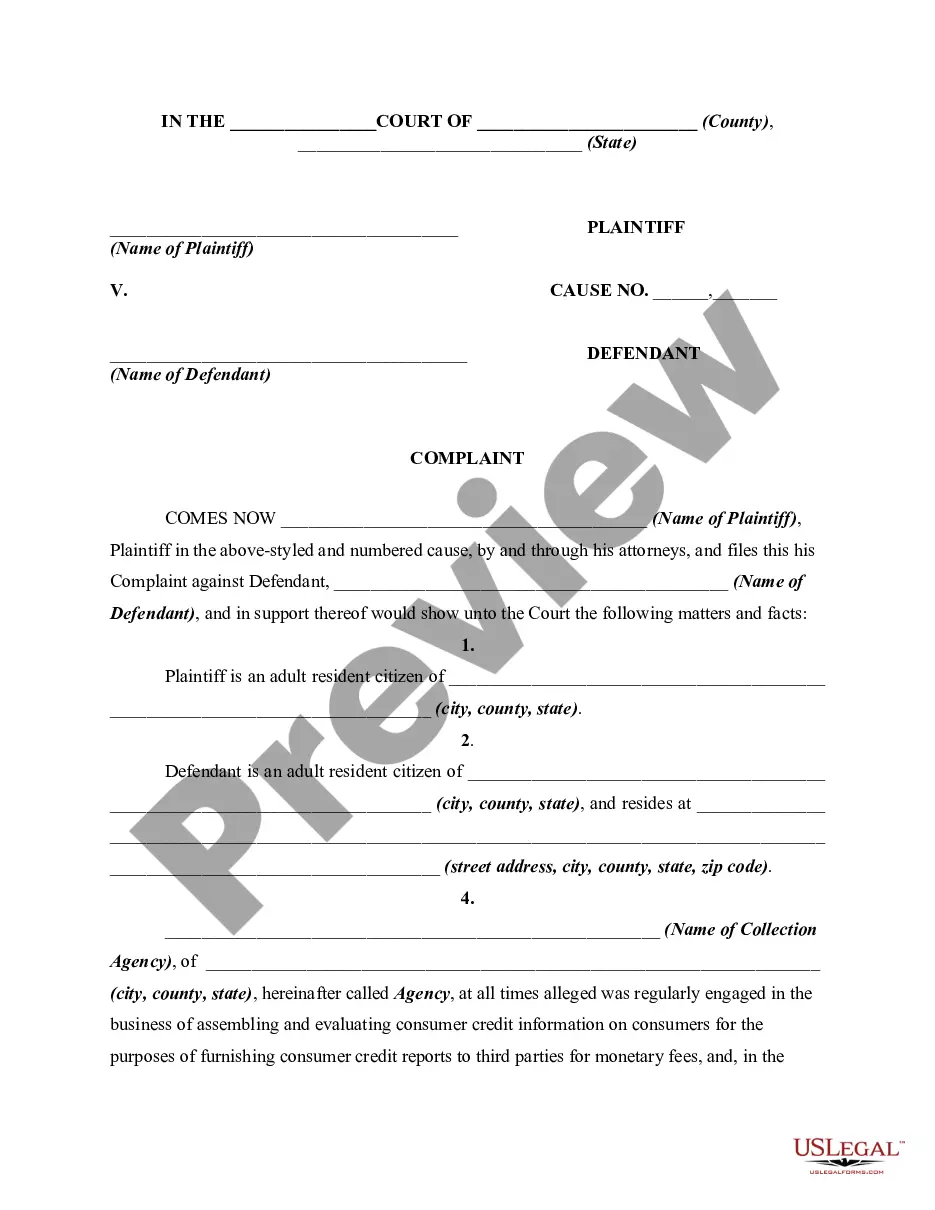

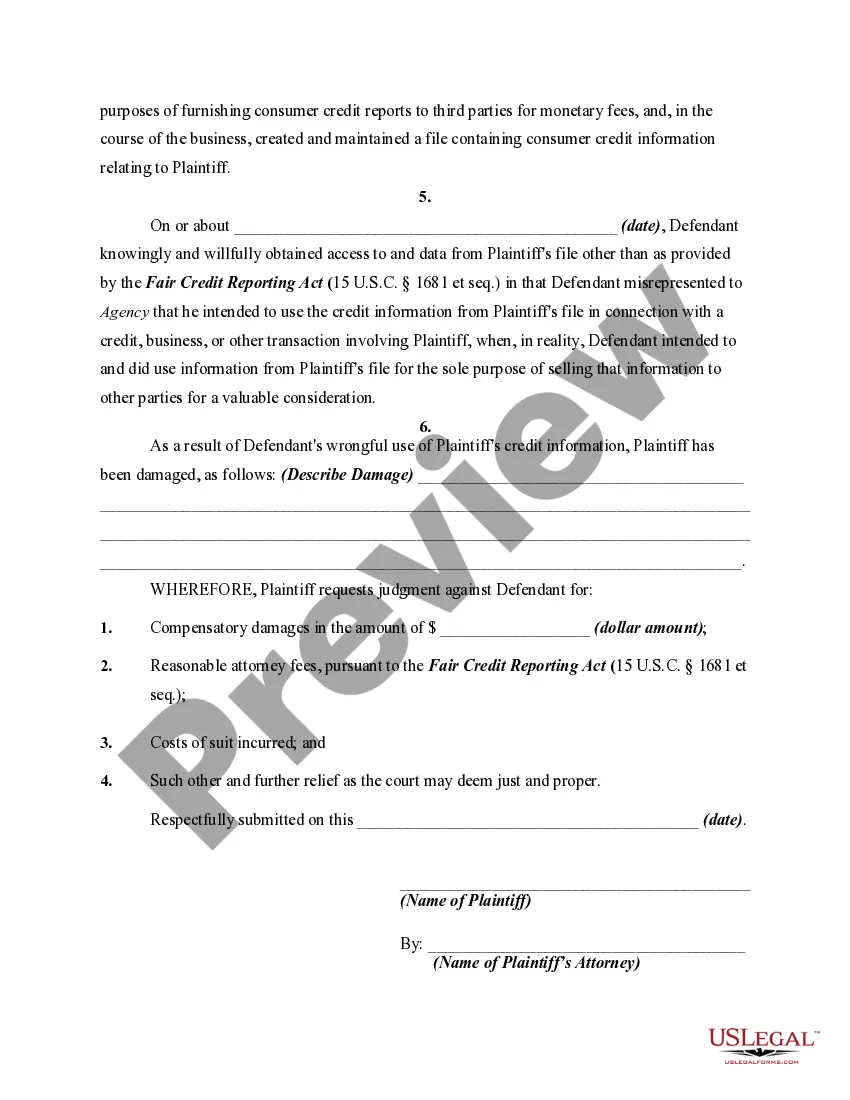

The Fair Credit Reporting Act regulates the use of information on a consumer's personal and financial condition. The most typical transaction which this Act would cover would be where a person applies for a personal loan or other consumer credit. Consumer credit is credit for personal, family, or household use, and not for business or commercial transactions. The purpose of the Act is to insure that consumer information obtained and used is done in such a way as to insure its confidentiality, accuracy, relevancy and proper utilization. Credit reporting bureaus are not permitted to disclose information to persons not having a legitimate use for this information. It is a federal crime to obtain or to furnish a credit report for an improper purpose.

Title: Understanding Michigan Complaints by Consumers against Wrongful Users of Credit Information Introduction: Michigan Complaints by Consumers against Wrongful Users of Credit Information refer to formal complaints filed by individuals who suspect their credit information has been wrongfully used or mishandled. These complaints are crucial in protecting consumers' rights and seeking action against entities responsible for unauthorized or negligent handling of credit data. This article will provide a detailed description of what Michigan Complaints by Consumers against Wrongful Users of Credit Information entail, highlighting the different types of complaints consumers can file. 1. Defining Michigan Complaints by Consumers against Wrongful Users of Credit Information: Michigan Complaints by Consumers against Wrongful Users of Credit Information involve a legal process where consumers file complaints against entities, such as lenders, creditors, or service providers, who have allegedly misused or mishandled their credit information. These complaints typically aim to rectify any harm caused by unauthorized access, identity theft, or negligence in handling sensitive credit data. 2. Types of Michigan Complaints by Consumers against Wrongful Users of Credit Information: a. Unauthorized Credit Inquiry Complaint: This type of complaint arises when a consumer notices an unauthorized credit inquiry on their credit report. Consumers can file complaints against entities responsible for performing these inquiries without their consent or a valid reason. b. Identity Theft Complaint: Identity theft complaints are filed by consumers who believe their credit information has been stolen and used fraudulently. This type of complaint seeks action against individuals or organizations responsible for using the stolen data for financial gain or other malicious purposes. c. Data Breach Complaint: Data breach complaints are raised when consumer credit information is compromised due to a breach in an entity's data security measures. Consumers can file complaints against the affected entity, holding them accountable for the negligence or inadequate protection of their credit information. d. Erroneous Reporting Complaint: This type of complaint involves cases where consumers identify inaccuracies or discrepancies in their credit reports. Consumers can file complaints against credit reporting agencies or entities providing incorrect credit information, seeking corrections to ensure fair and accurate reporting. 