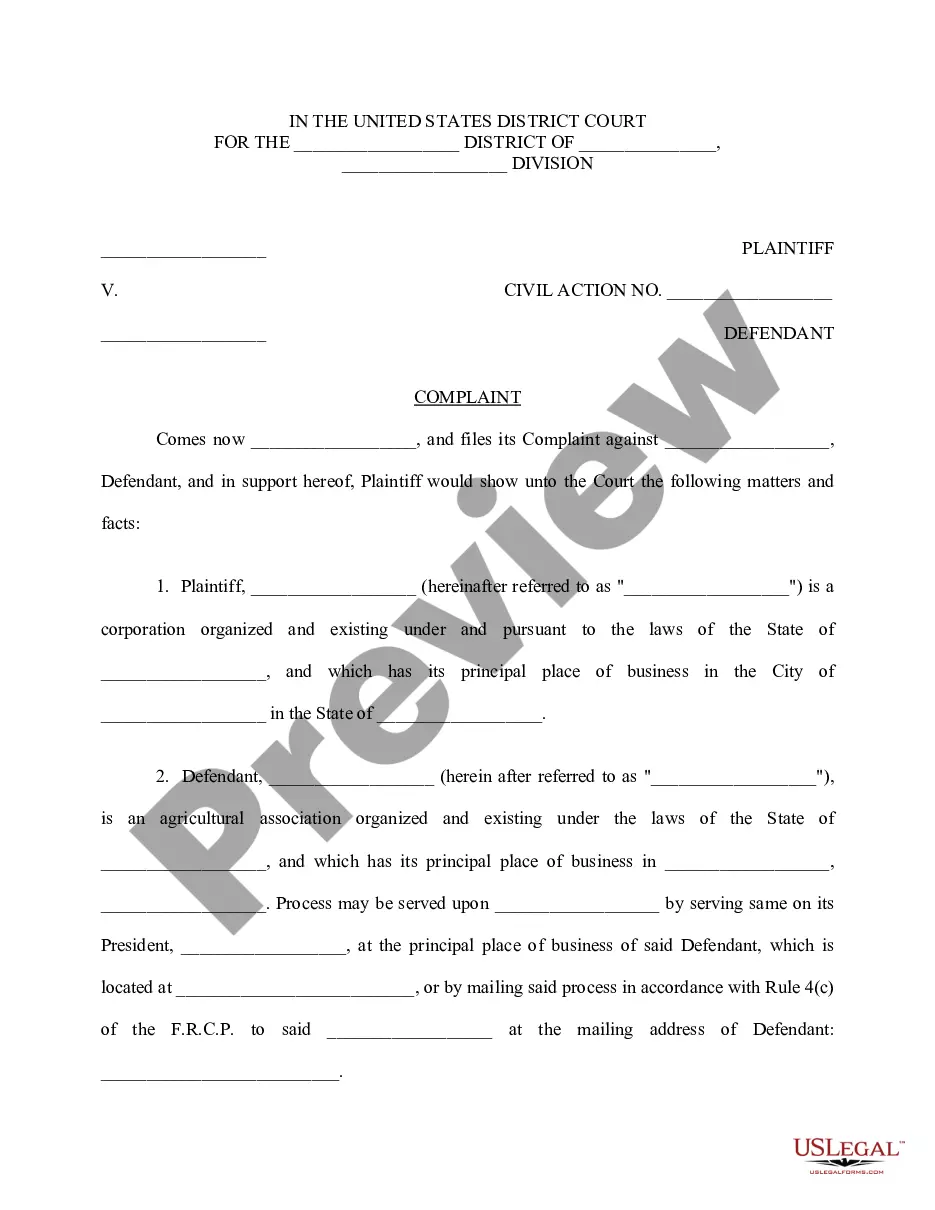

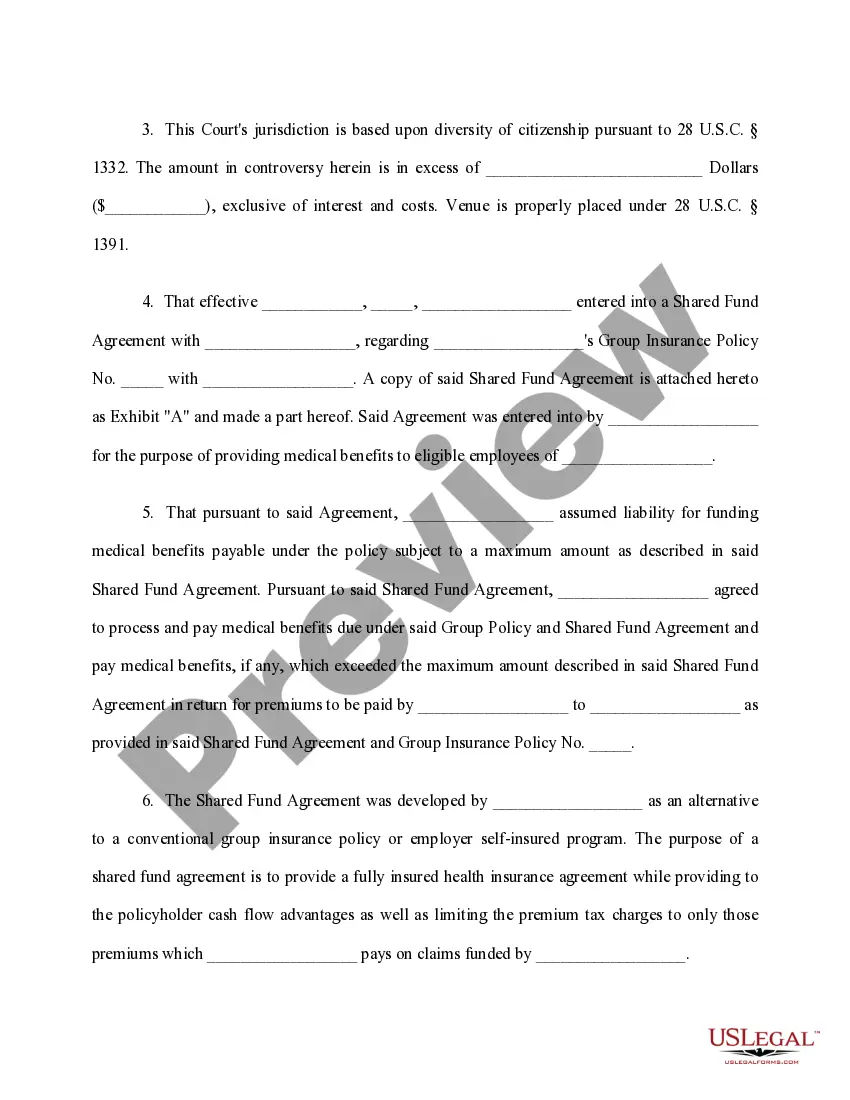

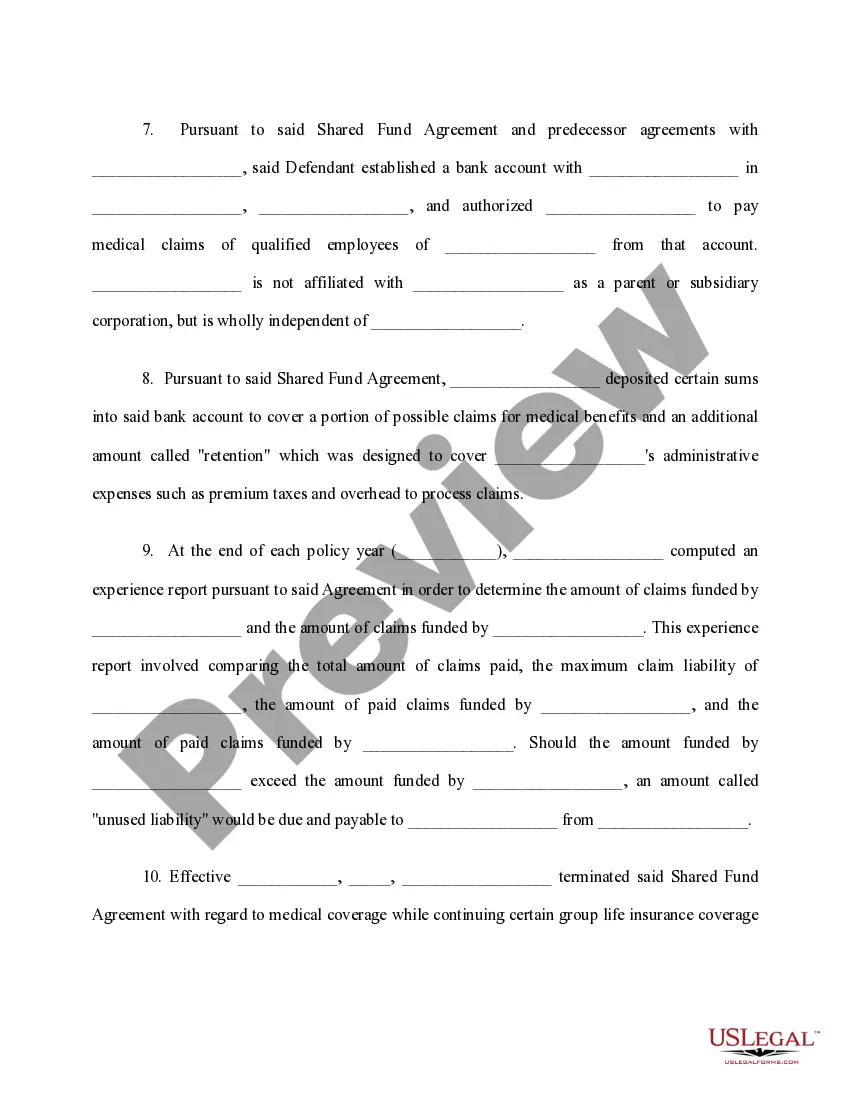

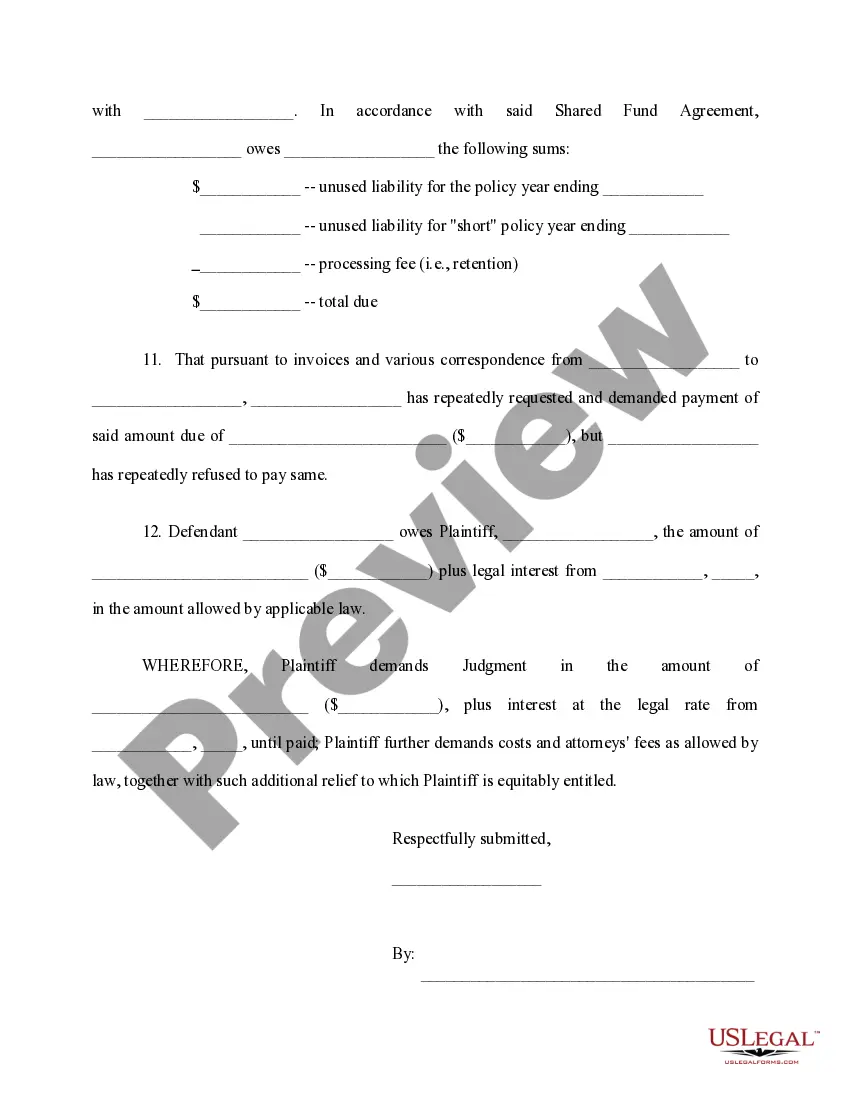

Title: Understanding Minnesota Complaints regarding Group Insurance Contracts Introduction: When it comes to group insurance contracts in Minnesota, it is crucial to know the potential complaints that might arise. This detailed description aims to clarify what constitutes a Minnesota complaint regarding group insurance contracts, explain the key components involved, and outline different types of complaints one may encounter. 1. Minnesota Complaints regarding Group Insurance Contracts: In Minnesota, complaints arise when there are disputes, dissatisfaction, or disagreement related to group insurance contracts. These complaints encompass various aspects, including policy coverage, claim settlements, premium rates, contract terms, exclusions, and other related concerns. It is essential to address and resolve these complaints to maintain a fair and transparent insurance market. 2. Key Components of a Minnesota Complaint: a. Policy Coverage: Complaints can revolve around inadequate coverage provided by the group insurance contract, especially if essential benefits or services are missing or not clearly defined. b. Claim Settlement: Discontent with claim settlements, such as delays, inadequate compensations, or denial of valid claims, is a