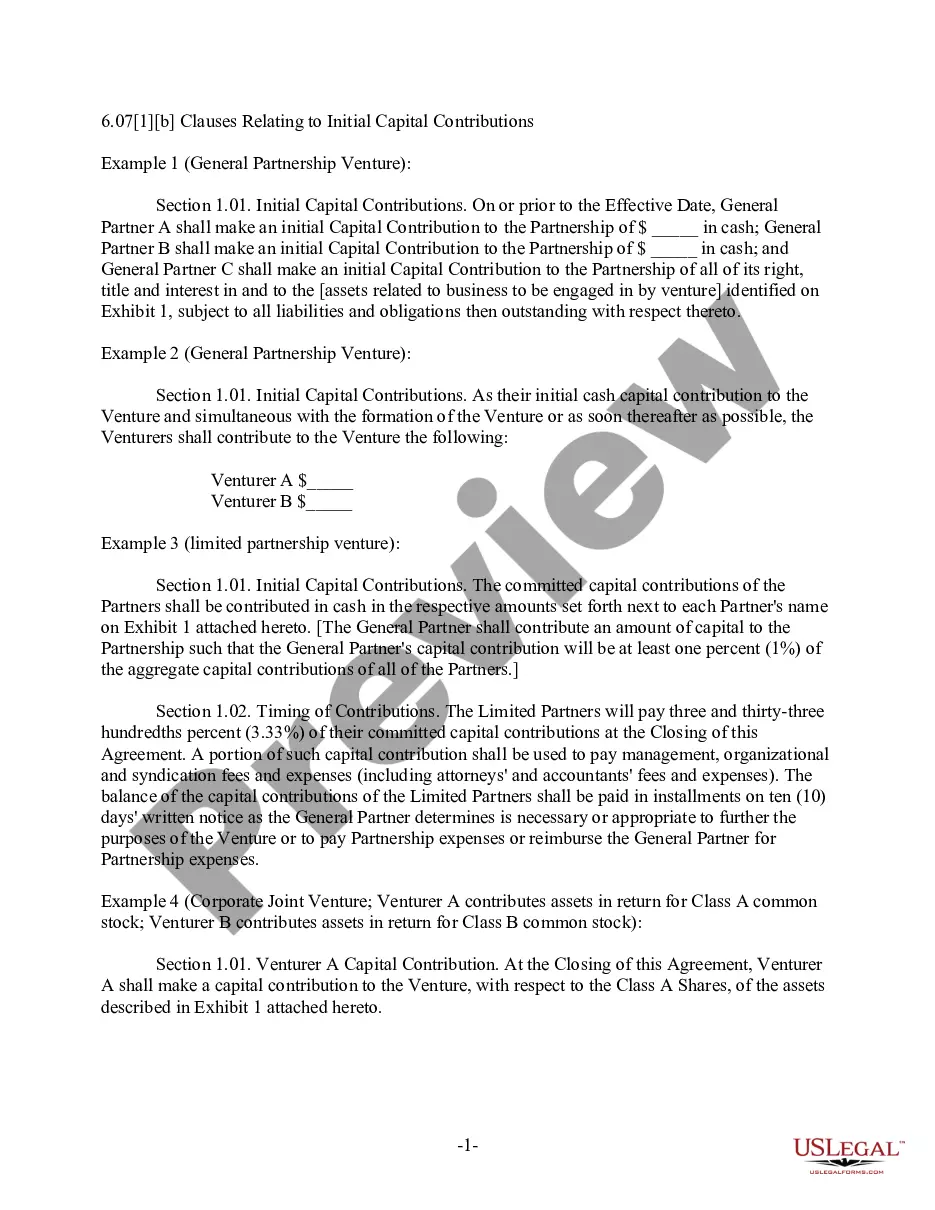

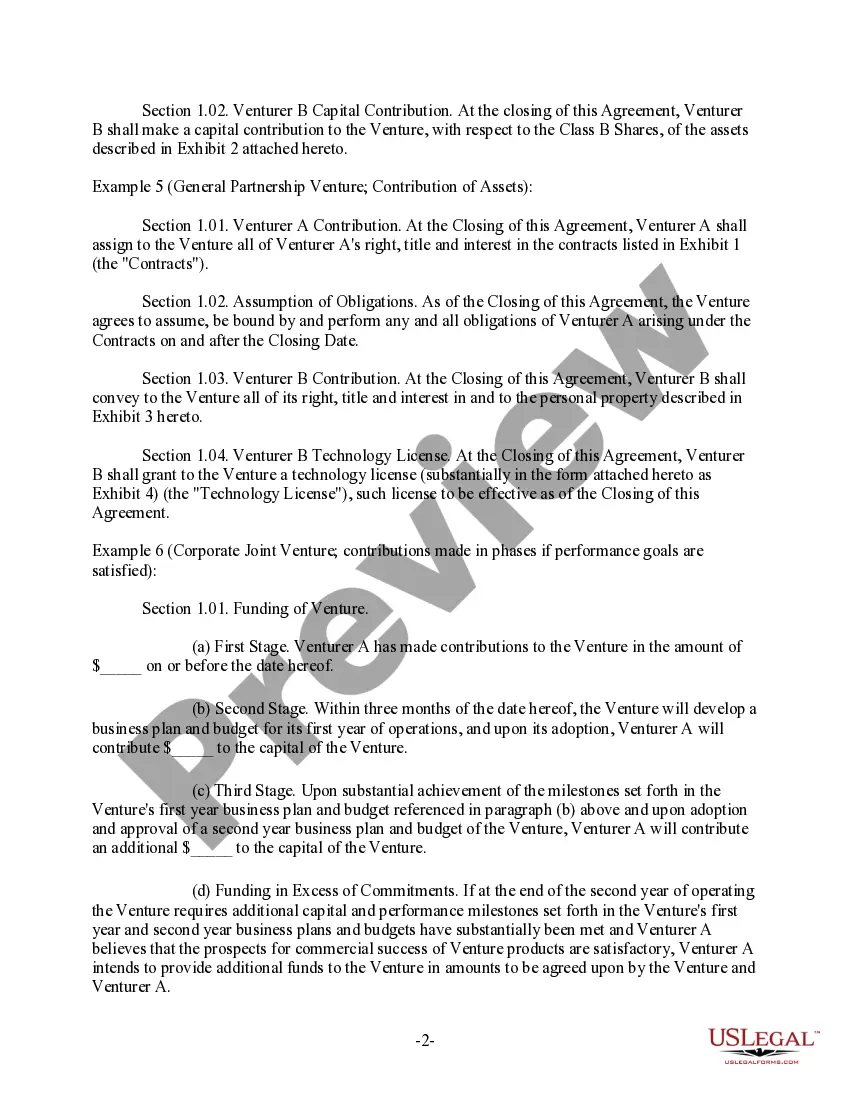

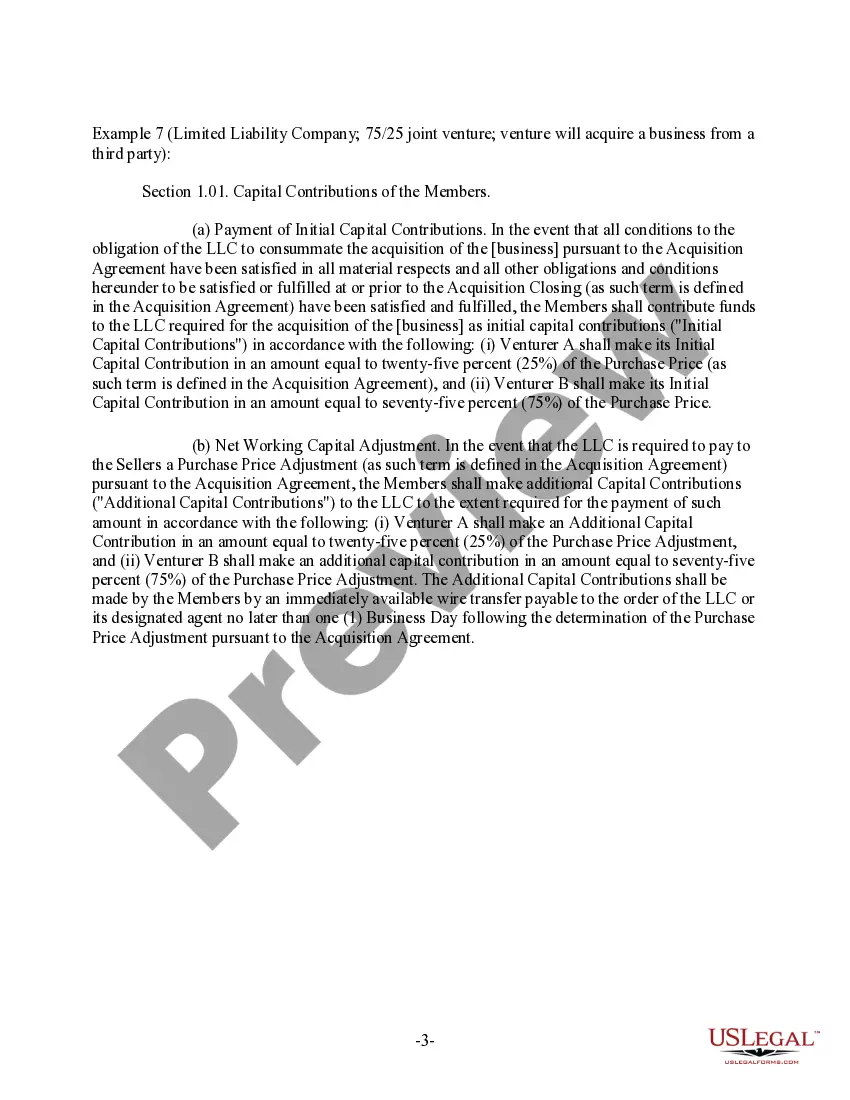

Michigan Clauses Relating to Initial Capital Contributions: A Detailed Description Michigan state laws govern the formation and operation of corporations and limited liability companies (LCS) within its jurisdiction. When it comes to initial capital contributions, there are several clauses within the Michigan Corporate Code and the Michigan Limited Liability Company Act that regulate and outline the procedures and requirements. These clauses are designed to ensure transparency, fairness, and protection for both the company and its stakeholders. 1. Initial Capital Contributions in Michigan Corporations: In Michigan, corporations are required to determine and document the capital structure of the company during the incorporation process. The Articles of Incorporation must include the authorized capital, the number of authorized shares, and the par value, if applicable. Directors and shareholders must agree on the amount and form of contributions required from the shareholders to meet the capital needs of the corporation. a. Monetary Contributions: Shareholders may contribute money as their initial capital contribution to corporations. This could be in the form of cash, check, wire transfer, or any other acceptable method as agreed upon by the shareholders. b. Non-Monetary Contributions: Shareholders may also contribute non-monetary assets, such as property, equipment, patents, or services, as part of their initial capital contribution to the corporation. In such cases, a fair valuation of these assets should be provided. 2. Initial Capital Contributions in Michigan LCS: LCS in Michigan have more flexibility than corporations regarding their initial capital contributions. The Michigan Limited Liability Company Act allows LLC members (owners) to define and allocate capital contributions according to their operating agreement. a. Proportionate Contributions: Members may decide to contribute capital to the LLC based on their ownership percentage. For example, a member owning 40% of the LLC's shares may