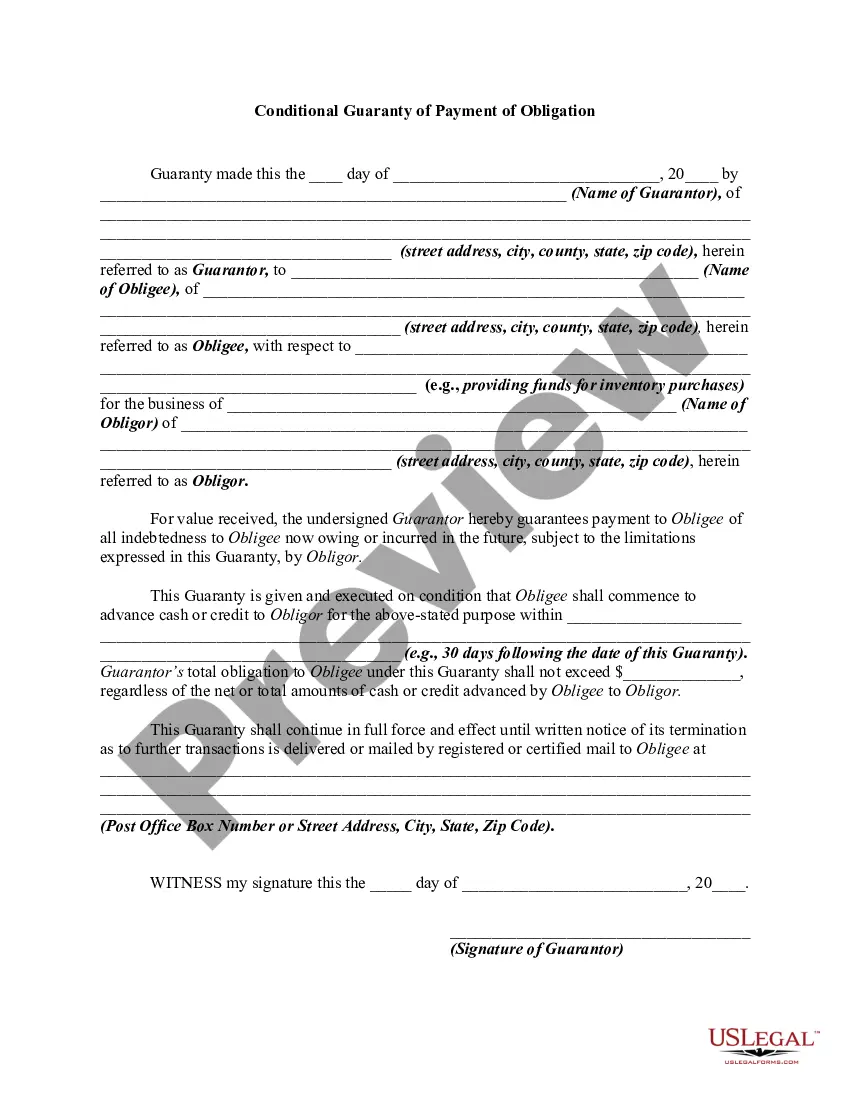

A guaranty is a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law. A conditional guaranty contemplates, as a condition to liability on the part of the guarantor, the happening of some contingent event. A guaranty of the payment of a debt is distinguished from a guaranty of the collection of the debt, the former being absolute and the latter conditional.

A Minnesota Conditional Guaranty of Payment of Obligation is a legal agreement wherein a guarantor agrees to be responsible for the payment of a specific debt or obligation in the event that the primary borrower defaults. This type of guaranty provides additional security to the lender and ensures that the debt will be repaid, even if the borrower is unable to fulfill their obligations. In Minnesota, there are a few different types of Conditional Guaranty of Payment of Obligation that can be utilized: 1. Unconditional Guaranty: This type of guaranty is the most common and straightforward form, where the guarantor agrees to be fully responsible for the debt or obligation in case of default by the borrower. It does not require any specific conditions or limitations to be triggered. 2. Limited Guaranty: Unlike an unconditional guaranty, a limited guaranty imposes certain restrictions or limitations on the guarantor's liability. The guarantor may agree to guarantee only a portion of the debt, up to a specific amount, or for a limited period. These limitations are typically negotiated and agreed upon by the parties involved. 3. Continuing Guaranty: A continuing guaranty is one where the guarantor's liability extends to all existing and future obligations owed by the borrower to the creditor. It remains in effect until the guarantor provides written notice of revocation or the parties mutually agree to terminate the guaranty. 4. Limited Recourse Guaranty: This type of guaranty limits the guarantor's liability to certain predetermined assets or collateral. In case of default, the lender's recourse will be limited to recovering from those specified assets, rather than pursuing the guarantor for the full amount. It provides some protection to the guarantor while offering reassurance to the lender. 5. Conditional Guaranty with Performance Trigger: In this type of guaranty, the guarantor's liability is triggered by a specific event or condition. For example, it may specify that the guarantor becomes liable only if the borrower's business fails to generate a certain level of revenue. The guarantor's obligation is then conditioned upon the occurrence of the specified trigger. Overall, a Minnesota Conditional Guaranty of Payment of Obligation provides a legal framework to ensure that a debt or obligation is repaid, even if the borrower default. The specific type of guaranty chosen will depend on the negotiation between the parties involved, their level of trust, and the borrower's financial situation. It is crucial for all parties to carefully review and understand the terms and conditions of the guaranty before entering into such a legal agreement.A Minnesota Conditional Guaranty of Payment of Obligation is a legal agreement wherein a guarantor agrees to be responsible for the payment of a specific debt or obligation in the event that the primary borrower defaults. This type of guaranty provides additional security to the lender and ensures that the debt will be repaid, even if the borrower is unable to fulfill their obligations. In Minnesota, there are a few different types of Conditional Guaranty of Payment of Obligation that can be utilized: 1. Unconditional Guaranty: This type of guaranty is the most common and straightforward form, where the guarantor agrees to be fully responsible for the debt or obligation in case of default by the borrower. It does not require any specific conditions or limitations to be triggered. 2. Limited Guaranty: Unlike an unconditional guaranty, a limited guaranty imposes certain restrictions or limitations on the guarantor's liability. The guarantor may agree to guarantee only a portion of the debt, up to a specific amount, or for a limited period. These limitations are typically negotiated and agreed upon by the parties involved. 3. Continuing Guaranty: A continuing guaranty is one where the guarantor's liability extends to all existing and future obligations owed by the borrower to the creditor. It remains in effect until the guarantor provides written notice of revocation or the parties mutually agree to terminate the guaranty. 4. Limited Recourse Guaranty: This type of guaranty limits the guarantor's liability to certain predetermined assets or collateral. In case of default, the lender's recourse will be limited to recovering from those specified assets, rather than pursuing the guarantor for the full amount. It provides some protection to the guarantor while offering reassurance to the lender. 5. Conditional Guaranty with Performance Trigger: In this type of guaranty, the guarantor's liability is triggered by a specific event or condition. For example, it may specify that the guarantor becomes liable only if the borrower's business fails to generate a certain level of revenue. The guarantor's obligation is then conditioned upon the occurrence of the specified trigger. Overall, a Minnesota Conditional Guaranty of Payment of Obligation provides a legal framework to ensure that a debt or obligation is repaid, even if the borrower default. The specific type of guaranty chosen will depend on the negotiation between the parties involved, their level of trust, and the borrower's financial situation. It is crucial for all parties to carefully review and understand the terms and conditions of the guaranty before entering into such a legal agreement.