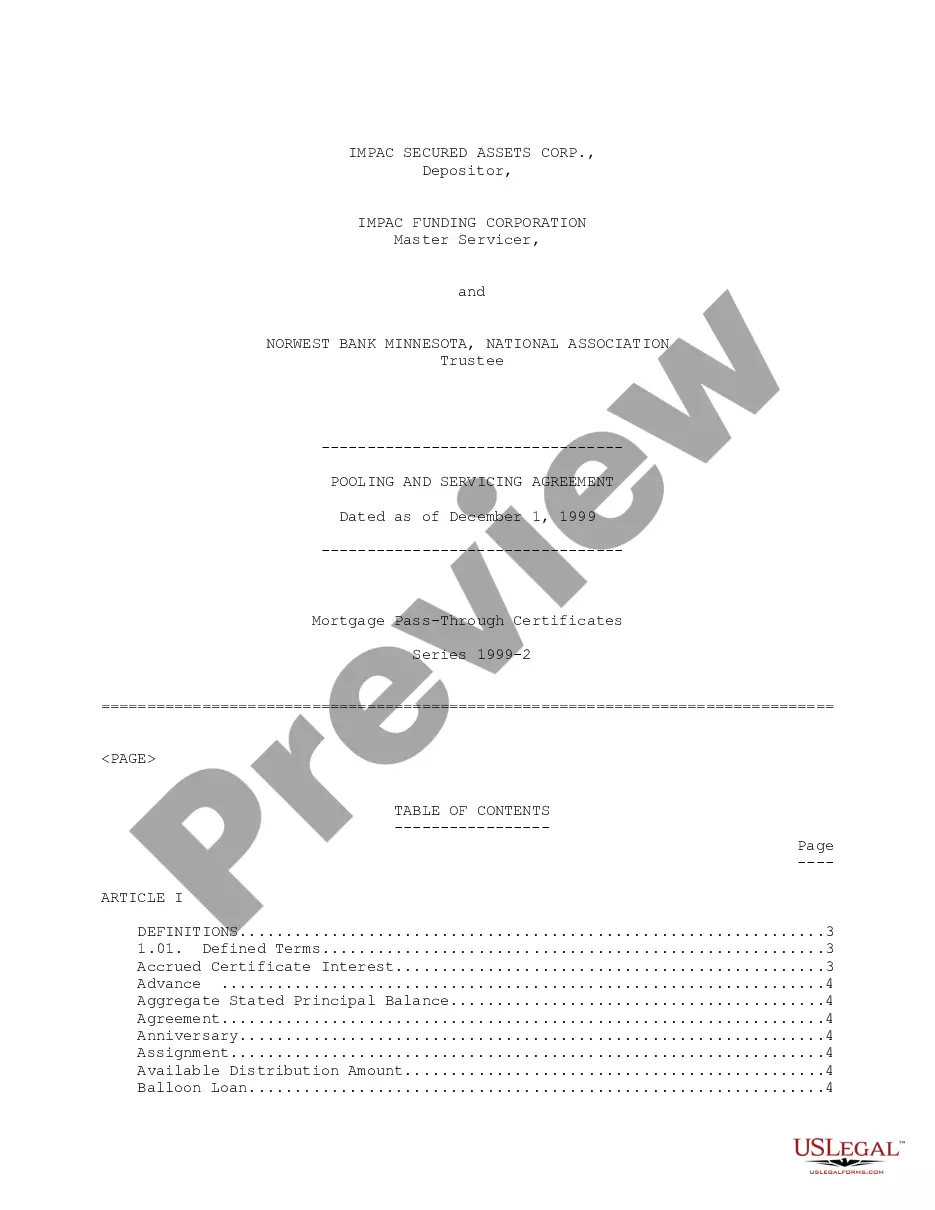

The Michigan Amended and Restated Principal Underwriting Agreement regarding Issuance of variable annuity contracts and life insurance is a legal document that outlines the terms and conditions governing the underwriting process for variable annuity contracts and life insurance policies in the state of Michigan. This agreement is specifically designed to protect both the insurer and the policyholders by ensuring compliance with applicable laws and regulations while facilitating the issuance of these financial products. It establishes a comprehensive framework for the underwriting process, including the evaluation of risk, determination of premiums, and the overall management of the policies. The agreement covers a range of important elements to ensure the smooth and efficient issuance of variable annuity contracts and life insurance policies. This includes the procedures for evaluating potential policyholders, such as assessing their health, financial stability, and insurability. It also defines the criteria for setting premium rates, taking into account the policyholder's age, gender, and other relevant factors. Under the Michigan Amended and Restated Principal Underwriting Agreement, the insurer also outlines the required disclosures and documentation that need to be provided to policyholders regarding the terms and conditions of the policies. This includes clear explanations of the benefits, limitations, and exclusions, as well as any potential risks associated with the products. In addition, the agreement addresses the ongoing management of the policies, including the process for policy modifications, renewals, and terminations. It also outlines the responsibilities and obligations of both the insurer and the policyholder, ensuring that all parties are aware of their rights and responsibilities throughout the duration of the contract. The Michigan Amended and Restated Principal Underwriting Agreement is a vital legal document that protects the interests of both the insurer and the policyholders. It ensures transparency, fairness, and compliance throughout the entire underwriting process, facilitating the issuance of variable annuity contracts and life insurance policies in the state of Michigan. Other types of related Michigan Amended and Restated Principal Underwriting Agreements may include specific variations or adaptations of the agreement for different types of variable annuities or life insurance policies. These variations may address specialized underwriting considerations, unique product features, or specific regulatory requirements for certain classes of insured individuals or policy types. It is important for insurers to carefully review and tailor the agreement to suit their specific offerings and comply with relevant laws and regulations.