3. Steps to File a Michigan Complaint by Consumer against Wrongful User of Credit Information: a. Gathering Evidence: Consumers need to collect and organize necessary evidence, such as credit reports, transaction records, correspondence, or any documentation supporting their claim of unauthorized credit use or mishandling. b. Contacting the Entity: Consumers should contact the entity responsible for the wrongful use of their credit information, notifying them about the issue and seeking resolution. Documentation of this communication is crucial for the complaint process. c. Filing the Complaint: Consumers can file a formal complaint with the Michigan Attorney General's office, the Federal Trade Commission (FTC), or other relevant regulatory bodies. The complaint should include detailed information about the alleged wrongful use of credit information and supporting evidence. d. Follow-up and Resolution: After filing the complaint, consumers should vigilantly follow up with the respective regulatory bodies or investigative agencies. They may be required to provide additional documentation or cooperate in investigations to seek a resolution. Conclusion: Michigan Complaints by Consumers against Wrongful Users of Credit Information play a vital role in protecting the rights of individuals whose credit information has been wrongfully handled. By understanding the different types of complaints and following the necessary steps to file a complaint, consumers can seek justice and prevent further harm resulting from unauthorized credit use or negligent handling of their sensitive data.Title: Understanding Michigan Complaints by Consumers against Wrongful Users of Credit Information Introduction: Michigan Complaints by Consumers against Wrongful Users of Credit Information refer to formal complaints filed by individuals who suspect their credit information has been wrongfully used or mishandled. These complaints are crucial in protecting consumers' rights and seeking action against entities responsible for unauthorized or negligent handling of credit data. This article will provide a detailed description of what Michigan Complaints by Consumers against Wrongful Users of Credit Information entail, highlighting the different types of complaints consumers can file. 1. Defining Michigan Complaints by Consumers against Wrongful Users of Credit Information: Michigan Complaints by Consumers against Wrongful Users of Credit Information involve a legal process where consumers file complaints against entities, such as lenders, creditors, or service providers, who have allegedly misused or mishandled their credit information. These complaints typically aim to rectify any