Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

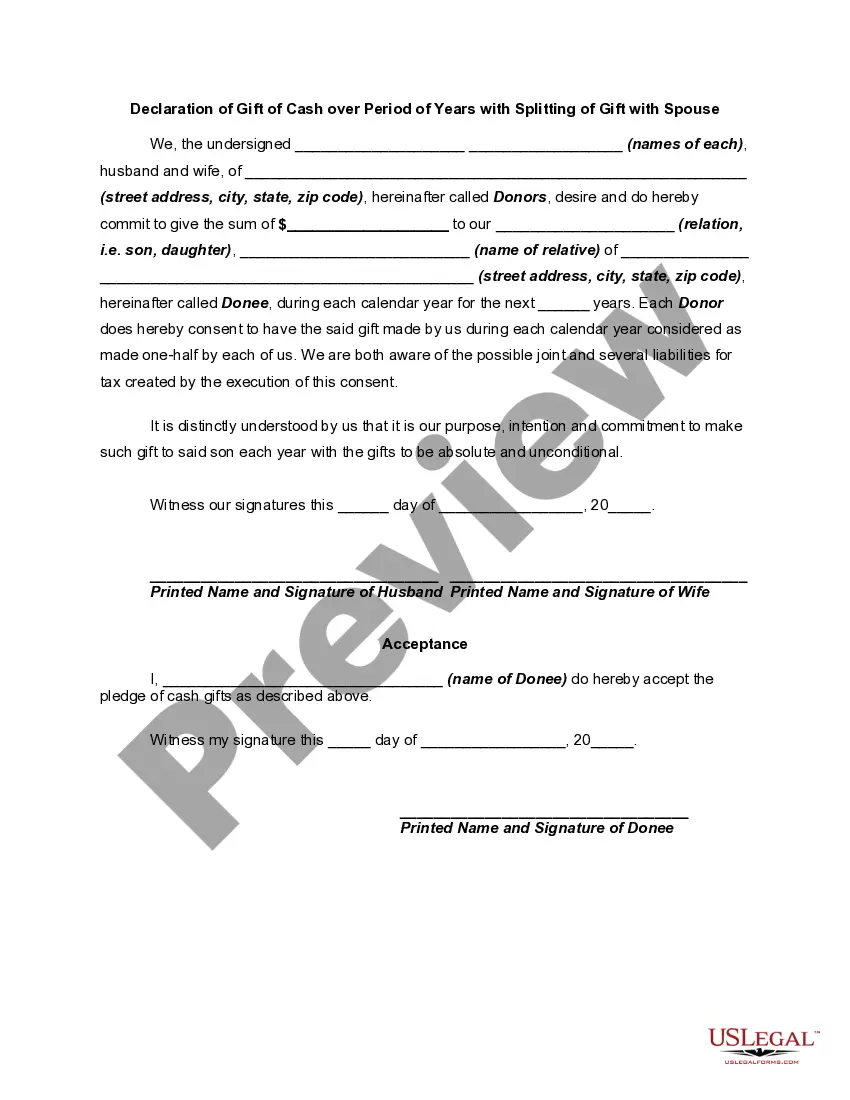

The Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make a gift of cash to another person or entity over a designated period of time, while also dividing the gift with their spouse. This declaration provides a structured and organized approach for gifting cash over the years, ensuring that both spouses have equal participation and involvement in the gift. Keywords: Michigan Declaration of Gift, cash gift, period of years, splitting of gift, gift with spouse, legal document, gifting cash, designated period of time, equal participation, involvement. Types of Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Individual Gift Splitting: This type of declaration allows an individual to make a gift of cash over a period of years while splitting the gift with their spouse. It ensures equal involvement and contribution from both spouses in the gifting process. 2. Joint Gift Splitting: In this type of declaration, both spouses join together to make a gift of cash over a designated period of time, dividing the gift equally between them. This declaration facilitates joint participation and decision-making in the gifting process. 3. Restricted Time Period Gift: This type of declaration limits the period of time over which the gift of cash can be spread. It specifies a specific timeframe during which the cash gift will be given gradually, with the option to split it with the spouse. 4. Open-ended Gift Splitting: With this declaration, individuals can make an open-ended commitment to gift cash over a period of years, with the flexibility to split the gift with their spouse. It allows for ongoing gifting with no predetermined endpoint. 5. Gradually Increasing Gift: This type of declaration outlines a gradual increase in the amount of cash gift over the years, while still allowing for the splitting of the gift with the spouse. It provides a structured approach to incrementally increase the gift amount over time. 6. Declining Gift Amount: In this type of declaration, the cash gift amount gradually decreases over the years. The declaration still enables the splitting of the gift with the spouse, ensuring both parties are involved in the gifting process while recognizing changing financial circumstances. Overall, the Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse provides a legal framework for individuals to make planned and organized cash gifts over time, allowing for the involvement of both spouses and ensuring equal participation in the gifting process.The Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows individuals to make a gift of cash to another person or entity over a designated period of time, while also dividing the gift with their spouse. This declaration provides a structured and organized approach for gifting cash over the years, ensuring that both spouses have equal participation and involvement in the gift. Keywords: Michigan Declaration of Gift, cash gift, period of years, splitting of gift, gift with spouse, legal document, gifting cash, designated period of time, equal participation, involvement. Types of Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Individual Gift Splitting: This type of declaration allows an individual to make a gift of cash over a period of years while splitting the gift with their spouse. It ensures equal involvement and contribution from both spouses in the gifting process. 2. Joint Gift Splitting: In this type of declaration, both spouses join together to make a gift of cash over a designated period of time, dividing the gift equally between them. This declaration facilitates joint participation and decision-making in the gifting process. 3. Restricted Time Period Gift: This type of declaration limits the period of time over which the gift of cash can be spread. It specifies a specific timeframe during which the cash gift will be given gradually, with the option to split it with the spouse. 4. Open-ended Gift Splitting: With this declaration, individuals can make an open-ended commitment to gift cash over a period of years, with the flexibility to split the gift with their spouse. It allows for ongoing gifting with no predetermined endpoint. 5. Gradually Increasing Gift: This type of declaration outlines a gradual increase in the amount of cash gift over the years, while still allowing for the splitting of the gift with the spouse. It provides a structured approach to incrementally increase the gift amount over time. 6. Declining Gift Amount: In this type of declaration, the cash gift amount gradually decreases over the years. The declaration still enables the splitting of the gift with the spouse, ensuring both parties are involved in the gifting process while recognizing changing financial circumstances. Overall, the Michigan Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse provides a legal framework for individuals to make planned and organized cash gifts over time, allowing for the involvement of both spouses and ensuring equal participation in the gifting process.