Minnesota UCC-1 for Personal Credit

Description

How to fill out UCC-1 For Personal Credit?

Finding the appropriate authentic document template can be challenging.

Surely, there are numerous templates accessible online, but how do you identify the authentic form you need.

Utilize the US Legal Forms website. The platform offers thousands of templates, including the Minnesota UCC-1 for Personal Credit, which you can use for both business and personal purposes.

You can preview the form using the Review button and read the form summary to confirm it's the right one for you.

- All forms are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Download button to retrieve the Minnesota UCC-1 for Personal Credit.

- Use your account to search through the legal forms you have previously acquired.

- Visit the My documents section of your account to download an additional copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward directions to follow.

- First, ensure you have selected the correct form for your city/area.

Form popularity

FAQ

You can file your UCC-1 statement with the Minnesota Secretary of State or relevant local offices. Utilizing the Minnesota UCC-1 for Personal Credit helps ensure your filing is legally recognized. Submitting your UCC-1 correctly is crucial for protecting your interests in personal property. For a straightforward filing process, uslegalforms can guide you every step of the way.

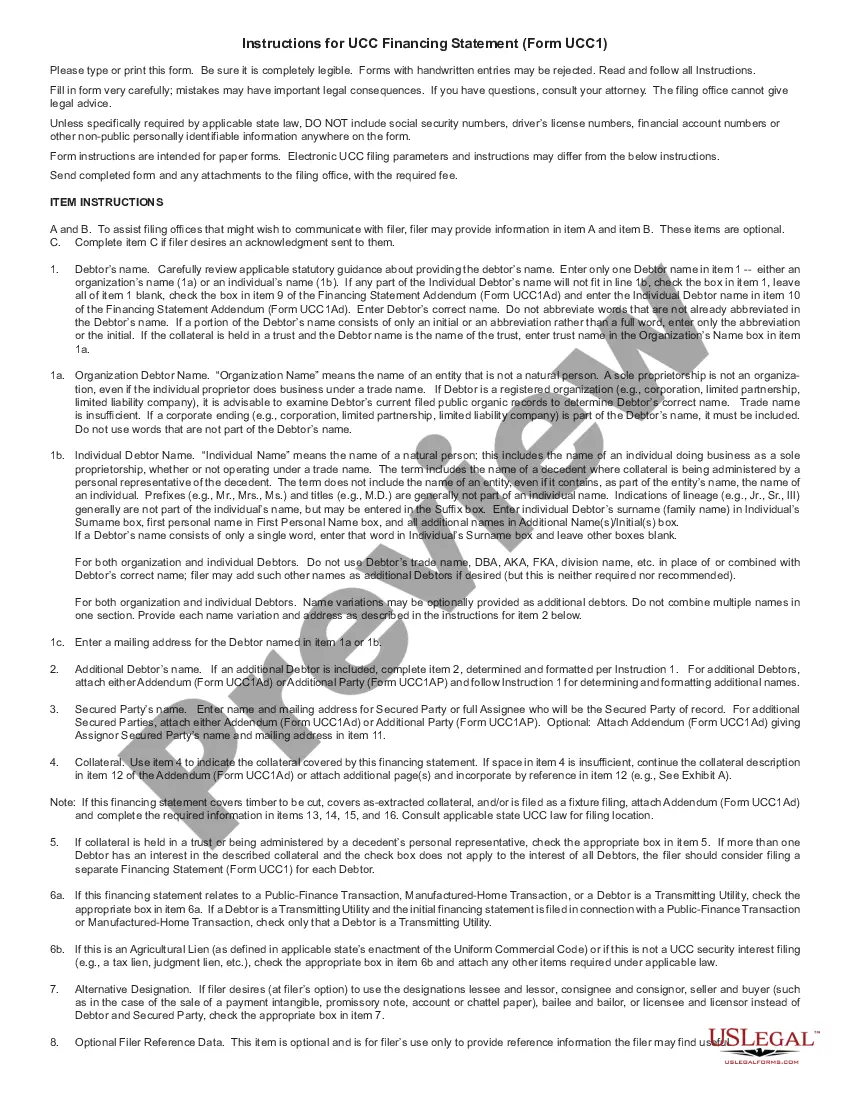

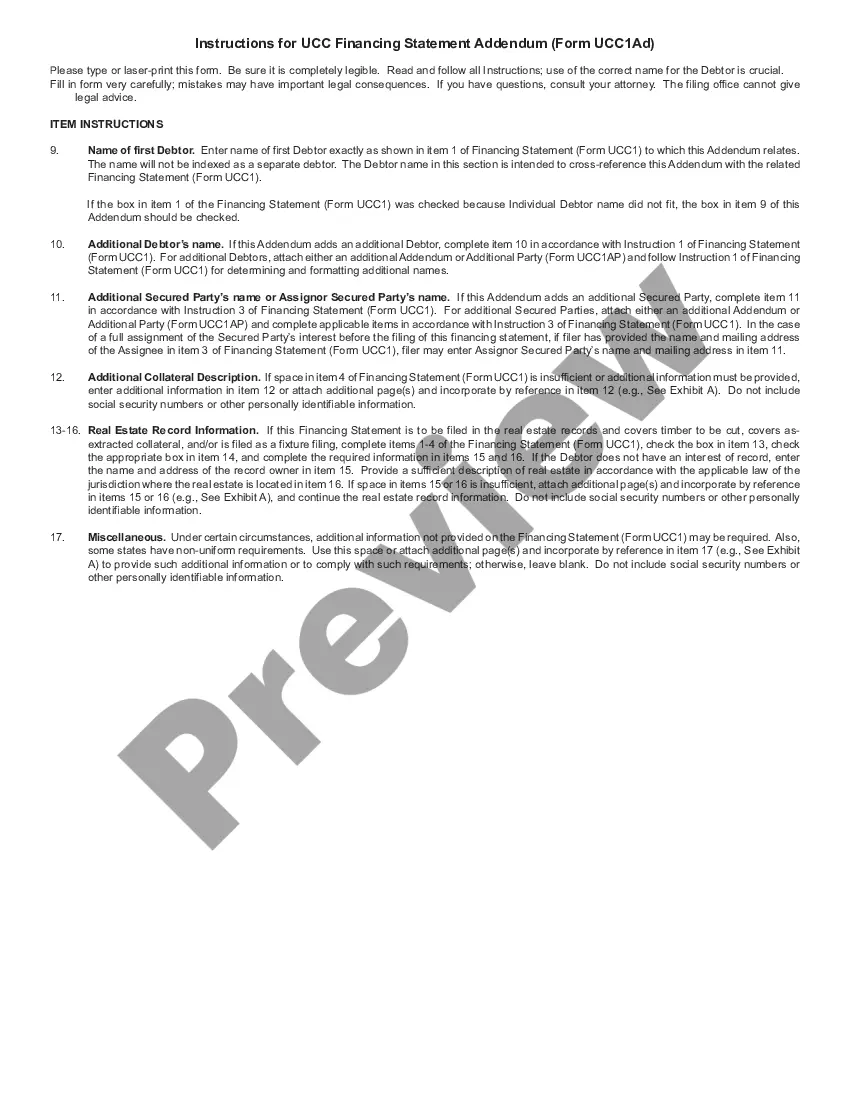

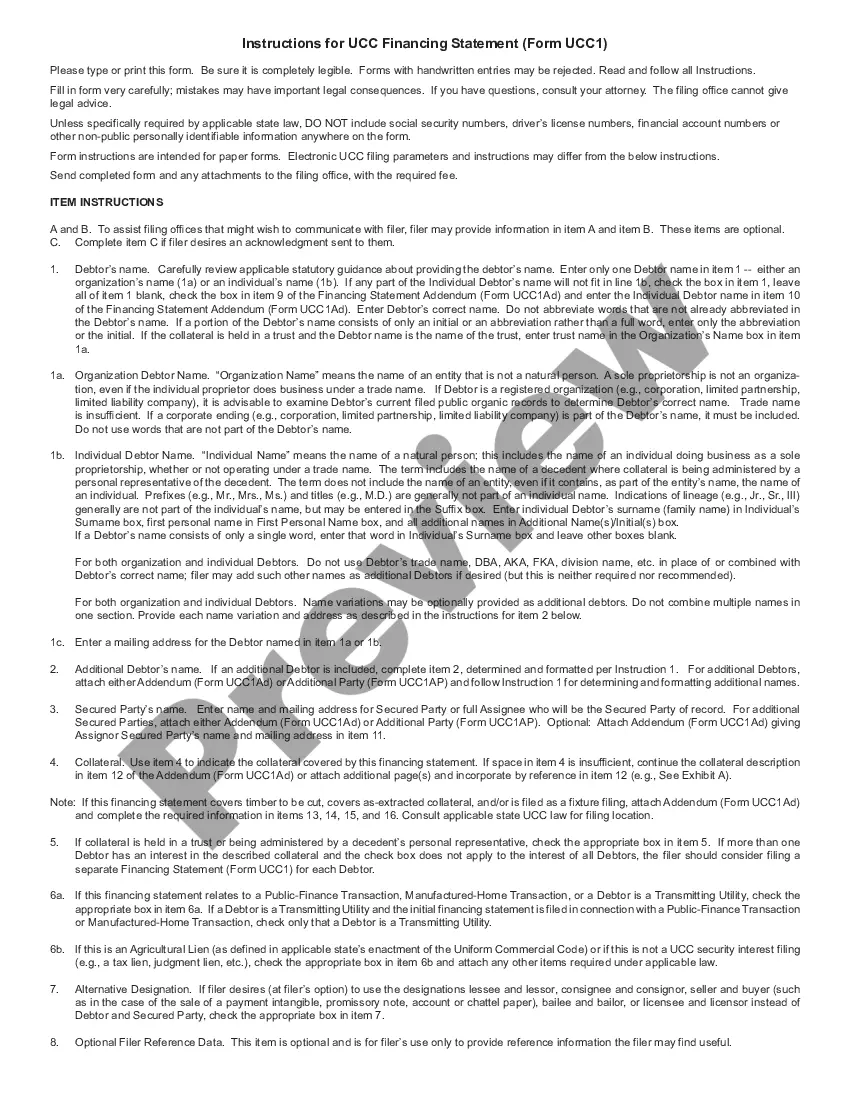

