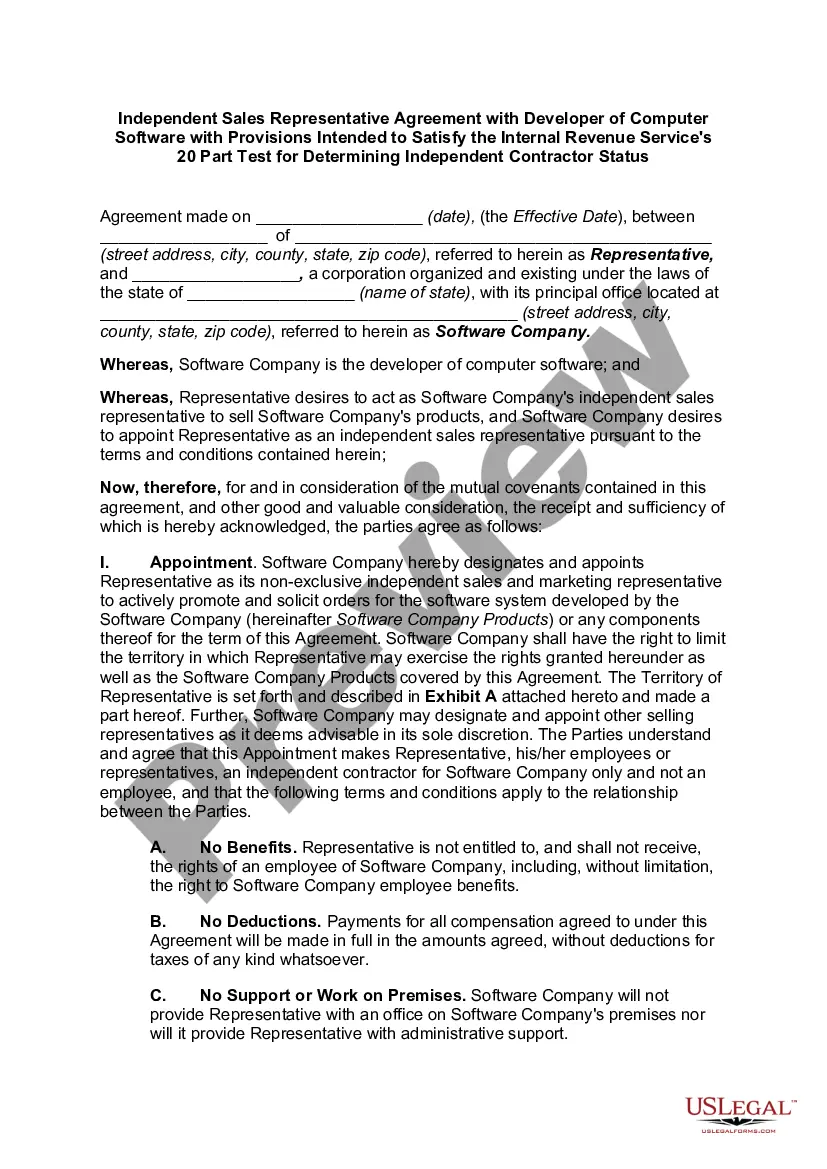

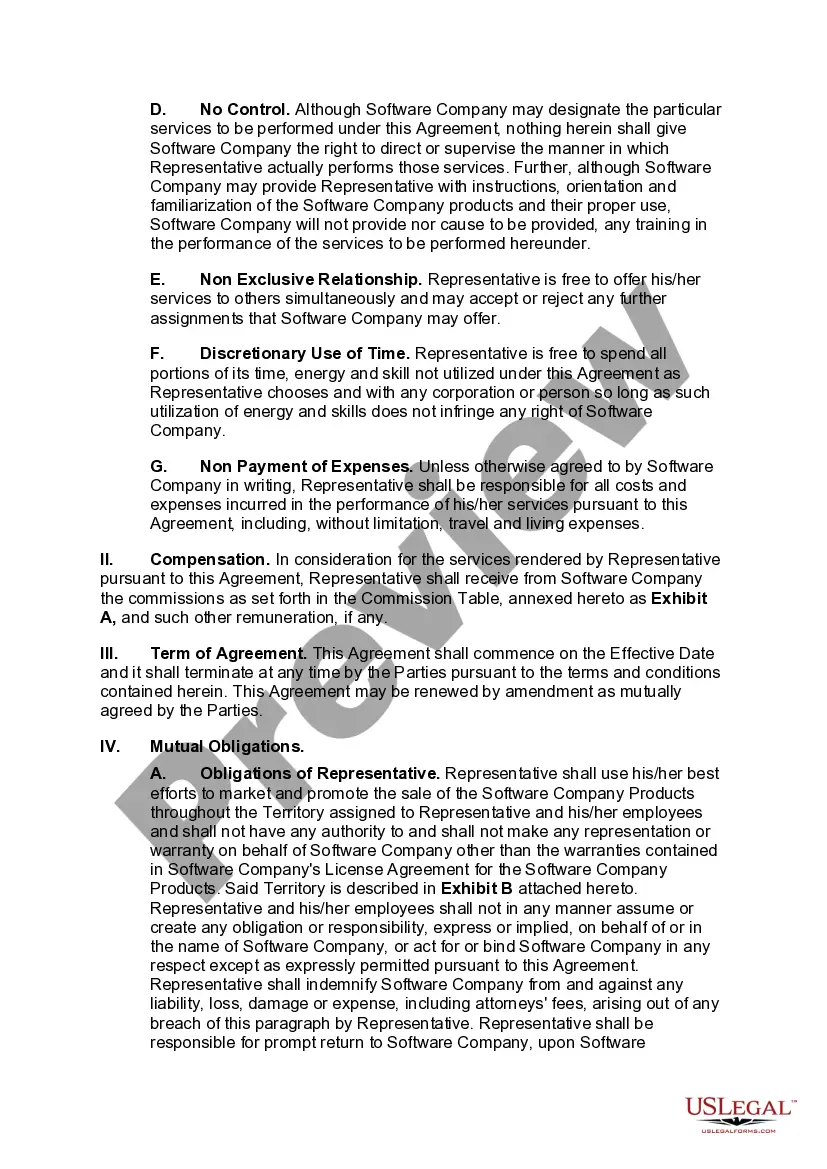

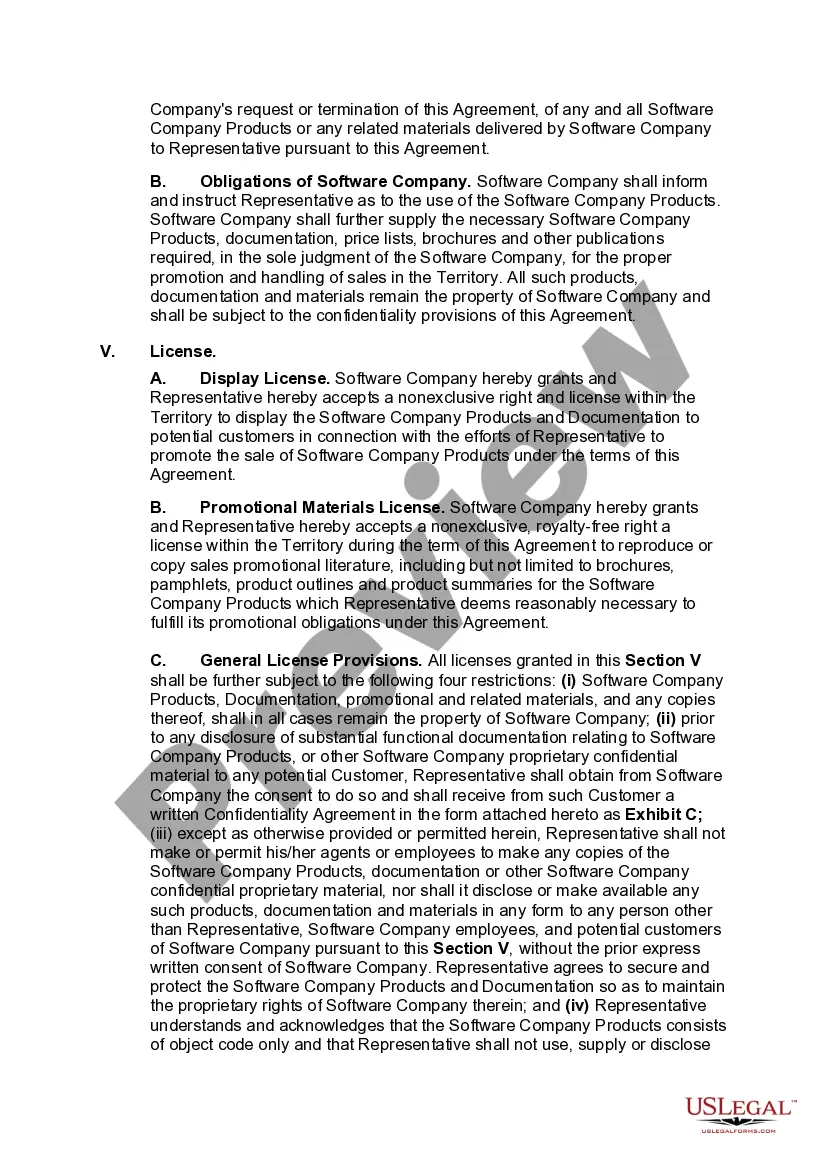

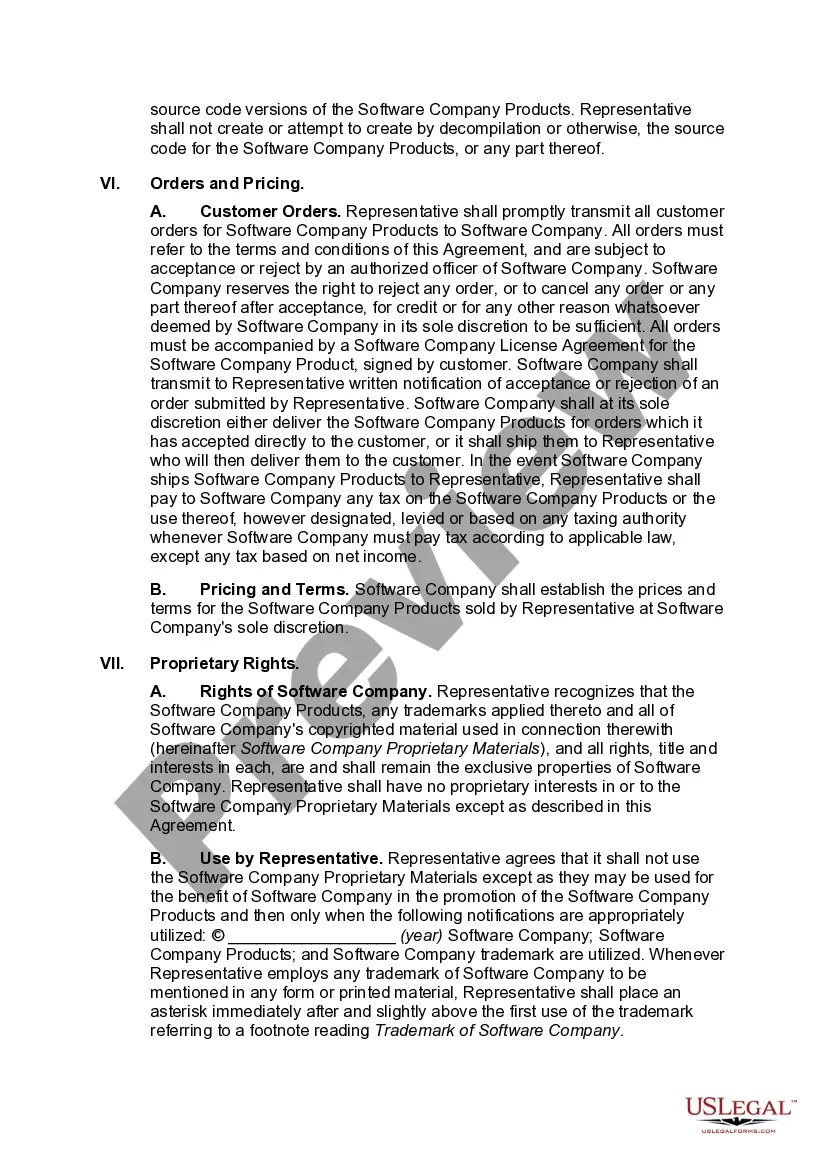

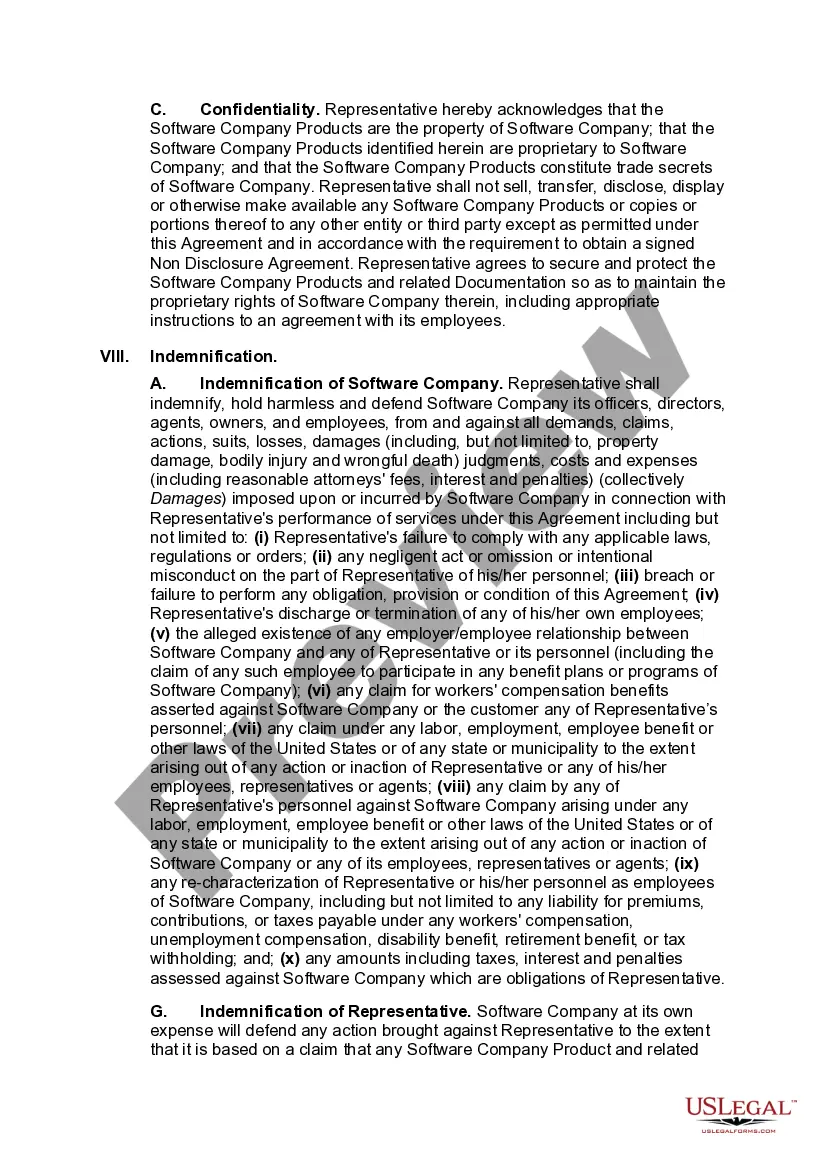

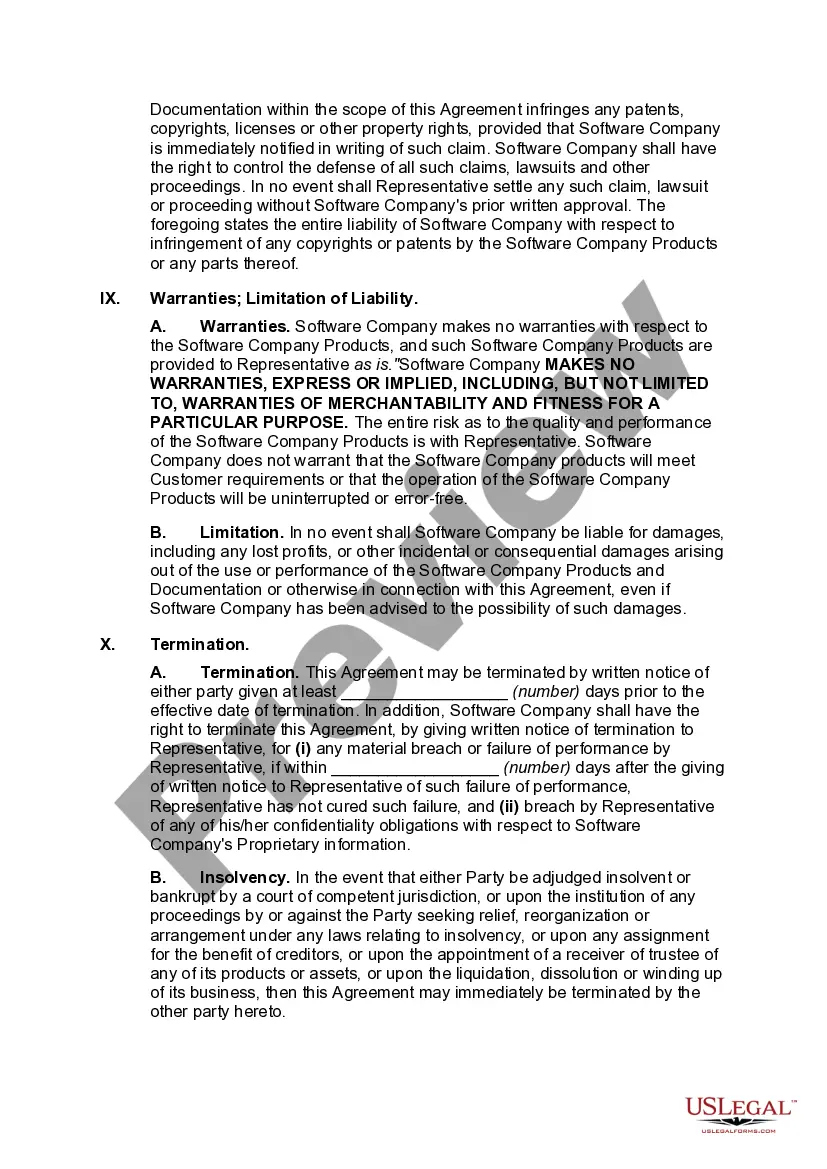

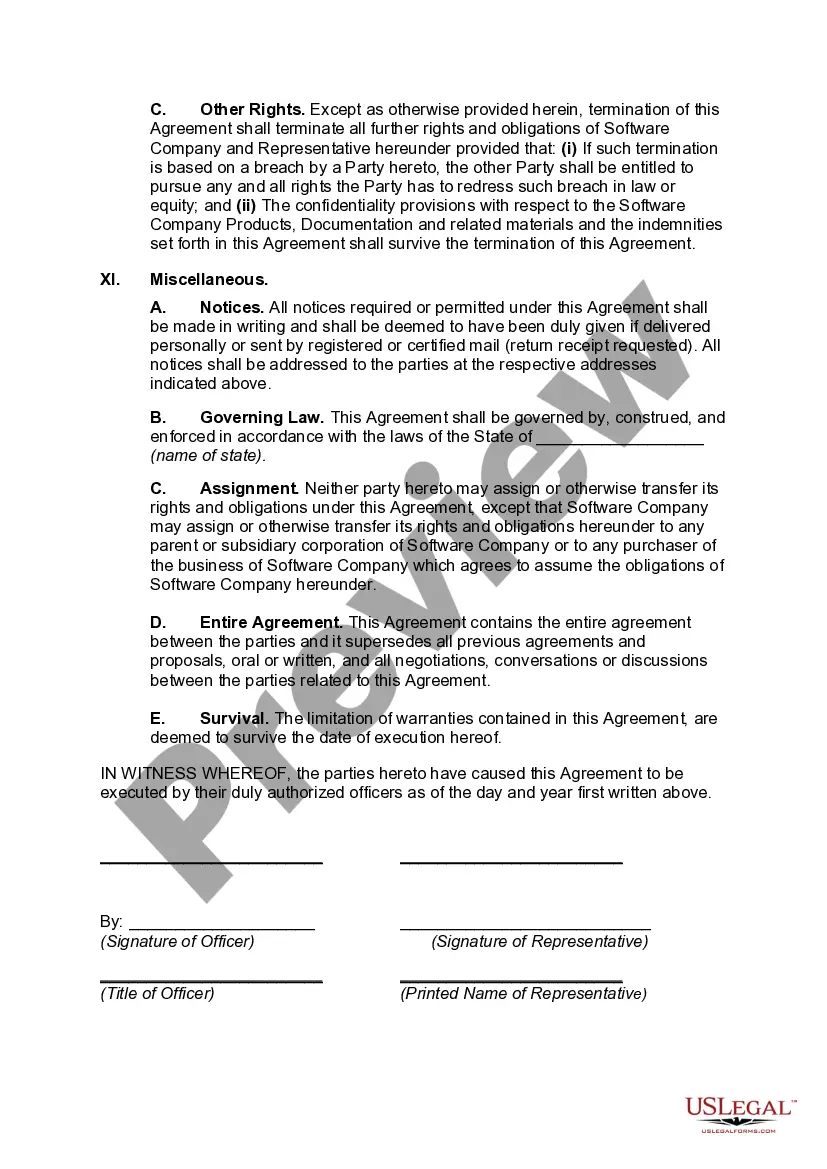

Title: Michigan Independent Sales Representative Agreement with Developer of Computer Software: A Comprehensive Guide Introduction: In the dynamic world of computer software development, it is crucial for businesses to establish clear relationships between independent sales representatives and developers. To ensure compliance with the Internal Revenue Service's (IRS) guidelines for determining independent contractor status, a well-drafted Michigan Independent Sales Representative Agreement is essential. This article will delve into the different types of agreements specifically tailored to meet the IRS's 20 part test for determining independent contractor status. By incorporating relevant keywords, we will provide a detailed description of these distinct agreements. 