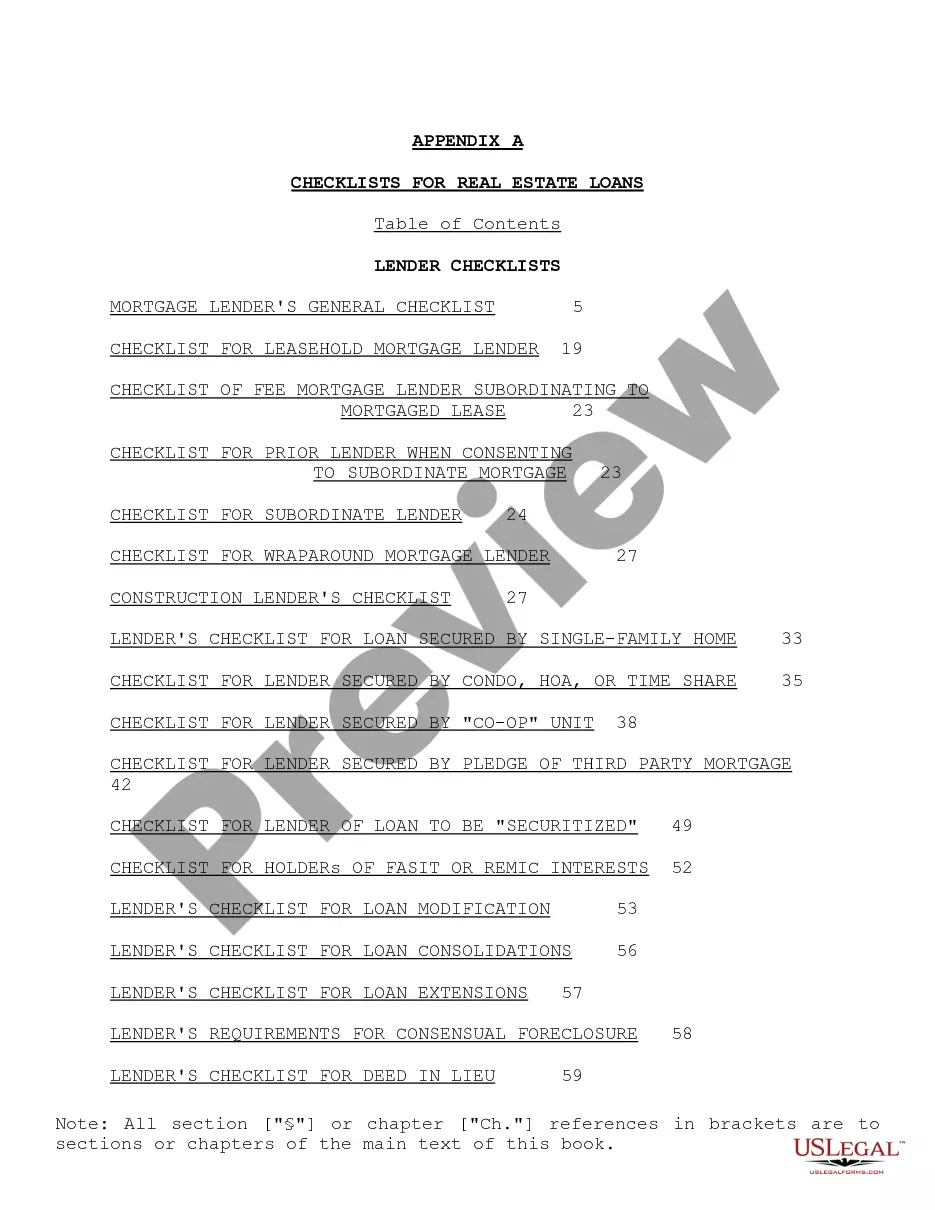

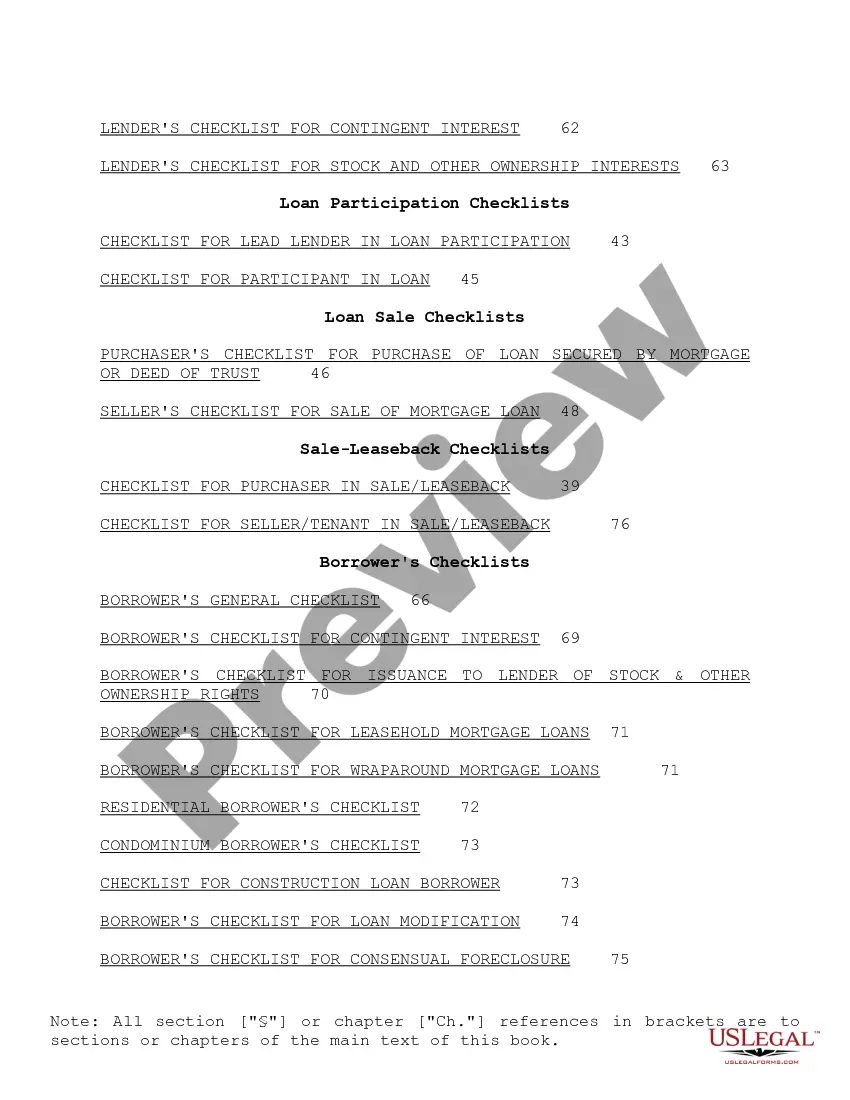

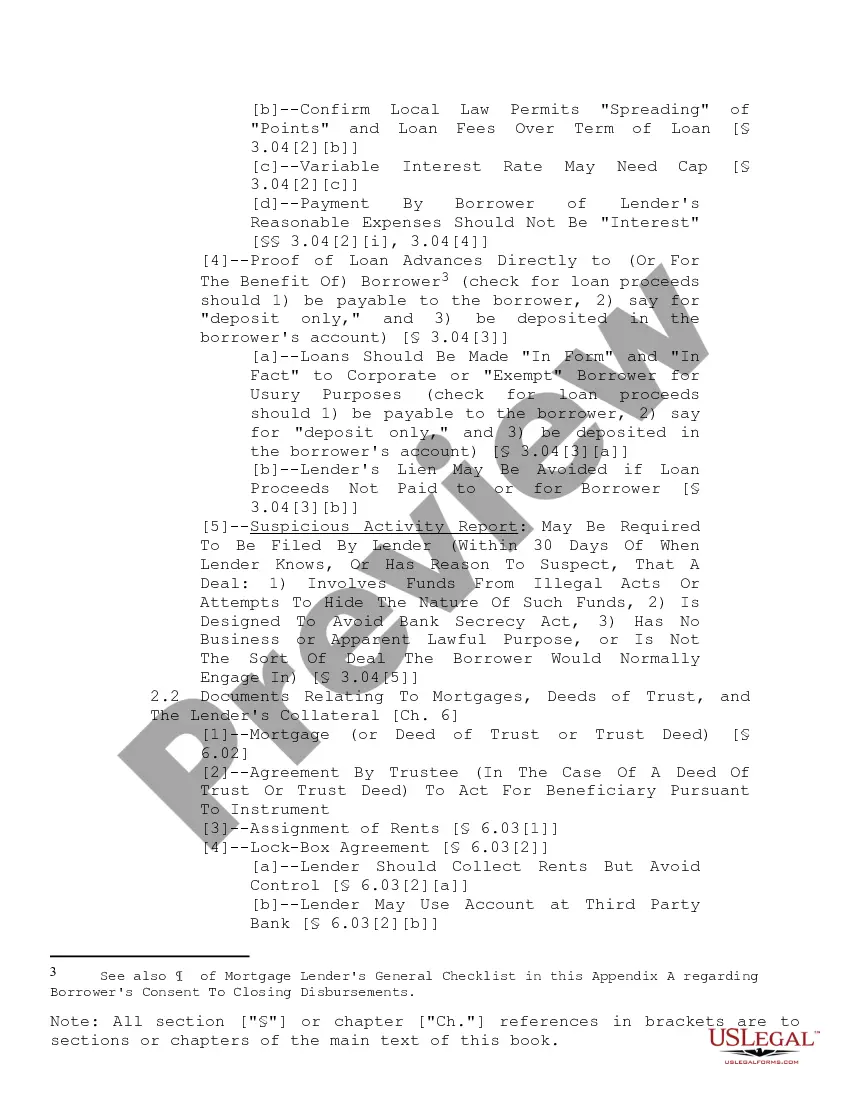

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Title: Michigan Checklist for Real Estate Loans: A Comprehensive Guide Keywords: Michigan real estate loans, checklist, loan application, loan requirements, mortgage process, types of loans Introduction: If you are planning to invest in the Michigan real estate market, understanding the loan process is essential. A checklist acts as a crucial tool that helps borrowers stay organized, ensuring they meet all the requirements to secure a real estate loan successfully. In this article, we will outline the detailed process of obtaining a real estate loan in Michigan, including various types of loans available. Michigan Checklist for Real Estate Loans: 1. Loan Application and Documentation: a. Complete loan application form accurately. b. Provide proof of income and employment history. c. Present bank statements for the previous few months. d. Furnish tax returns and W2 forms for the past two years. e. Prepare a list of all debts and liabilities. f. Gather personal identification documents such as driver's license or passport. 2. Credit Score and Credit History: a. Ensure a good credit score by reviewing credit reports. b. Pay off outstanding debts and fix any errors on the credit report. c. Maintain a low credit utilization ratio. d. Avoid opening new credit accounts during the loan process. 3. Down Payment and Reserves: a. Determine a suitable down payment amount. b. Arrange necessary funds for the down payment, closing costs, and reserves. c. Verify the source of funds and ensure they are readily available. 4. Property Appraisal and Inspection: a. Order a professional appraisal of the property. b. Schedule a thorough inspection to identify any potential issues. c. Address any significant concerns raised during the inspection. 