A lender funds the loan, may service the loan payments, and ensure the loans' compliance with underwriting guidelines. The mortgage broker, on the other hand, originates the loan. A detailed application process, financial and credit worthiness investigation, and disclosure requirements must be completed in order for a lender to evaluate a loan request. The broker simplifies this process for the borrower and the lender, by conducting this research, counseling consumers on their loan package choices, and enabling them to select the right loan for their needs.

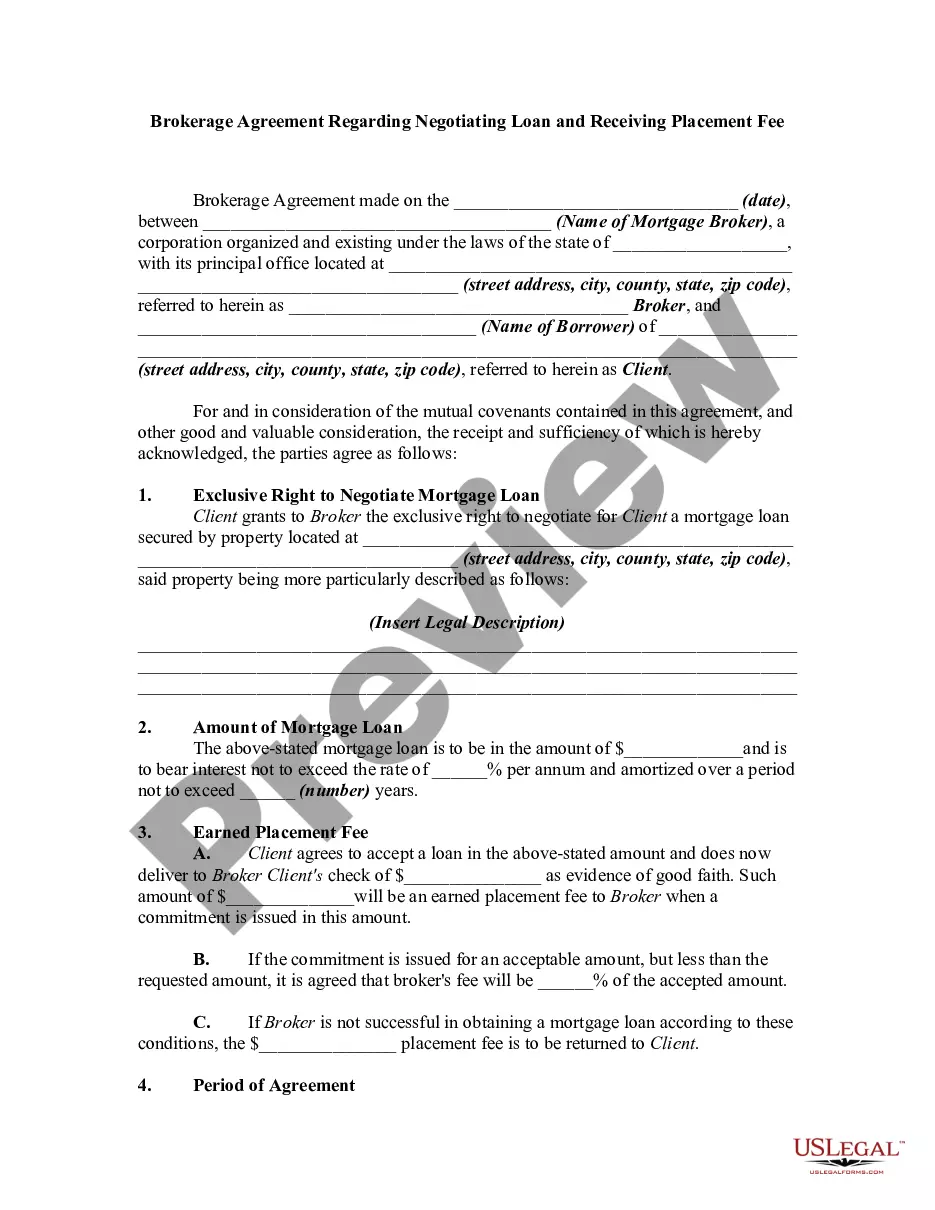

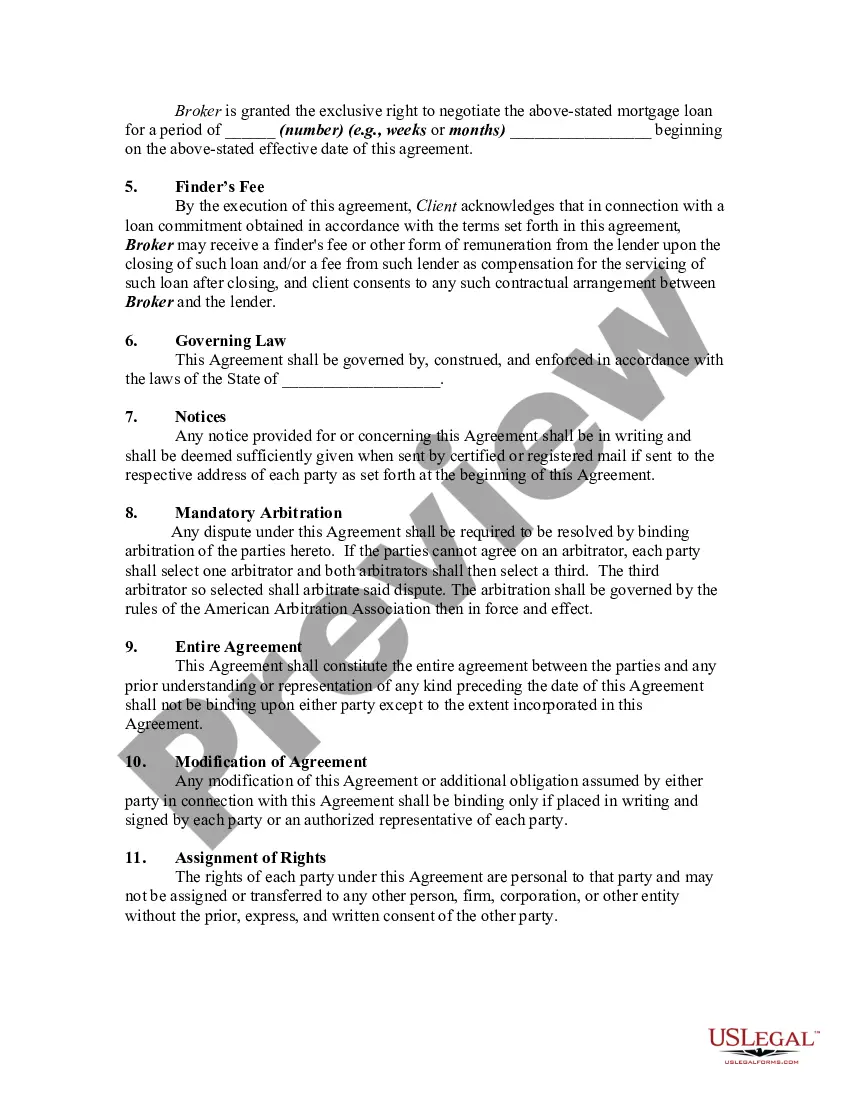

A Minnesota Brokerage Agreement Regarding Negotiating Loan and Receiving Placement Fee is a legally binding document that outlines the terms and conditions between a loan broker and a client who wishes to obtain a loan. This agreement defines the responsibilities and rights of both parties involved in the loan negotiation and placement process. The key keywords relevant to this agreement are Minnesota, Brokerage Agreement, Negotiating Loan, and Receiving Placement Fee. In Minnesota, there may be different types of Brokerage Agreements regarding negotiating loans and receiving placement fees, including but not limited to: 1. Residential Mortgage Loan Brokerage Agreement: This type of agreement is specific to brokers dealing with residential mortgage loans. It outlines the broker's responsibilities in securing loan options and negotiating terms on behalf of the client. 2. Commercial Loan Brokerage Agreement: This agreement focuses on brokering commercial loans for businesses or real estate ventures. It may include clauses related to property valuation, loan terms, and negotiation strategies specific to commercial lending. 