your account lacks an expiry time which is your own property for a long time. So, if you wish to acquire or print out yet another copy, just go to the My Forms area and click on around the develop you require.

Obtain access to the Michigan Partial Assignment of Life Insurance Policy as Collateral with US Legal Forms, the most comprehensive local library of authorized record layouts. Use 1000s of specialist and state-particular layouts that meet your organization or personal requires and needs.

Form popularity

FAQ

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

With an absolute assignment, the entire ownership of the policy would be transferred to the assignee, or the lender. Then, the lender would be entitled to the full death benefit. With a collateral assignment, the lender is only entitled to the balance of the outstanding loan.

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

?Collateral assignment of life insurance is typically associated with business loans and mortgages,? says Martinez. If you're launching a small business and applying for a loan to help you get started, the bank might request that you include your life insurance policy as collateral.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment.