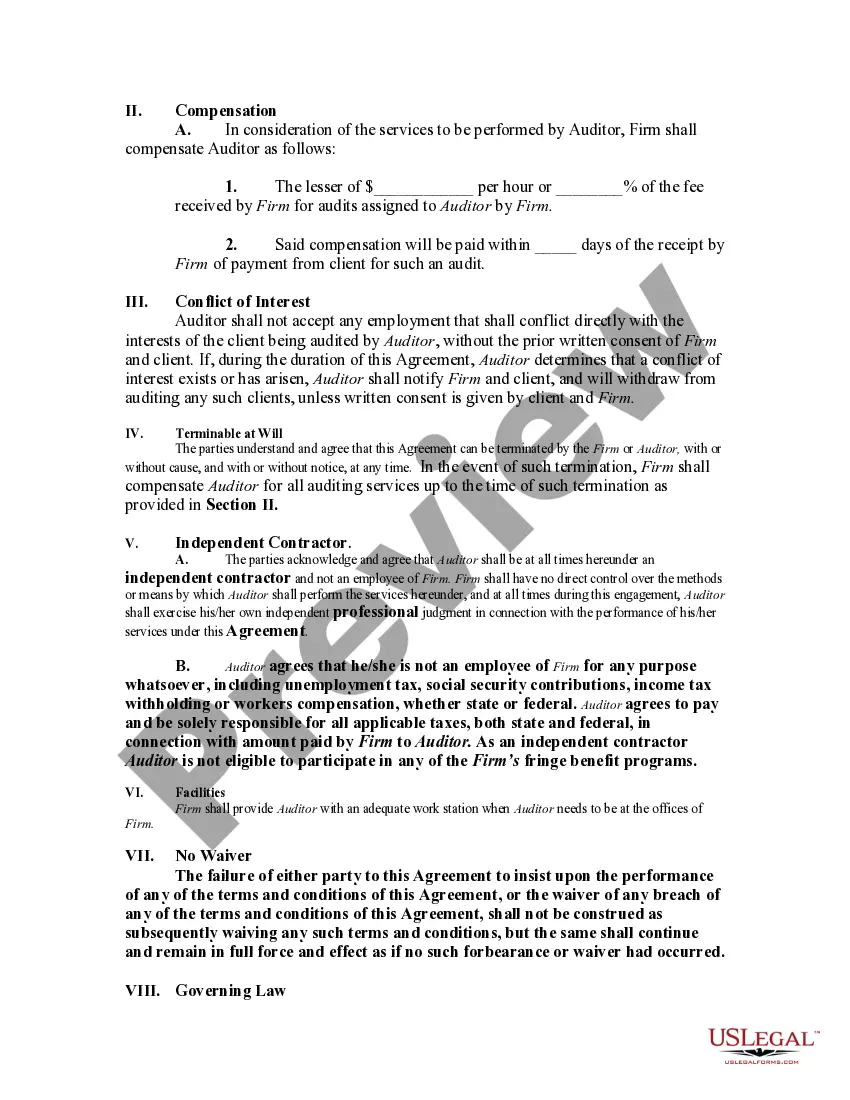

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

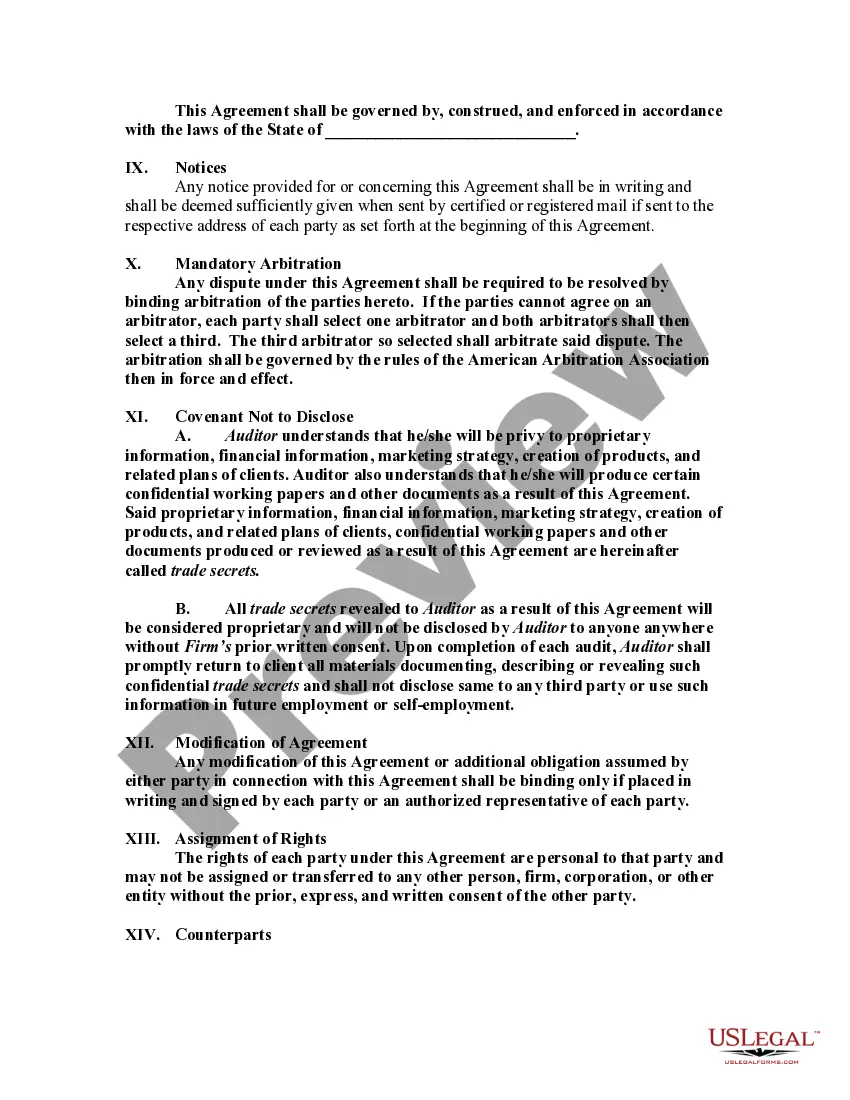

Title: Michigan Agreement by an Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor Introduction: In the world of accounting and auditing, it is crucial for accounting firms to establish clear and legally binding agreements when engaging auditors as self-employed independent contractors. This article aims to provide a detailed description of the Michigan Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor, explaining its purpose, key elements, and variations that may exist. 1. Purpose of the Michigan Agreement: The Michigan Agreement serves as a formal contract between an accounting firm and an auditor, outlining the terms and conditions of their professional relationship. The main objective of this agreement is to establish the auditor's status as a self-employed independent contractor rather than an employee, ensuring legal compliance and clarifying both parties' rights and obligations. 2. Key Elements of the Agreement: a) Contractor Status: The agreement specifies that the auditor will be engaged as an independent contractor, clearly differentiating their role from that of an employee. b) Scope of Services: It defines the specific auditing services to be performed by the contractor, including the nature, extent, and timeframes for completion. c) Compensation: The agreement outlines the payment terms, including the rate, method of payment, and any additional expenses or reimbursements. d) Confidentiality and Non-Disclosure: This section ensures that the auditor maintains the confidentiality of sensitive client information and refrains from disclosing it to third parties. e) Dispute Resolution: It establishes a mechanism for resolving any conflicts or disputes that may arise during the course of the engagement. f) Termination Clause: This clause defines the conditions under which either party can terminate the agreement, such as breach of contract or non-performance. 3. Variations of the Agreement: a) Michigan Agreement with Non-Compete Clause: Some accounting firms may choose to include a non-compete clause, which restricts the auditor from accepting similar engagements with competing firms for a specified period after termination. b) Michigan Agreement with Non-Solicitation Clause: This variant prevents the auditor from soliciting or accepting business from the firm's clients for a specific duration following the termination of the agreement. c) Michigan Agreement with Intellectual Property Clause: In cases where the auditor may create or contribute to intellectual property during the engagement, this clause ensures that the accounting firm retains ownership rights to such assets. Conclusion: The Michigan Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor is an essential legal document that safeguards the interests of both parties involved. By clearly defining the rights, responsibilities, and expectations, this agreement establishes a strong foundation for a mutually