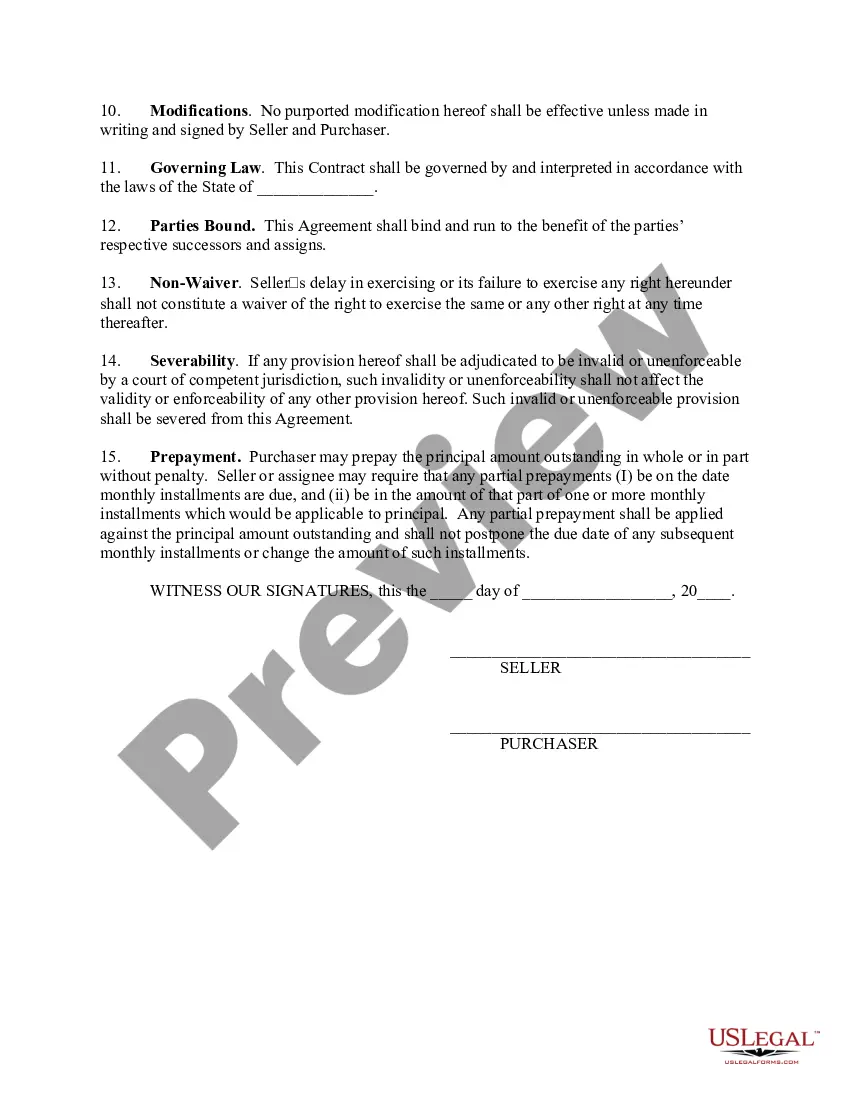

A retail installment agreement is an agreement signed by the Purchaser involving a finance charge and providing for the sale of goods or services. Federal and some State Laws (Consumer Credit Protection Acts) require the disclosure of what the Purchaser is being charged for the credit he/she is receiving. These disclosures include such things as the amount being financed; finance charges; the annual percentage rate; and the number of payments and when due. However, such disclosures are usually only required when a person regularly extends consumer credit (e.g. more than 25 times in the preceding calendar year).

This form is for a casual seller who does not enter into such transactions on a regular basis. It can also be used in commercial transactions (e.g., credit that is not being extended primarily for personal, family, or household purposes).

The Purchaser in this form grants the Seller a security interest in the collateral being sold. A security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. The Seller requires the Purchaser to secure the obligation with the personal property being purchased so that if the Purchaser does not pay as promised, the Purchaser can take the collateral back, sell it, and apply the proceeds against the unpaid obligation of the Purchaser.

The Minnesota Retail Installment Contract or Agreement is a legal document that outlines the terms and conditions of a purchase made on credit. It is used in retail transactions where the buyer agrees to pay for the purchased goods or services over a period of time, typically in installments. This agreement is governed by the Minnesota Retail Installment Sales Act (M.R.I.S.A), which regulates all retail installment contracts in the state. The purpose of the act is to protect both consumers and retailers by outlining the rights and responsibilities of each party involved in the transaction. The Minnesota Retail Installment Contract or Agreement should include several key elements. First and foremost, it should clearly state the names and contact information of both the buyer and the seller. It should also specify the date of the agreement, as well as the date of the purchase. The contract should outline the details of the purchase, including the description of the goods or services being bought, the quantity, and the price. It should also specify the payment terms, such as the total amount financed, the number of installments, the due dates, and the interest rate. Additionally, any additional charges or fees, such as late payment fees or finance charges, should be clearly stated. Under the M.R.I.S.A, there are two main types of Minnesota Retail Installment Contracts or Agreements: closed-end contracts and open-end contracts. 1. Closed-End Contracts: In a closed-end contract, the buyer agrees to repay a fixed amount of money over a specific period of time. This type of contract is commonly used for purchases of durable goods, such as appliances, furniture, or electronics. 2. Open-End Contracts: In an open-end contract, the buyer has an ongoing line of credit with the seller. This type of contract is typically used for revolving credit agreements, such as store credit cards. The buyer can make multiple purchases over time and is required to make minimum monthly payments based on their outstanding balance. Regardless of the type of Minnesota Retail Installment Contract or Agreement, it is important for both the buyer and seller to read and understand all the terms and conditions before signing. It is advisable to seek legal advice or consult a financial professional to ensure compliance with the M.R.I.S.A and to protect one's rights and interests.