The Michigan Amended and Restated Principal Underwriting Agreement regarding Issuance of variable annuity contracts and life insurance is a legal document that outlines the terms and conditions governing the underwriting process for variable annuity contracts and life insurance policies in the state of Michigan. This agreement is specifically designed to protect both the insurer and the policyholders by ensuring compliance with applicable laws and regulations while facilitating the issuance of these financial products. It establishes a comprehensive framework for the underwriting process, including the evaluation of risk, determination of premiums, and the overall management of the policies. The agreement covers a range of important elements to ensure the smooth and efficient issuance of variable annuity contracts and life insurance policies. This includes the procedures for evaluating potential policyholders, such as assessing their health, financial stability, and insurability. It also defines the criteria for setting premium rates, taking into account the policyholder's age, gender, and other relevant factors. Under the Michigan Amended and Restated Principal Underwriting Agreement, the insurer also outlines the required disclosures and documentation that need to be provided to policyholders regarding the terms and conditions of the policies. This includes clear explanations of the benefits, limitations, and exclusions, as well as any potential risks associated with the products. In addition, the agreement addresses the ongoing management of the policies, including the process for policy modifications, renewals, and terminations. It also outlines the responsibilities and obligations of both the insurer and the policyholder, ensuring that all parties are aware of their rights and responsibilities throughout the duration of the contract. The Michigan Amended and Restated Principal Underwriting Agreement is a vital legal document that protects the interests of both the insurer and the policyholders. It ensures transparency, fairness, and compliance throughout the entire underwriting process, facilitating the issuance of variable annuity contracts and life insurance policies in the state of Michigan. Other types of related Michigan Amended and Restated Principal Underwriting Agreements may include specific variations or adaptations of the agreement for different types of variable annuities or life insurance policies. These variations may address specialized underwriting considerations, unique product features, or specific regulatory requirements for certain classes of insured individuals or policy types. It is important for insurers to carefully review and tailor the agreement to suit their specific offerings and comply with relevant laws and regulations.