harm caused by unauthorized access, identity theft, or negligence in handling sensitive credit data. 2. Types of Michigan Complaints by Consumers against Wrongful Users of Credit Information: a. Unauthorized Credit Inquiry Complaint: This type of complaint arises when a consumer notices an unauthorized credit inquiry on their credit report. Consumers can file complaints against entities responsible for performing these inquiries without their consent or a valid reason. b. Identity Theft Complaint: Identity theft complaints are filed by consumers who believe their credit information has been stolen and used fraudulently. This type of complaint seeks action against individuals or organizations responsible for using the stolen data for financial gain or other malicious purposes. c. Data Breach Complaint: Data breach complaints are raised when consumer credit information is compromised due to a breach in an entity's data security measures. Consumers can file complaints against the affected entity, holding them accountable for the negligence or inadequate protection of their credit information. d. Erroneous Reporting Complaint: This type of complaint involves cases where consumers identify inaccuracies or discrepancies in their credit reports. Consumers can file complaints against credit reporting agencies or entities providing incorrect credit information, seeking corrections to ensure fair and accurate reporting. 3. Steps to File a Michigan Complaint by Consumer against Wrongful User of Credit Information: a. Gathering Evidence: Consumers need to collect and organize necessary evidence, such as credit reports, transaction records, correspondence, or any documentation supporting their claim of unauthorized credit use or mishandling. b. Contacting the Entity: Consumers should contact the entity responsible for the wrongful use of their credit information, notifying them about the issue and seeking resolution. Documentation of this communication is crucial for the complaint process. c. Filing the Complaint: Consumers can file a formal complaint with the Michigan Attorney General's office, the Federal Trade Commission (FTC), or other relevant regulatory bodies. The complaint should include detailed information about the alleged wrongful use of credit information and supporting evidence. d. Follow-up and Resolution: After filing the complaint, consumers should vigilantly follow up with the respective regulatory bodies or investigative agencies. They may be required to provide additional documentation or cooperate in investigations to seek a resolution. Conclusion: Michigan Complaints by Consumers against Wrongful Users of Credit Information play a vital role in protecting the rights of individuals whose credit information has been wrongfully handled. By understanding the different types of complaints and following the necessary steps to file a complaint, consumers can seek justice and prevent further harm resulting from unauthorized credit use or negligent handling of their sensitive data.