To file a UCC-1, you need to provide specific information about the secured party, the debtor, and the collateral. This information must be accurate and detailed to comply with the Minnesota UCC-1 for Personal Credit. It is essential to properly describe the assets to ensure legality and effectiveness. For guidance on filling out your UCC-1 correctly, consider using uslegalforms, which simplifies the filing process.

Yes, the UCC applies to personal property, covering a wide range of assets. With the Minnesota UCC-1 for Personal Credit, you can secure interests in various kinds of personal property. This could include equipment, inventory, or other assets. Understanding this framework can help you manage your claims more effectively, and platforms like uslegalforms offer resources to assist you.

A UCC filing generally does not directly appear on personal credit reports. However, it is visible in public records and can affect your financial reputation. When a UCC-1 is filed under the Minnesota UCC-1 for Personal Credit, it signifies an obligation that may impact your borrowing ability. If you're concerned about this, consulting with uslegalforms can provide clarity.

Yes, a UCC-1 can be filed on an individual as it serves to secure interests in personal property. The Minnesota UCC-1 for Personal Credit allows creditors to establish their claim on collateral. This filing gives you a public record of your interest, which can be crucial for protecting your rights. For ease and accuracy in filing, platforms like uslegalforms can help.

Yes, you can file a UCC against an individual, specifically to secure a debt or obligation. This process is common under the Minnesota UCC-1 for Personal Credit. It provides a legal claim against the individual's personal property, ensuring that your interests are protected. If you need assistance with filing, consider using platforms like uslegalforms to navigate the process.

A UCC filing can potentially have a negative impact on your credit score. It showcases that you are using your assets as collateral, which can be viewed unfavorably by some lenders. However, with responsible management of your finances after a Minnesota UCC-1 for Personal Credit filing, you can still maintain a healthy credit profile. Furthermore, using resources like USLegalForms can help you understand the ramifications and manage your filings effectively.

To properly fill out a Minnesota UCC-1 for Personal Credit, gather correct information about the debtor and secured party. Be precise when describing the collateral, and ensure you include all required signatures. Double-check the filing instructions specific to Minnesota, as each state may have slight variations. For ease, consider using ulegalforms, which offers guidance throughout the process.

A UCC filing, specifically a Minnesota UCC-1 for Personal Credit, is a legal notice that a lender has a security interest in the property of a borrower. This filing protects the lender by establishing a record of their claim. It's essential for people looking to secure financing against personal assets. Understanding this process can help you navigate personal credit effectively.

To fill out a Minnesota UCC-1 for Personal Credit, start by entering the name of the debtor. Next, provide the secured party's name and address. Then, specify the collateral type, ensuring you describe it clearly. Finally, review your information for accuracy before submitting the form to the appropriate state agency.