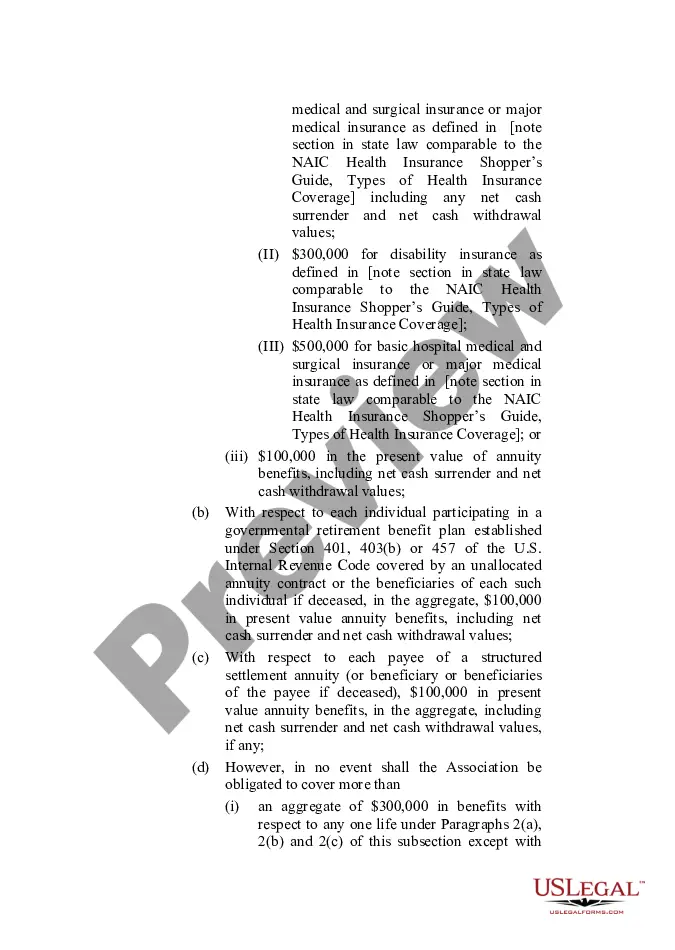

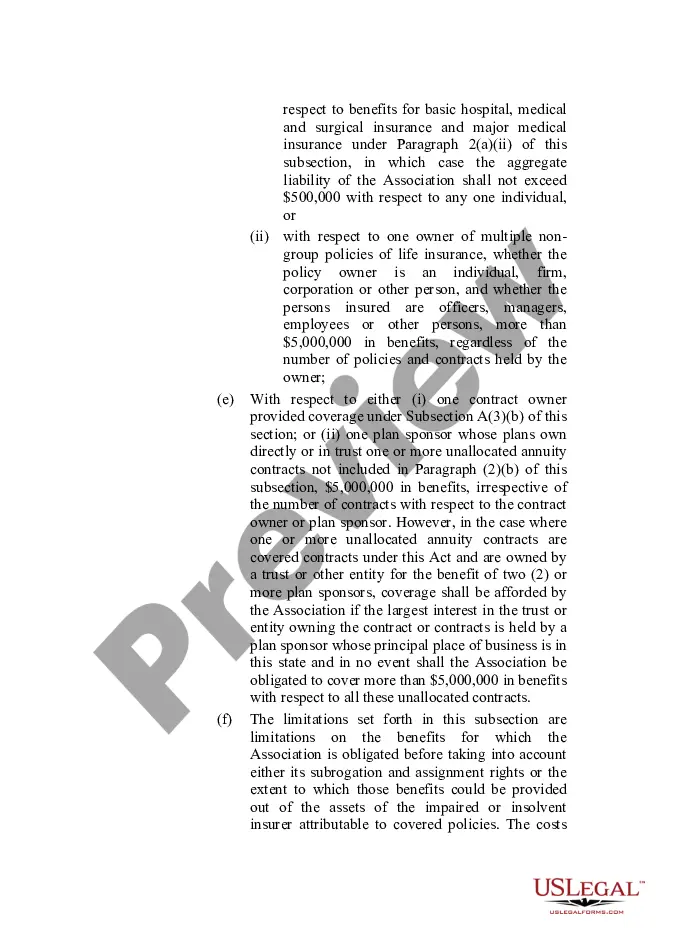

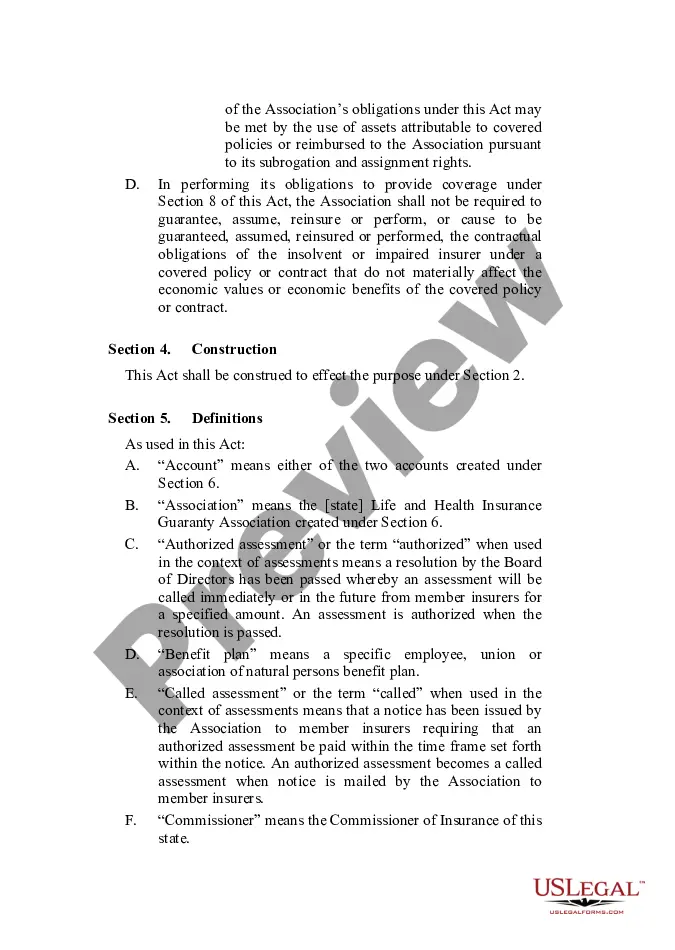

Full text and statutory guidelines for the Life and Health Insurance Guaranty Association Model Act.

The Michigan Life and Health Insurance Guaranty Association Model Act is a legislation that aims to protect policyholders in the event of an insurance company's insolvency. It serves as a safety net, ensuring that individuals with life and health insurance policies have some level of coverage if their insurer becomes insolvent and is unable to fulfill its obligations. The Michigan Life and Health Insurance Guaranty Association Model Act establishes a guaranty association, which is a safety net made up of insurance companies operating within the state. These companies pool their resources to provide coverage to policyholders of insolvent insurers. This coverage typically includes the payment of claims, continuation of coverage, and protection of policyholder interests. There may be different types of Life and Health Insurance Guaranty Association Model Acts, specific to each state. These acts are tailored to meet the individual requirements of each jurisdiction and may vary from state to state. In the case of Michigan, the Michigan Life and Health Insurance Guaranty Association Model Act is the specific legislation that governs the operations of the guaranty association within the state. Key elements of the Michigan Life and Health Insurance Guaranty Association Model Act may include: 1. Coverage Limits: The act outlines the maximum limits of coverage that the guaranty association can provide to policyholders in the event of insurer insolvency. These limits may be per policy, per policyholder, or both. 2. Covered Policies: The act defines the types of insurance policies that are eligible for coverage under the guaranty association. This typically includes life insurance, health insurance, disability insurance, long-term care insurance, and annuities. 3. Insolvency Triggers: The act specifies the conditions that must be met for an insurer to be considered insolvent, triggering the guaranty association's intervention. This may include the appointment of a receiver or liquidator for the insurer. 4. Plan of Operation: The act establishes guidelines for the operation and management of the guaranty association. It outlines the duties and responsibilities of the association's board, as well as reporting and assessment requirements. 5. Assessments: The act details the process by which insurers operating within the state are assessed to fund the guaranty association's activities. This may involve the collection of regular assessments or emergency assessments in times of insolvency. 