3. Personal Loan Brokerage Agreement: When a broker assists an individual in obtaining a personal loan, this type of agreement comes into play. It outlines the terms related to interest rates, repayment schedules, and any applicable fees. 4. Payday Loan Brokerage Agreement: This agreement pertains to brokers working within the payday loan industry. It may include provisions related to loan amounts, repayment terms, and fees associated with payday lending. In each of these variations of the Minnesota Brokerage Agreement Regarding Negotiating Loan and Receiving Placement Fee, the document typically includes the following details: — Parties Involved: The agreement identifies the names and contact information of the loan broker and the client. — Scope of Services: This section outlines the specific services that the broker will provide, such as loan sourcing, negotiations, and placement. — Broker's Compensation: The agreement specifies the broker's fees or commission for their services, including any upfront fees, percentage of loan amount, or other agreed-upon compensation models. — Client Obligations: This section describes the client's responsibilities, which may include providing accurate financial information, cooperating with the broker, and timely communication. — Terms and Termination: The agreement defines the duration of the contract, any renewal or termination clauses, and rights of either party to terminate the agreement. — Confidentiality and Non-Disclosure: This section emphasizes the obligation to maintain confidentiality regarding all sensitive financial information and trade secrets shared during the agreement. — Governing Law: The agreement may reference the state laws of Minnesota that govern the terms and enforcement of the agreement. — Dispute Resolution: This section outlines the process for resolving any disputes that may arise between the broker and the client, such as mediation or arbitration. It is essential for both parties to thoroughly review and understand the terms outlined in the Minnesota Brokerage Agreement Regarding Negotiating Loan and Receiving Placement Fee before signing it, as it will govern their professional relationship and the loan negotiation process.