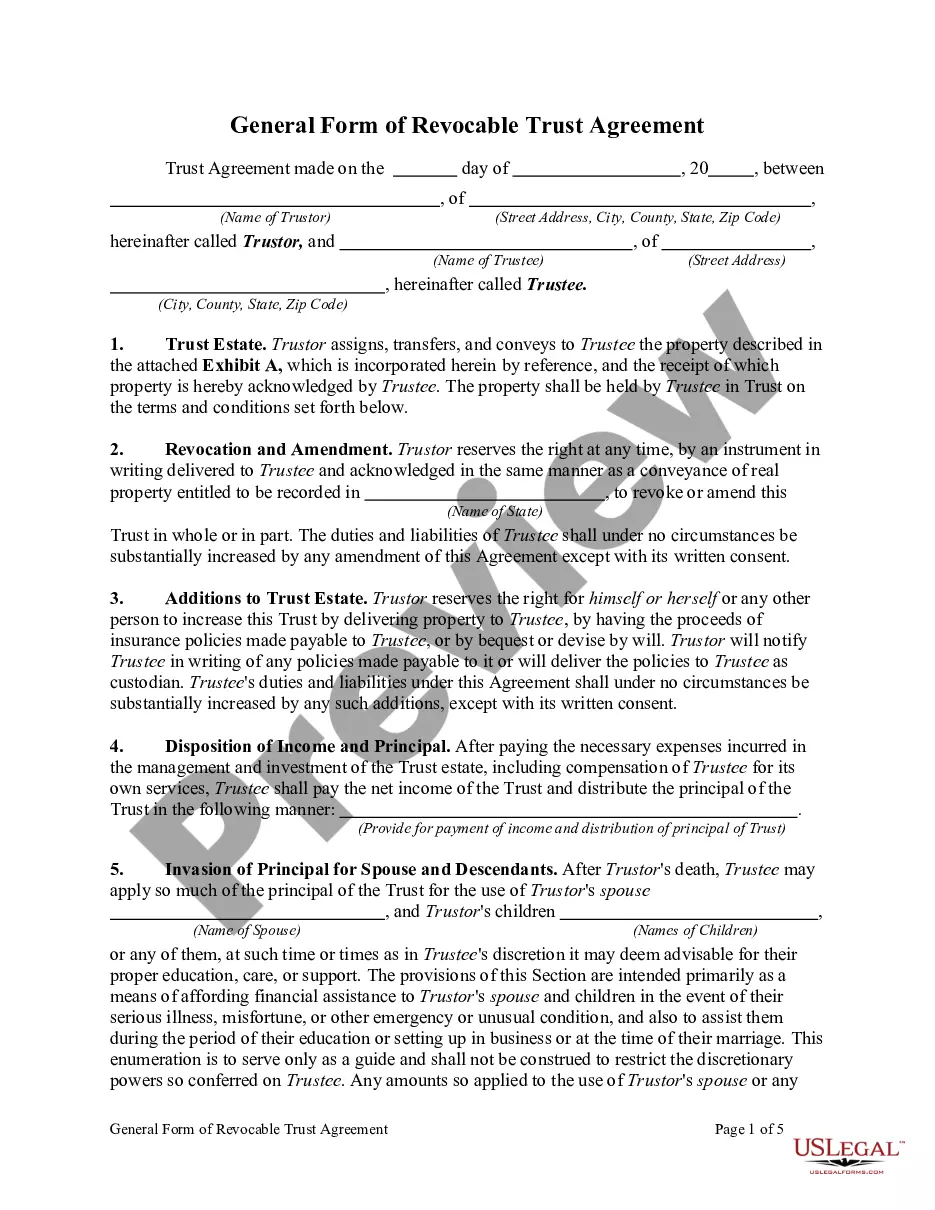

Michigan Qualifying Subchapter-S Revocable Trust Agreement

Description

How to fill out Qualifying Subchapter-S Revocable Trust Agreement?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a range of legal template types you can download or print.

Using the site, you can discover numerous forms for business and personal purposes, organized by categories, states, or keywords. You will find the latest versions of forms such as the Michigan Qualifying Subchapter-S Revocable Trust Agreement in moments.

If you already hold a membership, Log In and access the Michigan Qualifying Subchapter-S Revocable Trust Agreement from the US Legal Forms library. The Download button will appear on every form you view. You can access all previously downloaded forms in the My documents section of your account.

Complete the transaction with your credit card or PayPal account.

Select the format and download the form to your device. Make amendments. Fill out, revise, print, and sign the downloaded Michigan Qualifying Subchapter-S Revocable Trust Agreement. Each format you added to your account has no expiration date and is yours indefinitely. Therefore, to download or print another copy, just go to the My documents section and click on the form you need. Access the Michigan Qualifying Subchapter-S Revocable Trust Agreement with US Legal Forms, the most extensive library of legal template types. Utilize a wide array of professional and state-specific templates that meet your business or personal needs and requirements.

- Ensure you have selected the correct form for your location/region.

- Click on the Review button to examine the form's content.

- Check the form description to confirm that you have chosen the right form.

- If the form does not meet your needs, utilize the Search field at the top of the page to find one that does.

- Once you are satisfied with the form, validate your choice by clicking on the Buy now button.

- Next, choose the pricing plan you prefer and enter your credentials to register for an account.

Form popularity

FAQ

Yes, the IRS allows the estate of a deceased shareholder to be an S-Corporation shareholder. Note the language deceased shareholder. This indicates, correctly, that an estate can step in and become an S-Corp shareholder when a typical shareholder dies.

The election is made by filing Form 1041-T (Allocation of Estimated Tax to Beneficiaries) by the 65th day after the close of the of the trust's or estate's tax year. Please note that executors of estates may only make this election in the final year of the estate.

A trust can hold stock in an S corp only if it (1) is treated as owned by its grantor for income tax purposes under us grantor trust rules, (2) was a grantor trust immediately before its grantor's death (the trust can be a shareholder only for two years from that date), (3) received stock from the will of a decedent (

Living trusts also do not shield assets from Medicaid spend down or from creditors. To create a living trust in Michigan, you prepare the trust document then sign it in the presence of a notary. The final step is to transfer assets into the trust, funding it. Living trusts are a popular estate planning tool.

Types of Trusts Permitted as Shareholders of an S Corporation. Only certain kinds of trusts can be S corporation owners. The trust needs to be a U.S.-based trust under one of the following classifications: Grantor Sub-part E.

TRUSTS COMMONLY USED TO HOLD S CORPORATION STOCK Three commonly used types of ongoing trusts qualify as S corporation shareholders: grantor trusts, qualified subchapter S trusts (QSSTs) and electing small business trusts (ESBTs).

In order to use the 65-Day Rule, the trustee must make the 663(b) election by checking the box on line 6 under other information on page two of IRS Form 1041, the trust's fiduciary income tax return. To be valid, the election must be made by filing form 1041 by its due date, including extensions.

Since a revocable trust is not treated as separate from the grantor, it is an eligible S corporation shareholder while the grantor is alive.

They are sometimes able to wait until 1099s are actually issued to determine if a distribution under IRC 663(b) is indeed beneficial. How is the election made? The 663(b) election is made by checking the box on line 6 under Other Information at the bottom of page 2 of form 1041.

How to Create a Living Trust in MichiganDecide what type of trust you want.Next you'll need to take stock of your property.Pick a trustee.Create the trust document.Sign the trust document in front of a notary public.Fund the trust by placing property into it.