1. Types of Michigan Independent Sales Representative Agreements: 1.1. Exclusive Representative Agreement: An Exclusive Representative Agreement grants the sales representative exclusive rights to promote and sell the computer software within a specific territory. This agreement ensures that only one representative is authorized to represent the developer in that particular region, providing an element of control over sales and safeguarding the independent contractor status. 1.2. Non-Exclusive Representative Agreement: A Non-Exclusive Representative Agreement allows multiple sales representatives to promote and sell the computer software within a specific territory. Unlike the exclusive agreement, this arrangement offers more flexibility by allowing developers to engage with multiple independent contractors. However, it is crucial to include provisions that maintain the independent contractor status for each representative. 2. Essential Provisions for Independent Contractor Status: 2.1. Control and Independence: The agreement should clearly state that the sales representative is an independent contractor and not an employee of the developer. It should assert that the representative has the freedom to determine their own working hours, sales methods, and target customers, thereby satisfying the IRS's control factor. 2.2. Professional Services and Commissions: The agreement should outline the scope and nature of the services provided by the sales representative, specifying their responsibilities, such as marketing, sales presentations, and customer support. It should also detail the commission structure or compensation model for sales generated, reinforcing the independent contractor status. 2.3. Equipment and Expenses: To reinforce independence, the agreement should state that the sales representative will provide their own equipment, such as laptops or cell phones, necessary to carry out their tasks. Additionally, it should clarify that the sales representative will be responsible for their own expenses, such as travel costs and marketing materials. 2.4. Performance and Termination: Including provisions related to performance expectations and termination safeguards the independent contractor status. These provisions may specify sales targets, performance benchmarks, and reasons for termination, further ensuring the control factor is met. 