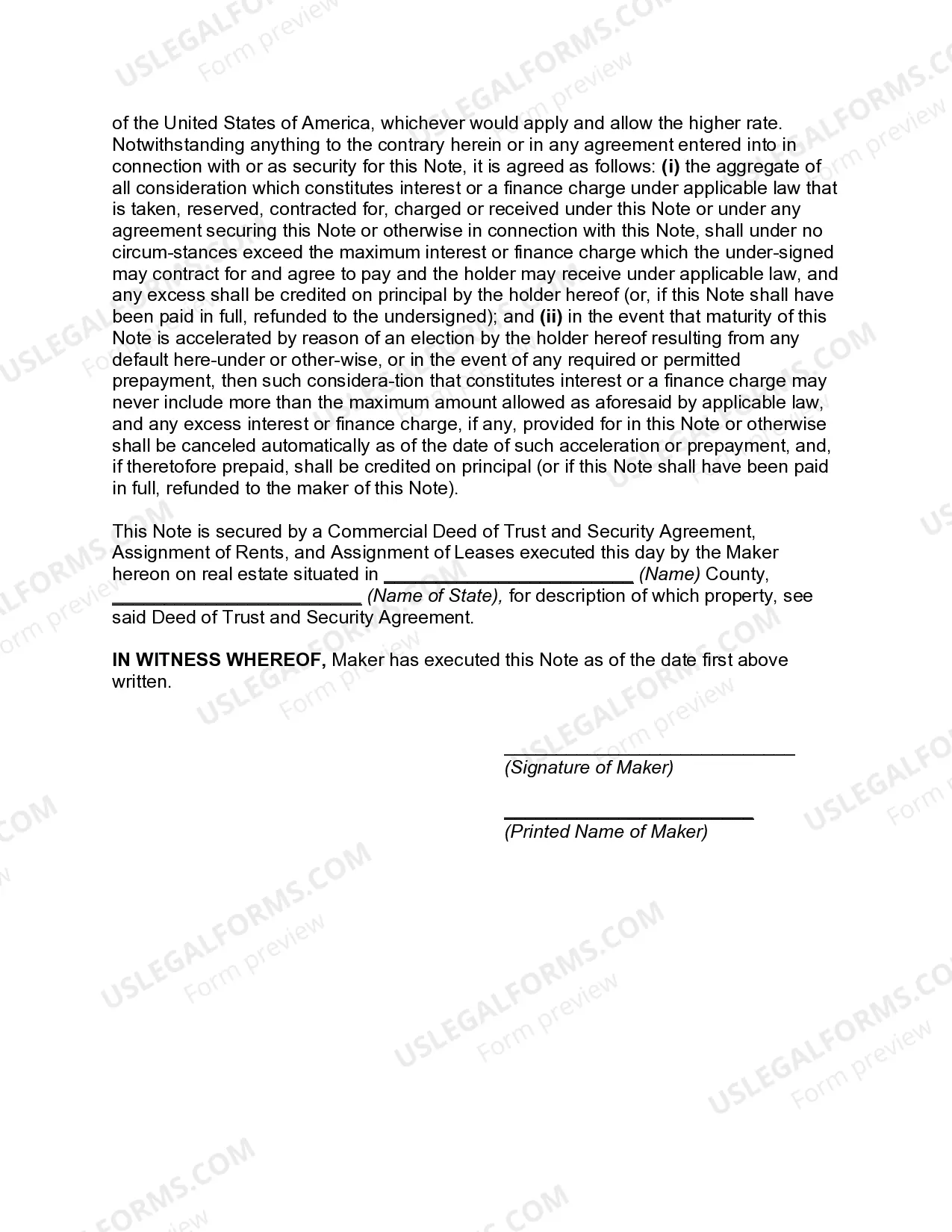

A Promissory Note is a legal document that outlines the terms and conditions of a loan agreement between a borrower (the debtor) and a lender (the creditor). In the case of commercial loans secured by real property in Michigan, a specific Promissory Note is used to secure the loan with real estate assets. The Michigan Promissory Note for Commercial Loan Secured by Real Property is a comprehensive contract that provides explicit details regarding the loan amount, interest rate, repayment terms, and property securing the loan. It serves as evidence of the borrower's promise to repay the loan amount plus interest to the lender within a specified period. Keywords: Michigan, Promissory Note, commercial loan, secured loan, real property, borrower, lender, loan agreement, loan amount, interest rate, repayment terms, property securing, evidence, promise, specified period. There may be different types or variations of the Michigan Promissory Note for Commercial Loan Secured by Real Property, including but not limited to: 1. Fixed-Rate Promissory Note: This type of Promissory Note defines a specific interest rate that remains consistent throughout the loan term. Borrowers benefit from a predictable repayment structure, ensuring stability in their monthly payment obligations. 2. Adjustable-Rate Promissory Note: Unlike a fixed-rate Promissory Note, an adjustable-rate note allows the interest rate to fluctuate over time. These notes often have a lower initial interest rate, but it can change periodically based on market conditions, potentially affecting the borrower's repayment amount. 3. Balloon Promissory Note: Balloon notes establish regular payment terms for a set period, similar to other Promissory Notes. However, they require a larger payment, often the remaining loan balance or a significant portion of it, at the end of the loan term. Balloon notes are useful for borrowers seeking lower monthly payments coupled with a final lump sum or the ability to refinance the loan before the balloon payment becomes due. 4. Installment Promissory Note: An installment note outlines a pre-determined payment schedule, specifying equal or varying payment amounts to be made at regular intervals. This type of Promissory Note enables borrowers to repay the loan in fixed or flexible installments, ensuring gradual debt reduction over time. 5. Interest-Only Promissory Note: An interest-only note allows borrowers to make payments solely towards the accrued interest for a certain period, without reducing the principal loan amount. After the interest-only period elapses, the borrower typically transitions to regular installment payments including both principal and interest. By specifying the Michigan jurisdiction in the description, it ensures that the Promissory Note adheres to the state's legal requirements, ensuring its enforceability and applicability under Michigan legislation. Remember, it is crucial to consult with legal professionals to ensure compliance with any specific Michigan laws and regulations pertaining to commercial loans secured by real property.

Michigan Promissory Note for Commercial Loan Secured by Real Property

Description

How to fill out Michigan Promissory Note For Commercial Loan Secured By Real Property?

You can invest several hours online attempting to find the legitimate papers web template that fits the state and federal requirements you require. US Legal Forms gives a huge number of legitimate varieties that are evaluated by specialists. It is simple to download or printing the Michigan Promissory Note for Commercial Loan Secured by Real Property from your support.

If you already possess a US Legal Forms accounts, it is possible to log in and click on the Down load button. Next, it is possible to complete, change, printing, or signal the Michigan Promissory Note for Commercial Loan Secured by Real Property. Each legitimate papers web template you acquire is your own property permanently. To acquire one more copy associated with a obtained form, check out the My Forms tab and click on the related button.