6. Claims Handling: The act sets procedures for the filing and handling of claims by policyholders. It ensures that eligible claims are processed and paid in a timely manner, subject to the coverage limits defined in the act. Overall, the Michigan Life and Health Insurance Guaranty Association Model Act plays a vital role in safeguarding the interests of policyholders in Michigan. By establishing a guaranty association and providing a framework for addressing insurer insolvency, it helps maintain stability and consumer confidence in the life and health insurance industry.The Michigan Life and Health Insurance Guaranty Association Model Act is a legislation that aims to protect policyholders in the event of an insurance company's insolvency. It serves as a safety net, ensuring that individuals with life and health insurance policies have some level of coverage if their insurer becomes insolvent and is unable to fulfill its obligations. The Michigan Life and Health Insurance Guaranty Association Model Act establishes a guaranty association, which is a safety net made up of insurance companies operating within the state. These companies pool their resources to provide coverage to policyholders of insolvent insurers. This coverage typically includes the payment of claims, continuation of coverage, and protection of policyholder interests. There may be different types of Life and Health Insurance Guaranty Association Model Acts, specific to each state. These acts are tailored to meet the individual requirements of each jurisdiction and may vary from state to state. In the case of Michigan, the Michigan Life and Health Insurance Guaranty Association Model Act is the specific legislation that governs the operations of the guaranty association within the state. Key elements of the Michigan Life and Health Insurance Guaranty Association Model Act may include: 1. Coverage Limits: The act outlines the maximum limits of coverage that the guaranty association can provide to policyholders in the event of insurer insolvency. These limits may be per policy, per policyholder, or both. 2. Covered Policies: The act defines the types of insurance policies that are eligible for coverage under the guaranty association. This typically includes life insurance, health insurance, disability insurance, long-term care insurance, and annuities. 3. Insolvency Triggers: The act specifies the conditions that must be met for an insurer to be considered insolvent, triggering the guaranty association's intervention. This may include the appointment of a receiver or liquidator for the insurer. 4. Plan of Operation: The act establishes guidelines for the operation and management of the guaranty association. It outlines the duties and responsibilities of the association's board, as well as reporting and assessment requirements. 5. Assessments: The act details the process by which insurers operating within the state are assessed to fund the guaranty association's activities. This may involve the collection of regular assessments or emergency assessments in times of insolvency. 6. Claims Handling: The act sets procedures for the filing and handling of claims by policyholders. It ensures that eligible claims are processed and paid in a timely manner, subject to the coverage limits defined in the act. Overall, the Michigan Life and Health Insurance Guaranty Association Model Act plays a vital role in safeguarding the interests of policyholders in Michigan. By establishing a guaranty association and providing a framework for addressing insurer insolvency, it helps maintain stability and consumer confidence in the life and health insurance industry.