contribute 40% of the required capital, while another member owning 60% may contribute the remaining 60%. b. Varying Contributions: LLC members can also agree to contribute different amounts or assets as their initial capital contributions. This could be based on their prior agreements, specific skills, or other factors. c. Equal Contributions: In some cases, members may choose to contribute equal amounts as their initial capital contribution, regardless of their ownership percentage. It is important to note that while Michigan allows flexibility in determining initial capital contributions, the operating agreement or bylaws of a corporation or LLC should clearly outline the terms, conditions, and manner of making these contributions. This ensures clarity and reduces the possibility of disputes in the future. Michigan's clauses relating to initial capital contributions provide a legal framework for corporations and LCS, ensuring that all parties involved are aware of their obligations and rights. Proper adherence to these clauses ensures the smooth functioning and financial viability of businesses established within the state.

Michigan Clauses Relating to Initial Capital Contributions: A Detailed Description Michigan state laws govern the formation and operation of corporations and limited liability companies (LCS) within its jurisdiction. When it comes to initial capital contributions, there are several clauses within the Michigan Corporate Code and the Michigan Limited Liability Company Act that regulate and outline the procedures and requirements. These clauses are designed to ensure transparency, fairness, and protection for both the company and its stakeholders. 1. Initial Capital Contributions in Michigan Corporations: In Michigan, corporations are required to determine and document the capital structure of the company during the incorporation process. The Articles of Incorporation must include the authorized capital, the number of authorized shares, and the par value, if applicable. Directors and shareholders must agree on the amount and form of contributions required from the shareholders to meet the capital needs