5. Mortgage Types in Michigan: a. Conventional loans: Traditional loans offered by banks or financial institutions. b. FHA loans: Insured by the Federal Housing Administration, ideal for first-time homebuyers with a low down payment. c. VA loans: Available to eligible veterans, active-duty service members, and surviving spouses. d. USDA loans: Designed for properties in rural areas, offering low-interest rates and zero down payment options. Conclusion: Obtaining a real estate loan in Michigan requires thorough preparation and adherence to specific guidelines. Following the Michigan Checklist for Real Estate Loans will help borrowers stay organized, increase their chances of loan approval, and navigate the mortgage process efficiently. Whether opting for conventional loans, FHA loans, VA loans, or USDA loans, understanding the particular requirements for each loan type is crucial. By utilizing this checklist, potential buyers can ensure a smooth loan process and embark on their real estate investment journey in Michigan with confidence.Title: Michigan Checklist for Real Estate Loans: A Comprehensive Guide Keywords: Michigan real estate loans, checklist, loan application, loan requirements, mortgage process, types of loans Introduction: If you are planning to invest in the Michigan real estate market, understanding the loan process is essential. A checklist acts as a crucial tool that helps borrowers stay organized, ensuring they meet all the requirements to secure a real estate loan successfully. In this article, we will outline the detailed process of obtaining a real estate loan in Michigan, including various types of loans available. Michigan Checklist for Real Estate Loans: 1. Loan Application and Documentation: a. Complete loan application form accurately. b. Provide proof of income and employment history. c. Present bank statements for the previous few months. d. Furnish tax returns and W2 forms for the past two years. e. Prepare a list of all debts and liabilities. f. Gather personal identification documents such as driver's license or passport. 