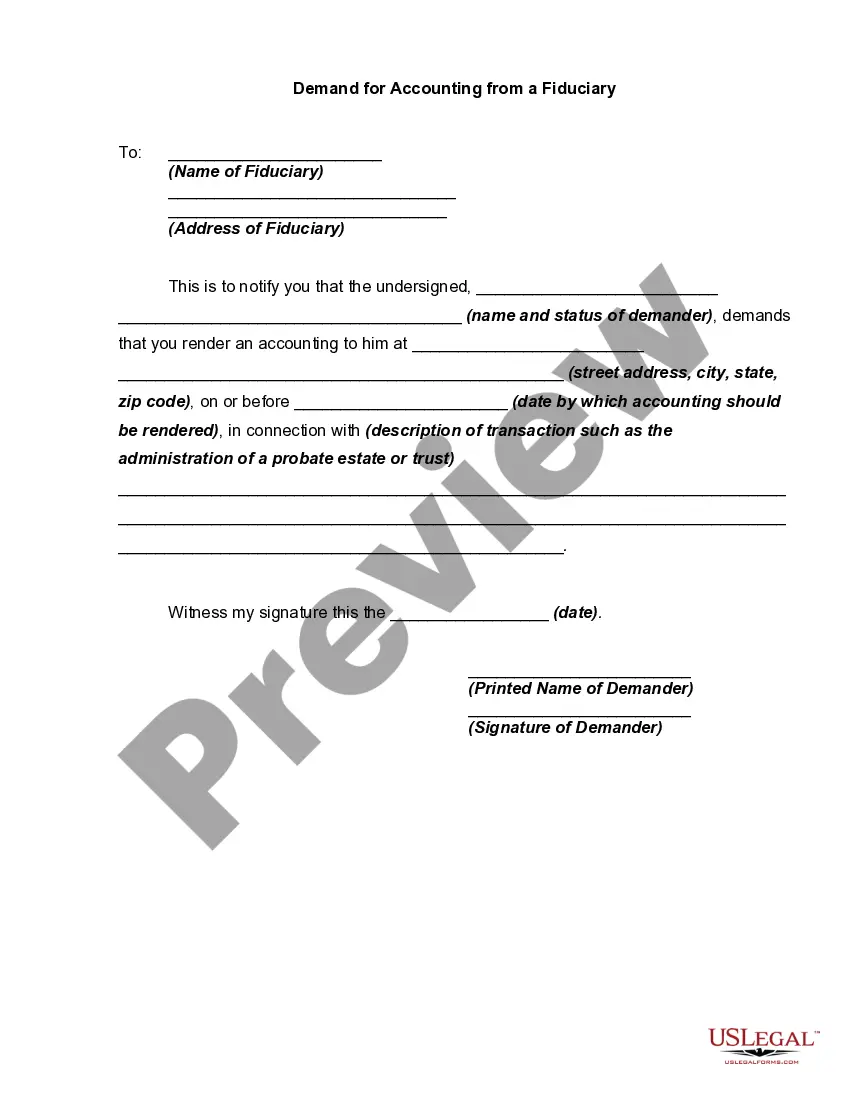

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary Such As An Executor, Conservator, Trustee Or Legal Guardian?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a vast array of legal template documents that you can download or print.

By utilizing the site, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can find the latest versions of forms like the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian in moments.

Read the form description to ensure you have selected the correct form.

If the form does not meet your needs, use the Search field at the top of the screen to find the one that does.

- If you possess a subscription, Log In to download the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian from the US Legal Forms library.

- The Download button will appear on every form you view.

- You can access all previously downloaded forms within the My documents section of your profile.

- To use US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the appropriate form for your city/region.

- Click the Review button to examine the content of the form.

Form popularity

FAQ

Conservatorship can sometimes lead to a loss of autonomy for the individual, as decisions may be taken out of their hands. Additionally, the process can become expensive, with court fees and management costs accumulating over time. Recognizing these challenges is important when dealing with the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian, as it emphasizes the need for careful planning.

In Michigan, a guardian cannot make certain decisions without court approval, such as altering the ward's legal status or refusing medical treatment that could save their life. Additionally, guardians must respect the wishes of the individual, as much as their abilities allow. Being informed about limits is crucial, especially when addressing the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

Yes, in Michigan, it is possible for one person to serve as both a guardian and a conservator. This dual role can simplify decision-making and provide unified support for the individual. However, careful consideration is necessary, especially regarding the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian, to ensure proper oversight.

A conservator in Michigan possesses the authority to handle financial matters for the individual under their care. This includes managing assets, paying bills, and making investment decisions. The role requires accountability, especially in the context of the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian, ensuring that all transactions are transparent.

In Michigan, a conservatorship is established to manage a person's financial affairs, while a guardianship focuses on making personal and medical decisions. The key distinction lies in the scope of control; a conservator handles assets and income, whereas a guardian oversees well-being and care. Understanding these roles is vital, especially when navigating the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

A fiduciary conservator is an individual or entity appointed to manage the financial affairs of a person deemed incapacitated. This role involves not only safeguarding assets but also making decisions that align with the best interests of the individual. If you are navigating this territory, a Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian can clarify responsibilities and ensure compliance with legal standards.

In Michigan, a guardian is responsible for making personal and healthcare decisions for an individual, often a minor or someone incapacitated. Conversely, a conservator manages the financial matters of an individual. Understanding these roles is vital when establishing a Michigan Demand for Accounting from a Fiduciary such as an Executor or Conservator, as each has specific duties and accountabilities.

Yes, in Michigan, an executor is required to provide an accounting to beneficiaries. This accounting should detail all income, expenses, and distributions related to the estate. Transparency is essential, ensuring beneficiaries understand how the estate assets were handled. If you have concerns about this process, consider a Michigan Demand for Accounting from a Fiduciary such as an Executor.

A Conservator fiduciary is a person appointed by the court to manage the financial affairs of an individual deemed unable to do so themselves. The conservator has a legal duty to act in the best interest of the individual, ensuring their assets are protected and managed appropriately. This role is crucial in cases involving minors or disabled adults. If you need assistance understanding these roles further, US Legal Forms can provide clarity in relation to Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

To pursue guardianship in Michigan, you will typically need specific forms, including a petition for guardianship and a notice of hearing. These forms require details about the proposed ward and the reason for guardianship. Additionally, you may need to submit medical evaluations or other relevant documentation. Utilizing US Legal Forms can help streamline your application process for the Michigan Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.