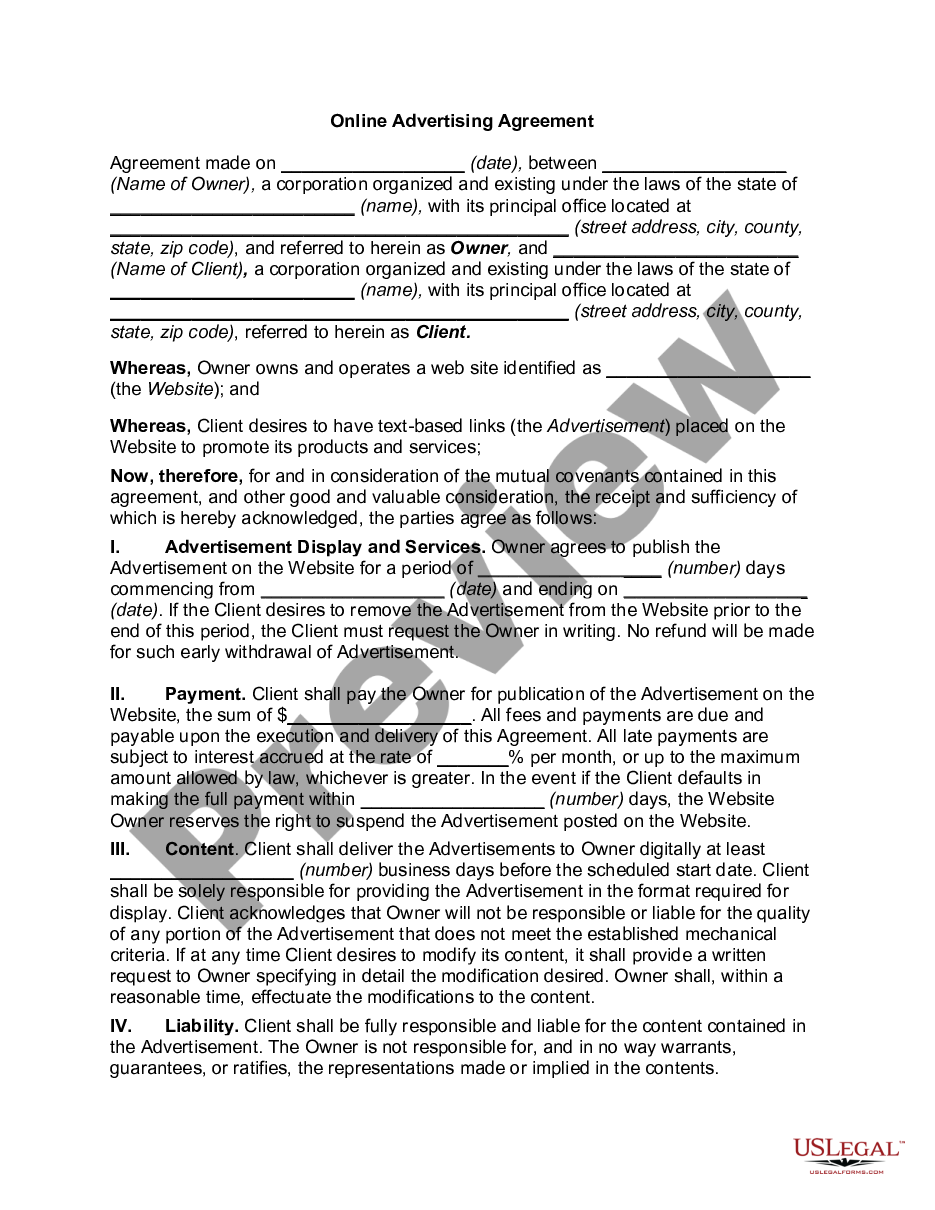

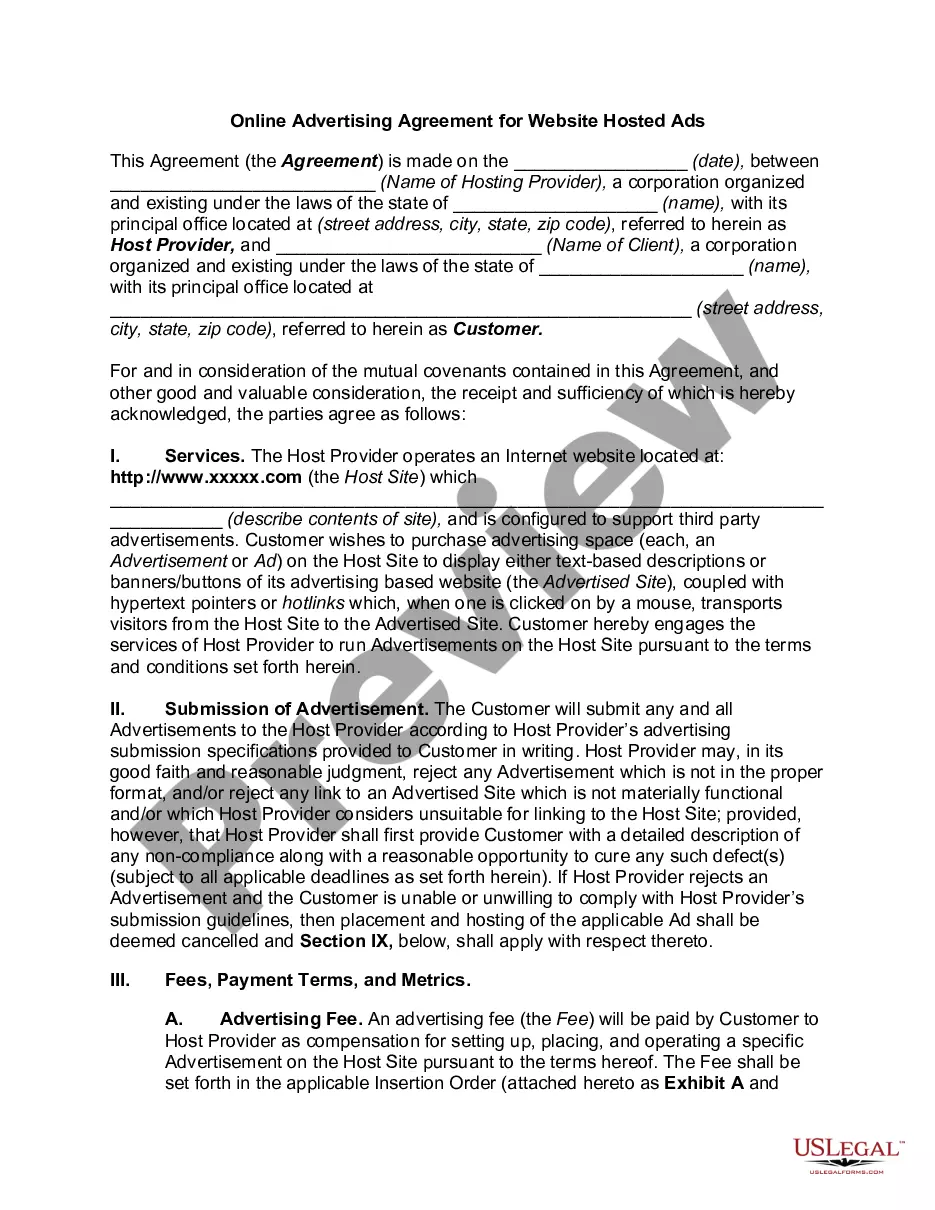

Minnesota Website Advertising Contract

Description

How to fill out Website Advertising Contract?

US Legal Forms - one of the largest collections of legal forms in the United States - provides a selection of legal document formats that you can purchase or create.

By using the site, you can access thousands of forms for commercial and personal use, organized by categories, states, or keywords.

You can find the latest versions of forms such as the Minnesota Website Advertising Contract in mere seconds.

Review the form summary to confirm that you have selected the right document.

If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you already have an account, Log In and obtain the Minnesota Website Advertising Contract from the US Legal Forms catalog.

- The Download button will appear on each form you view.

- You can access all previously obtained forms in the My documents section of your account.

- If you are using US Legal Forms for the first time, here are straightforward steps to get you started.

- Ensure you have selected the correct form for your city/state.

- Click the Review option to examine the form's details.

Form popularity

FAQ

You are responsible for collecting and remitting sales tax on taxable sales made through your website and other sources. When the marketplace is not required to collect Minnesota sales tax on your behalf, you must also collect and remit Minnesota sales tax on those taxable sales.

Charges for maintenance or upgrades to online hosting software are not taxable, even if separately stated. Digital products are products provided to a customer electronically.

Common examples include:Clothing for general use, see Clothing.Food (grocery items), see Food and Food Ingredients.Prescription and over-the-counter drugs for humans, see Drugs.

The rendering of advertising and public relations services is not taxable when related to the development of media advertising. The total gross receipts for advertising services related to the development of media advertising billed by the service provider are not subject to sales tax.

In essence, the advertising income is subject to tax only if the periodical produces an overall profit for the year. If the circulation income of the periodical equals or exceeds the readership costs, the organization is not required to use circulation income and readership costs in calculating UBTI.

Charges for maintenance or upgrades to online hosting software are not taxable, even if separately stated. Digital products are products provided to a customer electronically.

If the web design is delivered electronically, meaning there is no tangible property transfer, no sales tax will be charged. However, if the finished site is transferred to a zip drive, disk or a paper copy of the site design is provided, there is a tangible property transfer, and sales tax must be charged.

Advertising that has functional use is taxable. Example: A brochure is used only for advertising. If the advertising message is taken away, nothing is left but a piece of paper. However, a calendar with an advertising message on it is used for both advertising and also date information.