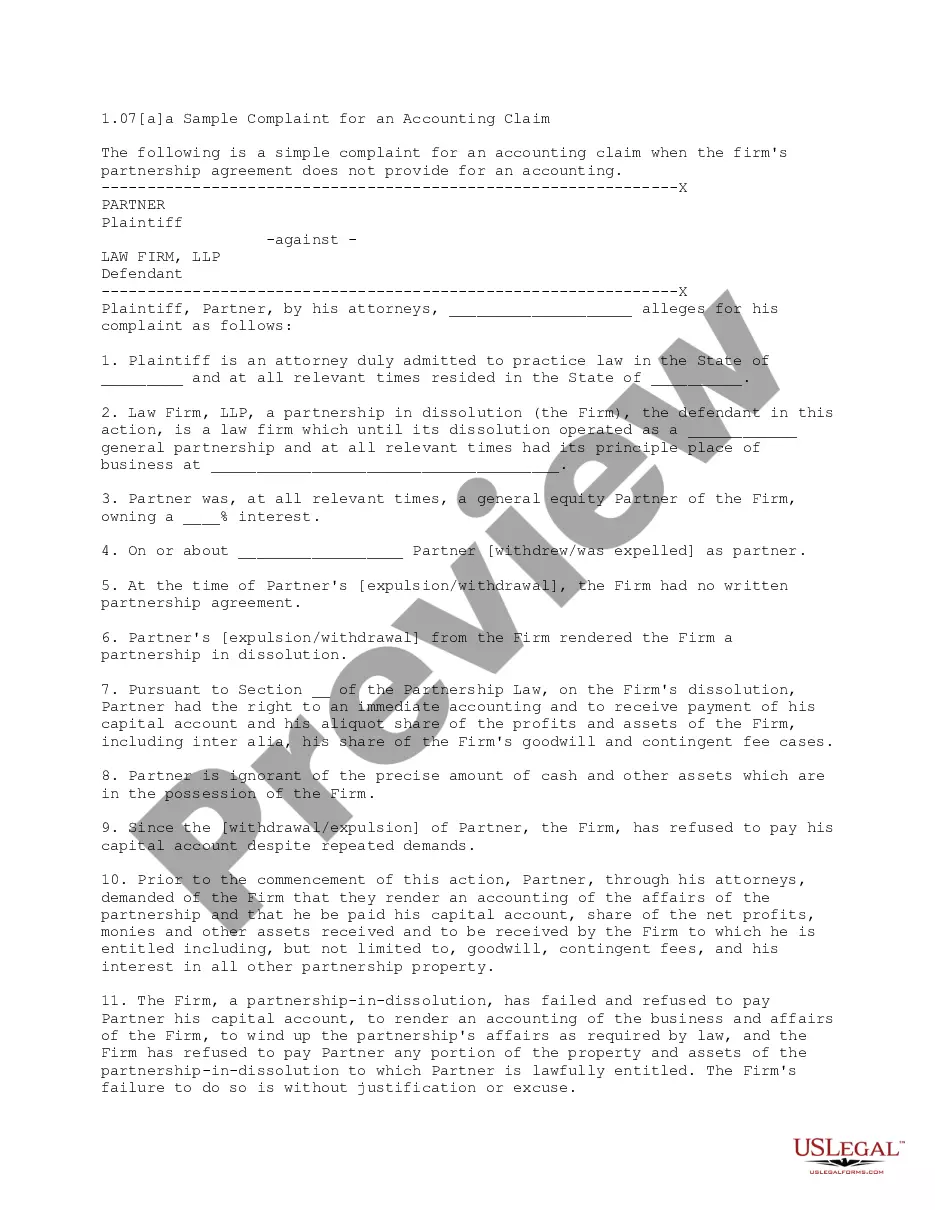

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Michigan Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

Finding the right lawful record format might be a battle. Obviously, there are a lot of themes available on the net, but how do you obtain the lawful type you want? Utilize the US Legal Forms site. The assistance offers 1000s of themes, such as the Michigan Alternative Complaint for an Accounting which includes Egregious Acts, that you can use for organization and personal requirements. Each of the kinds are checked by specialists and satisfy state and federal demands.

In case you are presently signed up, log in in your bank account and click the Acquire button to obtain the Michigan Alternative Complaint for an Accounting which includes Egregious Acts. Make use of your bank account to look throughout the lawful kinds you might have ordered previously. Proceed to the My Forms tab of your bank account and acquire one more copy in the record you want.

In case you are a new consumer of US Legal Forms, here are basic directions that you can comply with:

- Initial, ensure you have selected the correct type for your personal metropolis/region. You can look over the form using the Review button and browse the form information to make sure it is the best for you.

- If the type does not satisfy your preferences, utilize the Seach field to find the correct type.

- Once you are certain that the form is acceptable, click the Acquire now button to obtain the type.

- Opt for the costs strategy you would like and enter in the required info. Build your bank account and buy an order making use of your PayPal bank account or charge card.

- Pick the submit structure and down load the lawful record format in your product.

- Complete, modify and produce and indicator the obtained Michigan Alternative Complaint for an Accounting which includes Egregious Acts.

US Legal Forms is the greatest library of lawful kinds where you will find various record themes. Utilize the company to down load appropriately-manufactured files that comply with state demands.