common cause for complaints. c. Premium Rates: Complaints can arise if there are inconsistencies or unfairness in the calculation of premium rates, leading to higher costs for the insured group. d. Contract Terms: Disputes can occur if the terms of the contract are ambiguous, misleading, or differ from what was initially agreed upon. e. Exclusions and Limitations: Complaints may arise when certain coverages are excluded or limitations imposed, affecting policyholders' ability to utilize insurance benefits fully. 3. Different Types of Minnesota Complaints regarding Group Insurance Contracts: a. Coverage Denial Complaints: These complaints occur when the insurer refuses to cover a specific medical procedure, treatment, or service, leading to dissatisfaction or financial burden for the policyholder. b. Claim Handling Complaints: Complaints stem from delays, incomplete investigations, or insufficient compensations during the claims process, causing frustration and dissatisfaction. c. Premium Rate Complaints: These complaints highlight concerns about unfair, incorrect, or sudden premium rate increases, impacting the financial stability of policyholders. d. Contract Disclosure Complaints: Complaints arise when the terms and conditions of the group insurance contract are not adequately disclosed or explained, leading to misunderstanding and potential disputes. e. Provider Network Complaints: These complaints involve issues related to the availability, accessibility, or quality of healthcare providers within the group insurance network, causing inconveniences and dissatisfaction. Conclusion: Being aware of the potential Minnesota complaints regarding group insurance contracts is essential to protect the rights and interests of policyholders. Addressing concerns related to policy coverage, claim settlements, premium rates, contract terms, and exclusions is crucial to maintain a fair insurance market. Understanding the types of complaints that may arise provides insights into potential areas of improvement for insurers, ensuring customer satisfaction and trust.

Minnesota Complaint regarding Group Insurance Contract

Description

How to fill out Minnesota Complaint Regarding Group Insurance Contract?

You are able to spend hours on the Internet trying to find the legal papers design that fits the federal and state specifications you will need. US Legal Forms gives 1000s of legal forms that happen to be evaluated by professionals. It is possible to download or print the Minnesota Complaint regarding Group Insurance Contract from your assistance.

If you have a US Legal Forms account, you are able to log in and then click the Obtain switch. Next, you are able to total, change, print, or indicator the Minnesota Complaint regarding Group Insurance Contract. Every single legal papers design you purchase is yours permanently. To obtain an additional duplicate for any acquired kind, check out the My Forms tab and then click the corresponding switch.

If you use the US Legal Forms website the first time, stick to the straightforward guidelines listed below:

- Very first, ensure that you have chosen the best papers design for the region/area of your choice. Look at the kind explanation to make sure you have chosen the correct kind. If accessible, take advantage of the Preview switch to look from the papers design also.

- If you would like discover an additional edition in the kind, take advantage of the Lookup area to obtain the design that fits your needs and specifications.

- Upon having found the design you desire, click on Buy now to move forward.

- Choose the rates program you desire, enter your accreditations, and sign up for a free account on US Legal Forms.

- Complete the deal. You should use your bank card or PayPal account to cover the legal kind.

- Choose the structure in the papers and download it in your product.

- Make changes in your papers if necessary. You are able to total, change and indicator and print Minnesota Complaint regarding Group Insurance Contract.

Obtain and print 1000s of papers templates while using US Legal Forms Internet site, which provides the largest assortment of legal forms. Use skilled and express-specific templates to deal with your organization or personal demands.