of the corporation. a. Monetary Contributions: Shareholders may contribute money as their initial capital contribution to corporations. This could be in the form of cash, check, wire transfer, or any other acceptable method as agreed upon by the shareholders. b. Non-Monetary Contributions: Shareholders may also contribute non-monetary assets, such as property, equipment, patents, or services, as part of their initial capital contribution to the corporation. In such cases, a fair valuation of these assets should be provided. 2. Initial Capital Contributions in Michigan LCS: LCS in Michigan have more flexibility than corporations regarding their initial capital contributions. The Michigan Limited Liability Company Act allows LLC members (owners) to define and allocate capital contributions according to their operating agreement. a. Proportionate Contributions: Members may decide to contribute capital to the LLC based on their ownership percentage. For example, a member owning 40% of the LLC's shares may contribute 40% of the required capital, while another member owning 60% may contribute the remaining 60%. b. Varying Contributions: LLC members can also agree to contribute different amounts or assets as their initial capital contributions. This could be based on their prior agreements, specific skills, or other factors. c. Equal Contributions: In some cases, members may choose to contribute equal amounts as their initial capital contribution, regardless of their ownership percentage. It is important to note that while Michigan allows flexibility in determining initial capital contributions, the operating agreement or bylaws of a corporation or LLC should clearly outline the terms, conditions, and manner of making these contributions. This ensures clarity and reduces the possibility of disputes in the future. Michigan's clauses relating to initial capital contributions provide a legal framework for corporations and LCS, ensuring that all parties involved are aware of their obligations and rights. Proper adherence to these clauses ensures the smooth functioning and financial viability of businesses established within the state.