beneficial professional relationship within the accounting industry.Title: Michigan Agreement by an Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor Introduction: In the world of accounting and auditing, it is crucial for accounting firms to establish clear and legally binding agreements when engaging auditors as self-employed independent contractors. This article aims to provide a detailed description of the Michigan Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor, explaining its purpose, key elements, and variations that may exist. 1. Purpose of the Michigan Agreement: The Michigan Agreement serves as a formal contract between an accounting firm and an auditor, outlining the terms and conditions of their professional relationship. The main objective of this agreement is to establish the auditor's status as a self-employed independent contractor rather than an employee, ensuring legal compliance and clarifying both parties' rights and obligations. 2. Key Elements of the Agreement: a) Contractor Status: The agreement specifies that the auditor will be engaged as an independent contractor, clearly differentiating their role from that of an employee. b) Scope of Services: It defines the specific auditing services to be performed by the contractor, including the nature, extent, and timeframes for completion. c) Compensation: The agreement outlines the payment terms, including the rate, method of payment, and any additional expenses or reimbursements. d) Confidentiality and Non-Disclosure: This section ensures that the auditor maintains the confidentiality of sensitive client information and refrains from disclosing it to third parties. e) Dispute Resolution: It establishes a mechanism for resolving any conflicts or disputes that may arise during the course of the engagement. f) Termination Clause: This clause defines the conditions under which either party can terminate the agreement, such as breach of contract or non-performance. 3. Variations of the Agreement: a) Michigan Agreement with Non-Compete Clause: Some accounting firms may choose to include a non-compete clause, which restricts the auditor from accepting similar engagements with competing firms for a specified period after termination. b) Michigan Agreement with Non-Solicitation Clause: This variant prevents the auditor from soliciting or accepting business from the firm's clients for a specific duration following the termination of the agreement. c) Michigan Agreement with Intellectual Property Clause: In cases where the auditor may create or contribute to intellectual property during the engagement, this clause ensures that the accounting firm retains ownership rights to such assets. Conclusion: The Michigan Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor is an essential legal document that safeguards the interests of both parties involved. By clearly defining the rights, responsibilities, and expectations, this agreement establishes a strong foundation for a mutually beneficial professional relationship within the accounting industry.