2. Credit Score and Credit History: a. Ensure a good credit score by reviewing credit reports. b. Pay off outstanding debts and fix any errors on the credit report. c. Maintain a low credit utilization ratio. d. Avoid opening new credit accounts during the loan process. 3. Down Payment and Reserves: a. Determine a suitable down payment amount. b. Arrange necessary funds for the down payment, closing costs, and reserves. c. Verify the source of funds and ensure they are readily available. 4. Property Appraisal and Inspection: a. Order a professional appraisal of the property. b. Schedule a thorough inspection to identify any potential issues. c. Address any significant concerns raised during the inspection. 5. Mortgage Types in Michigan: a. Conventional loans: Traditional loans offered by banks or financial institutions. b. FHA loans: Insured by the Federal Housing Administration, ideal for first-time homebuyers with a low down payment. c. VA loans: Available to eligible veterans, active-duty service members, and surviving spouses. d. USDA loans: Designed for properties in rural areas, offering low-interest rates and zero down payment options. Conclusion: Obtaining a real estate loan in Michigan requires thorough preparation and adherence to specific guidelines. Following the Michigan Checklist for Real Estate Loans will help borrowers stay organized, increase their chances of loan approval, and navigate the mortgage process efficiently. Whether opting for conventional loans, FHA loans, VA loans, or USDA loans, understanding the particular requirements for each loan type is crucial. By utilizing this checklist, potential buyers can ensure a smooth loan process and embark on their real estate investment journey in Michigan with confidence.