2.5. Tax and Insurance Obligations: The agreement should explicitly state that the sales representative is responsible for their own taxes, including self-employment taxes. Additionally, it may require the sales representative to maintain their own liability insurance or professional indemnity insurance, strengthening their independent contractor status. Conclusion: Developing a comprehensive Michigan Independent Sales Representative Agreement with provisions designed to meet the IRS's 20 part test for determining independent contractor status is essential for both parties involved. Whether through an Exclusive Representative Agreement or a Non-Exclusive Representative Agreement, the inclusion of relevant keywords, along with the necessary provisions outlined in this guide, will ensure compliance with IRS guidelines, protecting the relationship between independent sales representatives and software developers.

Michigan Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status

Description

How to fill out Michigan Independent Sales Representative Agreement With Developer Of Computer Software With Provisions Intended To Satisfy The Internal Revenue Service's 20 Part Test For Determining Independent Contractor Status?

US Legal Forms - one of the greatest libraries of legal kinds in America - provides an array of legal document themes you are able to acquire or print. While using site, you may get a huge number of kinds for company and specific functions, sorted by groups, suggests, or keywords and phrases.You will discover the latest variations of kinds much like the Michigan Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status within minutes.

If you currently have a subscription, log in and acquire Michigan Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status through the US Legal Forms collection. The Acquire key will appear on each kind you see. You get access to all formerly saved kinds from the My Forms tab of your respective account.

In order to use US Legal Forms the first time, allow me to share easy recommendations to help you started off:

- Make sure you have selected the proper kind for your area/area. Click on the Review key to check the form`s content material. See the kind information to ensure that you have selected the appropriate kind.

- In the event the kind doesn`t fit your specifications, utilize the Look for field at the top of the display to find the one which does.

- Should you be happy with the shape, validate your choice by clicking on the Acquire now key. Then, opt for the rates program you favor and give your accreditations to register for the account.

- Procedure the deal. Utilize your Visa or Mastercard or PayPal account to finish the deal.

- Find the structure and acquire the shape on your own gadget.

- Make changes. Fill up, modify and print and indicator the saved Michigan Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status.

Every design you put into your account lacks an expiration day and it is yours permanently. So, if you want to acquire or print one more duplicate, just proceed to the My Forms area and click on the kind you want.

Obtain access to the Michigan Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status with US Legal Forms, probably the most comprehensive collection of legal document themes. Use a huge number of professional and state-certain themes that meet your business or specific demands and specifications.