Michigan Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

Finding the correct valid document template can be a challenge.

Clearly, there is an abundance of templates accessible online, but how can you locate the authentic version you require.

Make use of the US Legal Forms website. This platform offers thousands of templates, including the Michigan Summary of Savings for Budget and Emergency Fund, that can be utilized for both business and personal purposes.

First, ensure you have selected the appropriate template for your city/region. You can review the form using the Preview button and read the form description to confirm that this is the right fit for you. If the form does not meet your criteria, use the Search bar to find the suitable form. When you are certain that the form is adequate, click the Purchase now button to get the template. Choose the pricing plan you prefer and enter the necessary information. Create your account and complete the payment using your PayPal account or credit card. Select the file format and download the valid document template to your device. Finally, complete, modify, print, and sign the acquired Michigan Summary of Savings for Budget and Emergency Fund. US Legal Forms is the largest collection of legitimate forms where you can explore various document templates. Utilize the service to download professionally crafted paperwork that adheres to state requirements.

- All forms are verified by professionals and comply with state and federal regulations.

- If you are currently registered, Log In to your account and click the Download button to obtain the Michigan Summary of Savings for Budget and Emergency Fund.

- Leverage your account to browse the legitimate forms you have acquired in the past.

- Access the My documents section of your account and download another copy of the document you require.

- If you are a new user of US Legal Forms, here are straightforward steps you should follow.

Form popularity

FAQ

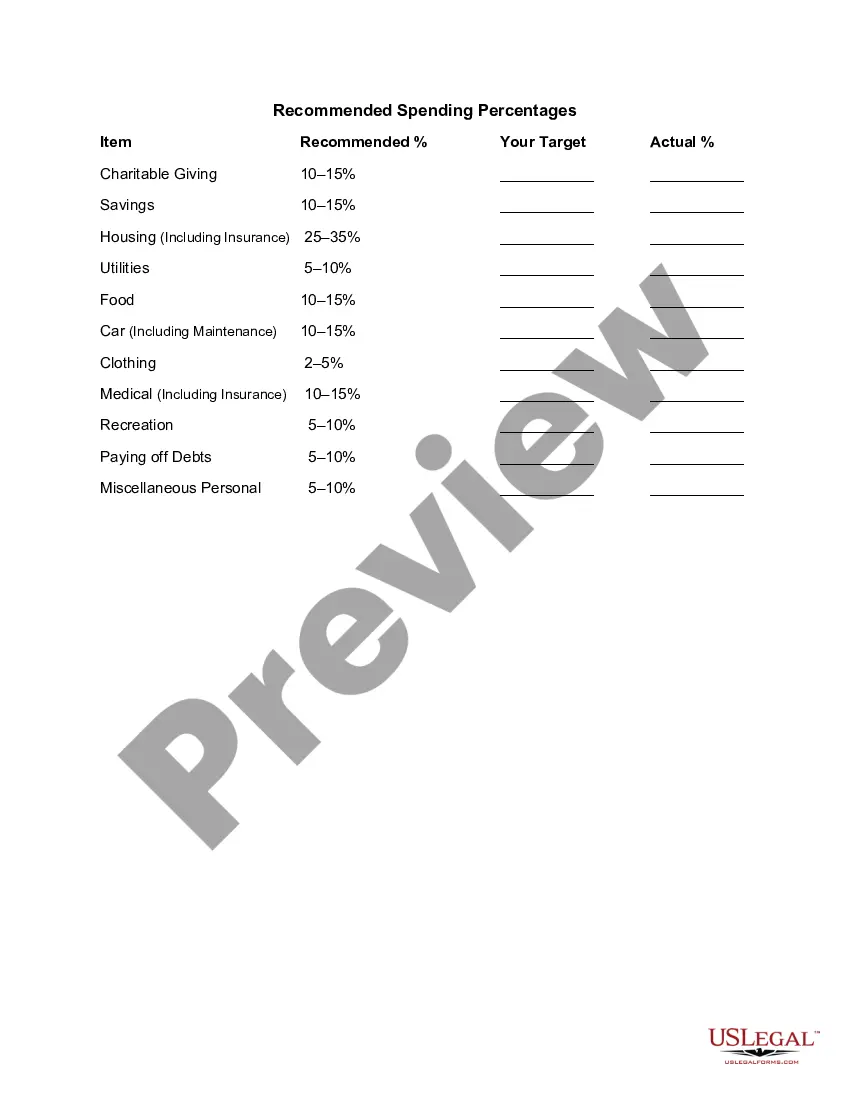

What is the 50/30/20 rule? The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

At least 20% of your income should go towards savings. Meanwhile, another 50% (maximum) should go toward necessities, while 30% goes toward discretionary items.

How much should you save each month? One popular guideline, the 50/30/20 budget, proposes spending 50% of your monthly take-home pay on necessities, 30% on wants and 20% on savings and debt repayment. For example, if you make $4,000 after taxes each month, that works out to $800 for savings and paying off debt.

What is the 50/30/20 rule? The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

It's our simple guideline for saving and spending: Aim to allocate no more than 50% of take-home pay to essential expenses, save 15% of pretax income for retirement savings, and keep 5% of take-home pay for short-term savings. (Your situation may be different, but you can use our framework as a starting point.)

But the national savings rate isn't as important as your personal savings rate. One common strategy for saving money is called the 50-30-20 rule: Spend 50 percent on needs, 30 percent on wants and put 20 percent toward savings and paying off debt.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

The rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must-have or must-do. The remaining half should be split up between 20% savings and debt repayment and 30% to everything else that you might want.

The 50/30/20 rule budget is a simple way to budget that doesn't involve detailed budgeting categories. Instead, you spend 50% of your after-tax pay on needs, 30% on wants, and 20% on savings or paying off debt.