If you are using the US Legal Forms web site initially, stick to the basic directions under:

- Very first, be sure that you have selected the correct papers web template for your region/town of your liking. Browse the form outline to ensure you have selected the appropriate form. If available, make use of the Review button to look throughout the papers web template as well.

- In order to find one more edition of your form, make use of the Research discipline to discover the web template that suits you and requirements.

- When you have located the web template you desire, just click Get now to continue.

- Pick the prices plan you desire, enter your qualifications, and register for a free account on US Legal Forms.

- Comprehensive the financial transaction. You can use your charge card or PayPal accounts to purchase the legitimate form.

- Pick the file format of your papers and download it to your system.

- Make adjustments to your papers if needed. You can complete, change and signal and printing Michigan Promissory Note for Commercial Loan Secured by Real Property.

Down load and printing a huge number of papers layouts while using US Legal Forms Internet site, which provides the greatest assortment of legitimate varieties. Use skilled and condition-certain layouts to tackle your business or personal needs.

Form popularity

FAQ

The Difference Between a Promissory Note & a Mortgage. The main difference between a promissory note and a mortgage is that a promissory note is the written agreement containing the details of the mortgage loan, whereas a mortgage is a loan that is secured by real property.

Secured Promissory Notes The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust.

Promissory notes are ideal for individuals who do not qualify for traditional mortgages because they allow them to purchase a home by using the seller as the source of the loan and the purchased home as the source of the collateral.

There is no legal requirement for most promissory notes to be witnessed or notarized in Michigan (a promissory note for a home loan, however, may need to be notarized). Still, the parties may decide to have the document certified by a notary public for protection in the event of a lawsuit.

When a borrower takes out a loan, promissory notes legally bind them to repay it. Promissory notes also help private parties in owner financing safeguard the lending process. When a borrower pays the seller directly, mortgage lenders or banks are not involved.

Even if you have the original note, it may be void if it was not written correctly. If the person you're trying to collect from didn't sign it and yes, this happens the note is void. It may also become void if it failed some other law, for example, if it was charging an illegally high rate of interest.

What is a Secured Promissory Note? A Secured Promissory Note is a legal agreement that requires a borrower to provide security for a loan. With this lending document, the borrower puts forth their personal property or real estate as collateral if the loan isn't repaid.

As part of the home loan mortgage process, you can expect to execute both a legally binding mortgage and mortgage promissory note, which work toward complementary purposes.

Secured Promissory Notes The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document.

More info

Business Registration Your business needs an Official Form of Recognized Registration. You can register your business with your local government. Find your local government. Doing Business Nonprofit A group of individuals or companies can form a non-profit organization to conduct business. Find a non-profit company. Nonprofit Sole Proprietorship A sole proprietorship is a type of company where all the owners are the same, and you do not have to hire a manager. Find a sole proprietorship corporation. What business registration do you want? Legalism Business Registering a company Your business needs a Legal Form of Recognized Registration.